Key Points

Amazon has already sold out chip capacity for months in advance.

The company's stock looks like a smart buy now.

- These 10 stocks could mint the next wave of millionaires ›

Nvidia (NASDAQ: NVDA) has been one of the top ways to invest in artificial intelligence (AI) since 2023. Its GPUs were and still are the go-to computing chip for nearly every AI hyperscaler.

However, Nvidia is no longer the only option available. There are other chip designers tailoring their designs for specific workloads, giving them an advantage over more broad-purpose GPUs. Broadcom (NASDAQ: AVGO) is the most popular pick in that sector, but there's another one that investors need to watch out for: Amazon (NASDAQ: AMZN).

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Amazon isn't the first company that comes to mind in the AI computing space, but it should be. Amazon Web Services (AWS) and its custom chips are starting to make waves. Nvidia shareholders need to be aware of this growing threat and continue to monitor the situation, as Amazon had some fighting words for Nvidia.

Image source: Getty Images.

Could Nvidia chips be replaced by Amazon's?

In Amazon's shareholder letter, CEO Andy Jassy made some noteworthy comments regarding Nvidia chips. He began by using an example of another competitor the company has taken down.

In 2018, Amazon released its Graviton CPU, which was a competitor to Intel. Back then, everyone was using Intel's CPUs. Now, Amazon notes that 98% of its large clients utilize Amazon's custom-designed Graviton CPUs. Jassy sees the same thing happening in the GPU space, as their Trainium chips offer better cost-performance than GPU-based training.

The current generation offers about a 30% improvement over GPU-based training, and the upcoming generations (whose computing capacity is already sold out) will see further improvement. This underscores how much more efficient purpose-built chips can be, and it could be something Nvidia needs to watch out for.

While Amazon is actively trying to steal Nvidia's market share, it also noted that it's committed to being the best platform to utilize Nvidia chips. So Amazon isn't turning its back on Nvidia; it's just challenging it while also being a partner.

This may give Nvidia investors some relief, but they should also consider buying Amazon shares, just in case Amazon can truly shift the majority of its customers to its custom chips.

Amazon is a solid investment pick

While Amazon may seem like a mature e-commerce investment, the reality is that AWS is far more important to the company's bottom line than e-commerce. In Q4, AWS produced 50% of Amazon's operating profits. In Q3, that figure was 66%. With AWS making most of the profits, it's really the decision to watch.

As long as AWS is growing rapidly, it really doesn't matter what the company's overall revenue growth rate is, because its profit growth will be much faster.

With AWS having its best quarter in over three years, now is the perfect time to hop on the Amazon bandwagon. The company has huge growth ahead, something Jassy pointed out in his shareholder letter.

It is spending $200 billion on capital expenditures this year, with most of that going to AWS infrastructure. Amazon has commitments from several major clients to use the new capacity, which will drive rapid revenue growth once the infrastructure is online.

Even though Amazon's stock has run up a bit in the past few days, it's still attractively priced.

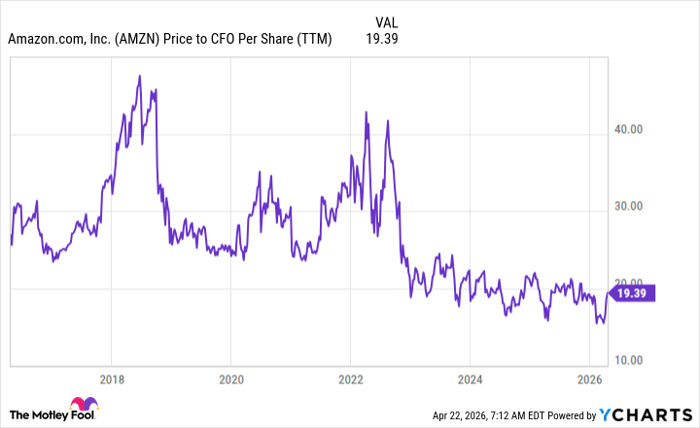

AMZN Price to CFO Per Share (TTM) data by YCharts

Valuing Amazon's stock on operating cash flow is a smart way to assess the company, because it always has to invest in new capabilities in its commerce and cloud businesses, so its earnings can be thrown out of whack quite often. Using cash flow valuation eliminates these oddities and gives investors an idea of how much money a business truly generates.

With Amazon being valued toward the lower end of its usual range, I think now is still a solid time to buy the stock.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $540,224!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $51,615!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $498,522!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of April 25, 2026.

Keithen Drury has positions in Amazon, Broadcom, and Nvidia. The Motley Fool has positions in and recommends Amazon, Broadcom, Intel, and Nvidia. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.