Shares of MGIC Investment Corporation MTG closed at $25.30 on Tuesday, near its 52-week high of $25.93. Solid insurance in force, a decline in loss and claims payments, lower delinquency, better housing market fundamentals and prudent capital deployment are driving the price higher.

Given the strong purchase market and potential share gains from the Federal Housing Administration, MGIC Investment expects strong premium writing. Increased persistency rate should continue to boost insurance in force.

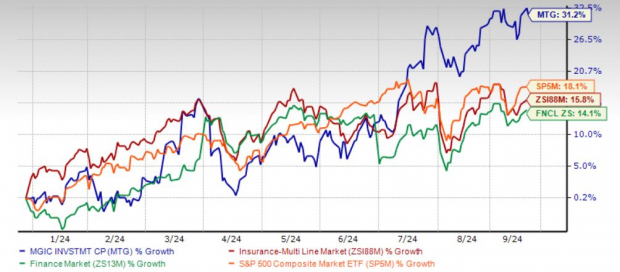

Shares have gained 31.2% year to date, outperforming the industry’s increase of 15.8%, the Finance sector’s rise of 14.1% and the Zacks S&P 500 composite’s increase of 18.1% in the said time frame.

MTG Outperforms Industry, Sector, S&P 500 YTD

Image Source: Zacks Investment Research

MTG shares are trading well above the 50-day moving average, indicating a bullish trend.

MTG’s Northbound Estimate Revision Instills Confidence

All three analysts covering the stock raised estimates for the current and next year. The Zacks Consensus Estimate for MTG’s 2024 and 2025 earnings has moved 2.2% and 1.5% north, respectively, in the past 30 days, reflecting analyst optimism.

MTG’s Return on Capital

Return on invested capital in the trailing 12 months was 11.4%, better than the industry average of 2.4%, reflecting MTG’s efficiency in utilizing funds to generate income.

Factors Acting in Favor of MGIC Investment

The insurance-in-force portfolio is set to grow, banking on new business and increasing annual persistency. A higher level of new and existing home sales, an increased percentage of homes purchased for cash and an improved level of refinance activity in an improving housing market should help this largest private mortgage insurer in the United States grow.

MTG has been witnessing a declining pattern of claim filings. A decline in loss and claims will strengthen the balance sheet and improve the insurer’s financial profile.

The insurer is improving its capital position with capital contribution, reinsurance transactions and cash position. Both leverage and times interest earned ratios have been improving.

A solid capital position supports MTG in wealth distribution. The company currently has $724 million remaining in its authorization kitty through December 2026. Its share repurchase activity reflects continued strong mortgage credit performance.

MTG’s Optimistic Growth Outlook

The Zacks Consensus Estimate for 2024 earnings is pegged at $2.76 per share, suggesting an increase of 9.1% on 4.7% higher revenues of $1.2 billion. The consensus estimate for 2025 earnings per share is $2.76, flat year over year on 4.6% higher revenues of $1.3 billion. The long-term expected earnings growth rate is 6.8%.

MTG Shares Are Undervalued

MTG shares are trading at a price-to-book multiple of 1.28, lower than the industry average of 2.60. Its pricing, at a discount to the industry average, gives a better entry point to investors.

Shares of other insurers like Radian Group RDN are trading at a multiple lower than the industry average, while that of Arch Capital Group ACGL are trading at a multiple higher than the industry average.

Parting Thoughts

MTG has been seeing improving housing market fundamentals, such as household formations and home sales and the current capital status. Higher premiums, outstanding credit quality and new business will continue to induce growth for MCIG.

The latest 13% increase in its quarterly dividend to 13 cents per share marked four straight years of dividend increases at a compound annual growth rate of 21%. Its current dividend yield is 2.1%.

Given its attractive valuation and upbeat prospects, this Zacks Rank #1 (Strong Buy) mortgage insurer is a strong contender for addition to one’s portfolio.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks Names #1 Semiconductor Stock

It's only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>MGIC Investment Corporation (MTG) : Free Stock Analysis Report

Radian Group Inc. (RDN) : Free Stock Analysis Report

Arch Capital Group Ltd. (ACGL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.