Newell Brands, Inc. NWL highlighted that 2025 proved more challenging than anticipated. The company expected a positive inflection in the core sales in the back half of 2025. However, tariffs disrupted this outlook, forcing multiple pricing actions that significantly impacted consumer behavior and retail dynamics. Categories initially projected to remain flat instead fell by 2–3 points, while some major retailers shifted from direct imports to domestic fulfillment. Competitive pricing responses were delayed, and certain international markets faced secondary tariff effects.

Newell remains cautious, as the company expects core sales to be in the range of down 2% to flat for 2026. The company expects a weak first quarter, projecting core sales to decline 7% to 5%. However, performance is expected to improve from the second quarter of 2026 as innovation and distribution gains begin to take effect.

The company began its turnaround strategy in the summer of 2023, which includes hiring brand management teams and overhauling its innovation pipeline. These efforts are now culminating in a comprehensive wave of innovation launching across all business units this year. Notably, 25 Tier 1 and Tier 2 innovations are set to launch the highest number recorded. Every business unit is contributing to this rollout, marking a significant milestone in the company’s innovation strategy.

Specific brands are already gaining momentum, with Graco becoming the #1 selling baby item in the United States, driving a 350 basis point market share gain for the Baby business. Yankee Candle’s relaunch also delivered 6% U.S. core sales growth in the fourth quarter, highlighting the impact of strong innovation and marketing.

While the significant headwinds persist, including a $150 million total gross P&L impact from tariffs, the company announced a global productivity plan expected to generate about $75 million of year-over-year savings. Given weak near-term core sales guidance and tariff pressures, caution remains warranted, though innovation momentum and productivity savings could support a gradual recovery.

The Zacks Rundown for NWL

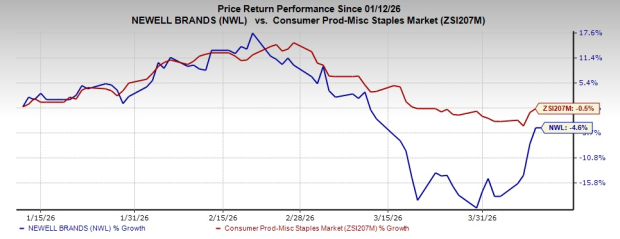

Shares of this Zacks Rank #3 (Hold) company have lost 4.6% in the past three months compared with the industry’s decline of 0.5%.

Image Source: Zacks Investment Research

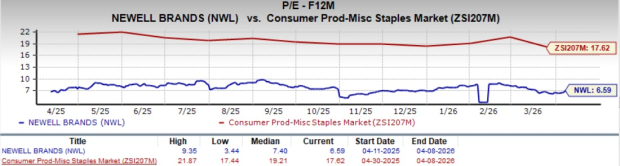

From a valuation standpoint, NWL trades at a forward price-to-earnings ratio of 6.59X, lower than the industry’s average of 17.62X.

Image Source: Zacks Investment Research

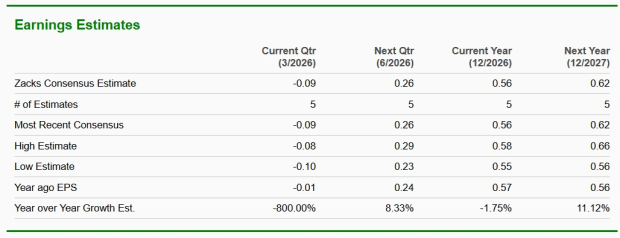

The Zacks Consensus Estimate for NWL’s current fiscal year earnings implies a year-over-year decline of 1.8%, and the same for next fiscal year earnings estimate implies year-over-year growth of 11.1%.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks have been discussed below:

Krispy Kreme, Inc. DNUT produces doughnuts in the United States, the United Kingdom, Ireland, Australia, New Zealand, Mexico, Canada, Japan, and internationally. At present, DNUT sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for DNUT’s current fiscal-year sales implies a decline of 6.8%, and the same for earnings implies growth of 50% from the year-ago reported figures. DNUT delivered a trailing four-quarter earnings surprise of 14.6%, on average.

ARKO Corp. ARKO operates a chain of convenience stores in the United States. ARKO currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for ARKO's current fiscal-year sales implies a decline of 4.9%, while the same for current fiscal-year earnings implies growth of 73.3% from the year-ago reported figures. ARKO delivered a trailing four-quarter earnings surprise of 36.5%, on average.

Kenvue Inc. KVUE operates as a consumer health company in the United States, the rest of North America, Europe, the Middle East, Africa, the Asia-Pacific and Latin America. KVUE currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for KVUE's current fiscal-year sales and earnings implies growth of 2.9% and 1.9%, respectively, from the year-ago actuals. KVUE delivered a trailing four-quarter negative earnings surprise of 9.8%, on average.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpNewell Brands Inc. (NWL) : Free Stock Analysis Report

ARKO Corp. (ARKO) : Free Stock Analysis Report

Krispy Kreme, Inc. (DNUT) : Free Stock Analysis Report

Kenvue Inc. (KVUE) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.