Tracking the Energy Transition Economy

Lithium is becoming cheaper as innovations lower the cost to produce it and investigations into battery electric vehicles (BEVs) import subsidies in the European Union lower demand. While this spells short-term disaster for the price of lithium - as we have seen throughout 2023 - there are claims that the demand for lithium will increase five-fold over the next decade as we continue our transition to clean energy. The Nasdaq Sprott Lithium Miners Index (NSLITP™) is uniquely situated to benefit from the continuation of the energy transition and the current dynamics of the growing lithium industry, while largely shielding investors from the volatility of direct investment into the commodity.

Mining Lithium

Lithium is found in salt flats (salars), hard rock minerals, underground aquifers, and other geological deposits concentrated in Chile, Australia, China, and Argentina. There are two primary methods to extract lithium. The first is hard rock mining through either open-pit or underground mining, typically of spodumene, a lithium-rich mineral, which is then processed through beneficiation, roasting, and leaching. The second is lithium brine extraction which involves drilling into salars, pumping the lithium-rich brine to the surface, and then removing impurities through evaporation. Several mining companies are engaging in direct lithium extraction, which is similar to brine extraction but without the need for evaporation ponds. Chile and Argentina primarily focus on brine extraction while Australia mostly engages in hard rock mining; China participates in both.

Use Cases of Lithium

74% of all lithium extracted is used to manufacture lithium-ion batteries which are essential to portable electronics (smartphones, laptops), electric vehicles, and energy storage systems. This is a large concentration in a single use case, but lithium-ion batteries are critical to developing key technologies and there is no current substitute for lithium's use within them. There is ongoing research into lithium and lithium ion battery substitutes such as sodium-ion and potassium-ion. Still, both have lower energy density and cycle life (the number of times a battery can be recharged before its effectiveness significantly degrades). Lithium's lightness compared to other metals, relative abundance, and high thermal conductivity lend itself to being a critical metal for energy transfer and storage.

The pie chart below shows the division of global end-use markets for lithium. While it is primarily used to manufacture batteries, it also is used in ceramics and glass to increase durability and to develop lubricating greases that can withstand environments with large temperature ranges.

Source: United States Geological Survey, 2022

Regulatory Woes

With lithium so heavily intertwined in the renewable energy transition, heavy involvement from governments in the form of subsidies and regulation should not be surprising. In April, the Chilean government decided to partially nationalize Chile's supply of lithium. Several locations in Chile -most notably the Salar de Atacama, which produces 25% of the world's battery-grade lithium- have been designated as strategic assets.

Therefore, going forward any commercial development will reguire a partnership with a state entity holding a majority stake. This is part of the broader trend of nationalization of minerals in the Global South. In 2022, Mexico nationalized its lithium supply to prevent foreign exploitation. Mexico has acted on its nationalization, canceling several contracts held by the Chinese firm Ganfeng Lithium. In contrast, Chile reached a preliminary agreement with SQM, the second-largest lithium mining company, to extend its contract for three decades in return for a majority stake being given to Codelco, a state-owned mining company, showing that it may be more open to additional contracts that are structured similarly.

To protect market share in the EV market, the European Union recently opened an inquiry into the subsidization of imported EVs, specifically from China. In the 2010s cheap Chinese imports hollowed out the domestic European manufacturing of solar, and Europe is still struggling to gain back market share. Mirroring the trend from last decade, there has recently been an influx of cheap, Chinese-manufactured EVs into the EU. The European Union removed subsidies from the solar industry too late. The EU is still attempting to gain back market share from China in the solar industry and it is trying to prevent something similar from happening within the EV market - - and by extension the lithium market.

Nasdaq Sprott Lithium Miners - Index Characteristics

Nasdaq Sprott Lithium Miners (NSLITP) is designed to track companies that produce, develop, and/or explore for lithium, and are classified as such by Sprott. Producers primarily extract lithium; developers prepare mines for production; and explorers are. companies that primarily prospect for lithium. For a security to be eligible for the index, it must have a free float market capitalization of at least $40 million (USD), have at least three months of trading history, and at least $100,000 (USD) three-month average daily traded value. For a security to remain in the index, it must have a free float market capitalization of $25 million (USD) and at least a $50,000 (USD) three-month average daily traded value.

NSLITP's weighting scheme is a theme-modified free float market capitalization. First, Sprott gives each eligible security an intensity score. The intensity score is the percentage of a company's revenue attributed to lithium production, development, and/or exploration. If a company either has no revenue - or if, in some rare cases, revenue is an inappropriate characteristic for a company - then the intensity score is set to 50%. Companies with an intensity score of less than or equal to 50% are given an adjusted market capitalization by multiplying their free float market capitalization by the intensity score; companies with an intensity score greater than 50% remain unadjusted.

The initial weights are then adjusted to meet the following constraints:

- For each of the securities with initial weight <= 0.3%, set the minimum weight to 0.3%.

- For each of the securities in the top 5 by initial weight, cap the maximum weight to 9.75%.

For each of the securities with an initial weight >0.3% and not in the top 5 by initial weight, set the weight between (0.3%, 4.75%). - In the event the sum of securities' weights that have theme intensity scores between 25% - 50% exceeds 15%, their aggregate weights are reduced down to 15%, with the individual securities weights being distributed pro rata by their previous weights. The excess weights are redistributed to all other securities that have not already reached a maximum-security weight threshold.

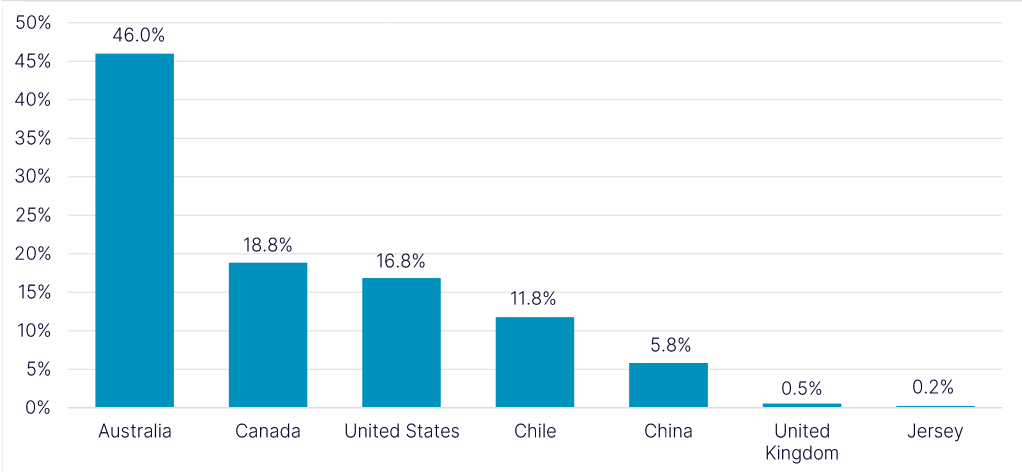

Index Composition by Geography

The lithium industry is largely concentrated in Australia, while the largest lithium reserves are in Chile. As mentioned previously, Chile nationalized their lithium supply in April so despite having the largest reserves, there are now logistical challenges in extracting those reserves. The Nasdaq Sprott Lithium Miners Index reflects this. As shown below the largest exposure by geography is Australia by a significant margin, followed by Canada, the United States, Chile, and China.

Source: Nasdaq Global Index Watch, Data as of 11/30/2023

NSLITP Total Return Performance vs. Lithium Commodity Markets

The below chart compares the returns of Nasdaq Sprott Lithium Miners to United States Lithium Carbonate 99.5% FOB (Bloomberg Ticker: L4US995D AMTL Index). As can be seen, the direct purchase of the commodity lithium outperformed SLIT over the first two years of our study, beginning in December 2020. However, the level of volatility of the direct purchase of lithium is significantly higher than that of NSLITP. Lithium carbonate has a volatility of 61.11% versus SLIT's volatility of 39.09%. Additionally, while NSLITP is down -26.52% in 2023 YTD, lithium carbonate is down -74.58% -- which may be an unacceptable level of risk for most investors. SLIT and lithium are weakly correlated with a correlation of only 17% based on nearly three years of weekly returns data.

Source: Nasdaq Global Index Watch, Bloomberg Data as of 11/30/2023

NSLITP vs. Competitor Indexes

We've shown why NSLIT may be a more reasonable solution for most investors' portfolios as opposed to a direct investment into the commodity. Now we will compare SLIT to another similar-sounding competitor index. Due to the nature of the lithium market over the past couple of years, several things are clear. In the longer term, NSLITP has been able to capitalize on the rapid growth of the lithium market, and in the shorter term, NSLITP has been able to limit downside.

Source: Nasdaq Global Index Watch, Bloomberg Data as of 11/30/2023

The Solactive Global Lithium Index (SOLLIT) has somewhat outperformed SLIT over the past year, but has not been able to capitalize on the longer-term uptrend; its trailing 3-year returns are negative. NSLITP follows the lithium market more closely than SOLLIT. This is largely due to the differences between the NSLIT and SOLLIT methodologies. SOLLIT is purely market capitalization weighted, meaning that companies that are only tangentially related to lithium production, prospecting, and innovation can be large holdings only due to their size. Additionally, SLIT focuses explicitly on the early stages of the lithium lifecycle (prospecting, mining, and processing the material) tying it more closely to the movement of lithium prices. By incorporating the intensity score of a company into its weighting scheme, SLIT adds an additional dimension and can track the lithium market with greater precision. This is evidenced by the relative correlation between NSLITPT, SOLLIT, and L4US995D. While NSLITPT is only loosely correlated to lithium, SOLLIT is practically not correlated with lithium at all, with a reading of - 01.

Index Composition by Sector

As a result of the intensity scoring and differences in the universe of eligible companies, there is a significant divergence in the sector concentration of these two indexes. Starting at the ICB Industry level we can already see differences. SLIT is almost completely concentrated in basic materials while SOLLIT has decent-sized holdings in Financials, Consumer Discretionary, and Consumer Staples. If we dig a couple of levels further down, we can start to see separation in SLIT but still a very heavy concentration in General Mining. NSLITP leans much more heavily towards mining operations (as defined by ICB Subsector) simply because the further away from lithium extraction a company sits, the lower their intensity score tends to be. Note that "Other" includes any subsector where both indexes hold less than 2%.

Source: Nasdaq Global Index Watch, Bloomberg, Data as of 11/30/2023

Due to numerous large companies utilizing lithium somewhere in their supply chains - but not necessarily generating most of their revenue from lithium activities - SOLLIT has excess weight in tangentially related subsectors. For example, the large exposure in Automobiles is largely due to a holding in Tesla, which does use lithium as a critical material in the manufacturing of its car batteries, but is not producing, developing, or exploring for lithium itself. Combining the lack of an intensity weighting system with a much larger starting universe leads to companies that are only moderately related to lithium production being heavily overrepresented in SOLLIT.

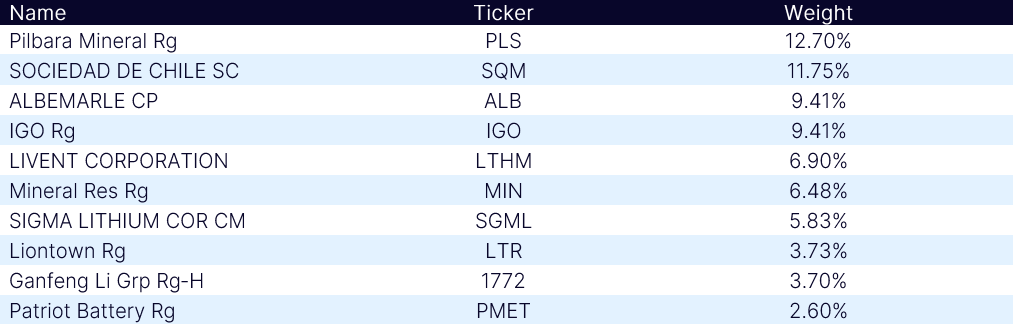

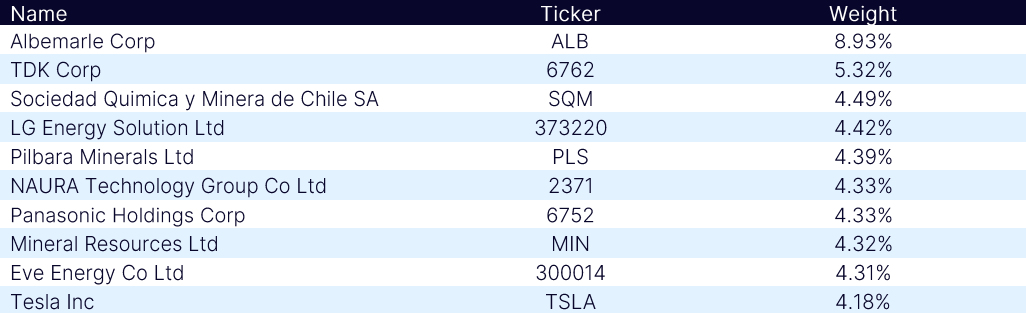

NSLITP vs. SOLLIT: Top 10 Holdings

NSLITP Top 10 Holdings:

Source: Nasdaq Global Index Watch, Data as of 11/30/2023

SOLLIT Top 10 Holdings:

Source: Bloomberg, Data as of 11/30/2023

Above are NSLITP's and SOLLITs top holdings by weight. The two largest holdings in NSLITP are located in Australia and Chile respectively. In contrast to SOLITT, every member of the top ten holdings of NSLITP is directly involved in the business of lithium mining and production.

Conclusion

NSLITP tracks the lithium market with enough correlation to participate in a strong, long-term uptrend, but limited enough that its downside volatility is only about one-third of the underlying commodity in 2023. While the short-term narrative for lithium has stumbled, the long-term investment thesis remains intact. As we transition to renewable and alternative energy systems, lithium will continue to be necessary to help facilitate energy storage and processing. The demand for lithium is not going away anytime soon, and NSLITP is well positioned to provide relevant equity exposure to a crucial component of the ongoing energy transition.

ETFs currently tracking the NSLITP Index include the Sprott Lithium Miners ETF (Nasdaq: LITP).

Sources: Nasdaq Global Index Watch, Bloomberg, Reuters, United States Geological Survey

Disclaimer:

Nasdaq® is a registered trademark of Nasdaq, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company.

Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED.

© 2024. Nasdaq, Inc. All Rights Reserved.