Credit: Shutterstock photo

Credit: Shutterstock photoBy Andrew Gracey :

Background

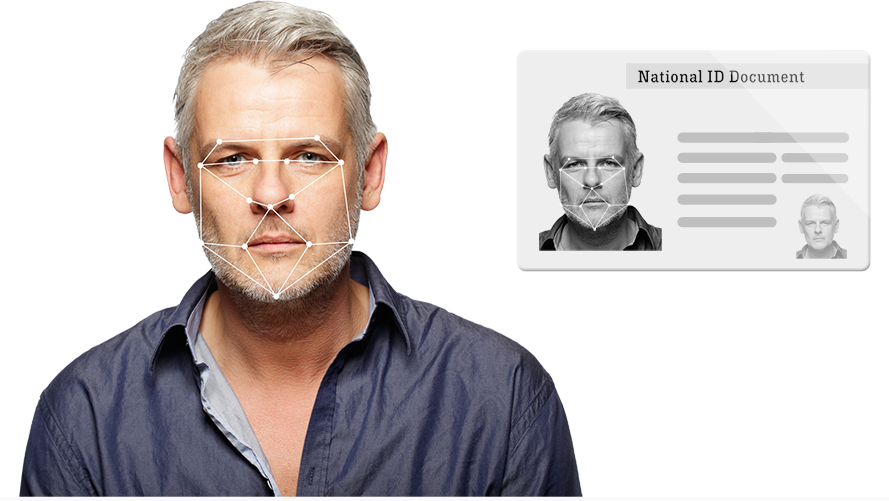

Mitek Systems ( MITK ) is the leading US provider of smartphone check deposit technology with its Mobile Deposit software product sold to retail and commercial banks. Mitek's other mobile products include technology which extracts information from drivers' licenses to pre-fill application forms (Photo Fill) and pure identity verification and authentication products (Photo Verify, IDchecker). The vast majority of today's revenues and valuation are attributed to the Mobile Deposit product.

Mitek had 4105 licensed Mobile Deposit bank customers as at June 30, 2015, which accounted for over 50% of all US banks. The company estimates 50 million customers have used their Mobile Deposit product. Investors need not get too excited around the number of banks signed up rather it's the size of the customer base and rate of consumer adoption that drives Mitek's profitability. The dominance of Mitek is nicely illustrated by the top 10 retail banks all using Mobile Deposit.

Mitek plans to use its strength in Mobile Deposit to expand into the identity verification and authentication market, with the recent $10.5 million acquisition of IDchecker accelerating this move. I'm yet to be convinced on the commercialization strategies for the verification and authentication products but the company believes the combined businesses gives them access to a $1.6 billion market.

Mitek has frustrated investors around the pace its quickly growing 4000+ US banking customer base has translated into Mobile Deposit revenue and profit growth. Investors are also concerned around the structural decline in the use of checks in the US. The good news is Mitek has already carved out a profitable Mobile Deposit business with GAAP earnings per share of 3 cents in the June 2015 quarter. Non-GAAP quarterly earnings of 7 cents included the adding back of acquisition costs, litigation and stock compensation expenses.

These annualised earnings places the company on an attractive 2015 earnings multiple; however, the company is a serial litigator so adding back full legal costs in arriving at GAAP earnings per share is probably too generous. It is however encouraging to see favourable earnings revenue momentum with Mitek giving revenue guidance for the first time in 2015 and upgrading this guidance soon after.

Drivers of June 2015 quarterly improvement vs. June 2014

- Software revenue +47% with the delta being growth of check transaction revenue.

- Services revenue +19% mostly attributed to growing maintenance revenue.

- Total revenue +38%.

- Cost of goods fall from 13% to 9% due to higher sales and less embedded third party software.

- Gross profit margin rises from 87% to 91%.

- Sales & Marketing percentage of Sales falls from 39% to 26% due to higher sales through channel partners.

- Research & Development percentage of Sales falls from 34% to 21% due to higher sales and cost reductions.

- Administration percentage of Sales falls from 49 to 28% due to higher sales and lower litigation expenses.

The rolling 12-month revenues were up 26% with June quarterly revenue growth accelerating 38%. The quarterly license and maintenance software revenue was up an impressive 47% indicating Mitek's business model is finally reaching critical mass, driven by growth in consumer adoption driving recharges.

The company guided $23 million of revenue in April for its September 2015 financial year, which was upgraded to $24 million in July. Backing out expected revenues from IDchecker, Mitek raised their second half revenue guidance by over 6%.

Investors ultimately don't want a one-trick Mobile Deposit pony. They want to see greater product breadth through Mitek leveraging their blue-chip banking relationships into other mobile product areas like identity and authentication going forward.

Business Model

There is little transparency or detailed explanation around how Mitek charges for its Mobile Deposit product, nor the revenue splits between Mitek and channel partners. Mitek's business model is largely built around a fixed charge per check processed which was mooted on Seeking Alpha to be 10 cents per transaction (I have assumed 8c), albeit channel partners including the likes of Cachet, Ensenta, Fiserv, FIS and NCR will be clipping this ticket.

Investors can take some comfort that pricing appears to be holding which is perhaps symptomatic of the structural decline in the check market. Mitek's transaction based pricing model has clearly been attractive to US banks given Mobile Deposit's impressive penetration into the top 50 banks.

The Mobile Deposit product economics are strong with channel partner NCR reporting the average cost of processing a check using Mobile Deposit was 14 cents against ATM costs of 60 cents and a branch cost of $3.75.

Mitek assigns an agreed number of Mobile Deposit transactions upfront when customers sign an initial software license agreement. Mitek receives an initial license fee followed by recurring annual maintenance fees. Maintenance fees are struck at 18% of the initial license fee and are becoming an important revenue stream for Mitek. There are small amounts of professional services revenue, with the systems integration work largely undertaken by channel partners. Bank customers and/or channel partners acquire a bundle of bank deposit transactions and once exhausted they recharge.

It's the timing of these license fees, recharges and maintenance revenues that has caused lumpiness in revenue and profitability historically. Going forward, maintenance and the Mobile Deposit recharges are the drivers of revenue and profitability.

I surmise that customer adoption of Mobile Deposit takes 2 years before reaching decent transaction volume. I see adoption following an S-Curve pattern with both Mitek and their banking customers overestimating short-term uptake meaning its takes longer before recharge transaction revenue is generated.

There is little consistency in the size of the Mobile Deposit bundles so investors don't get a consistent read-through from the number of renewals reported in any one quarter.

It's probably fair to say the company doesn't make it easy for investors to fully understand the business model. Mitek has recently started to give revenue guidance, which is reflective of improved revenue transparency as the business has more scale with higher maintenance revenue and more consistent transaction recharges. There seems to be good evidence consumers are using the Mobile Deposit product more and this forms the basis of our investment rationale.

Discussion on Mobile Deposit - Consumer Adoption and the US Check Market

Deep diving into some of the drivers around the US mobile deposit market, the important Mitek customer Bank of America ( BAC ) quoted in 2014 that Americans were depositing an average of 170,000 checks per business day or 44.2 million checks per year. Bank of America said in March 2015 that mobile check deposits in their network were up 30% on the previous corresponding period , while Chase also reported 30% growth in June 2015 . The Federal Reserve's Consumer and Mobile Financial Services 2015 report (March 2015) reported 51% of mobile phone banking users had made a remote deposit in 2014 vs. 38% in 2014 indicating annual growth of 34%. These growth rates are all consistent with what Mitek has been alluding to.

This 51% of mobile phone banking statistic should be viewed in the context of only 39% of mobile phone users actually having adopted any mobile banking services by 2014. This 39% is still a relatively low rate of consumer adoption and essentially represents the addressable market for Mobile Deposit in the US. The key take home being the addressable market for Mobile Deposit increased 18% in 2015 alone.

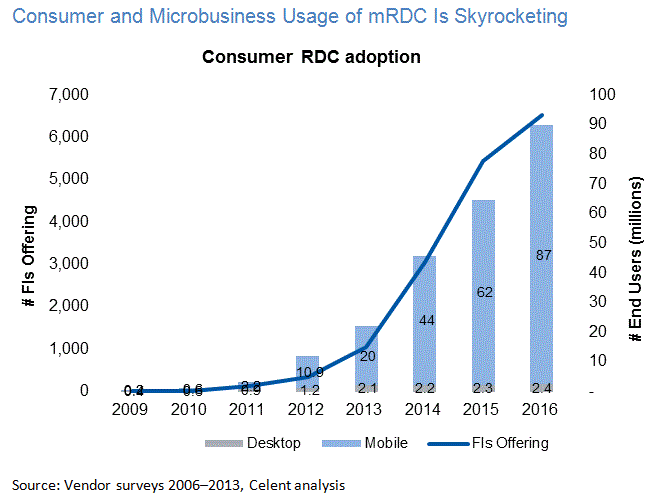

I believe we can expect more widespread adoption of consumer mobile banking services with research and consulting firm Celent pointing to sky rocketing adoption of mobile remote deposit capture (mRDC) . The number of transactions processed by Mobile Deposit is a function of the consumer adoption of the technology, the addressable market and the number of times per consumer the service is used annually. The offsetting factors include the volume of checks being written in the US is declining.

The Federal Reserve 2013 Payments Study showed the number of checks written in the US was 18.3 billion which had fallen 9.2% per year between 2009-2012. There is little reason to expect the decline in the number of transactions paid by checks has not accelerated. If one conservatively assumes the rate of decline accelerates 5% per year then the volume of consumer checks being deposited in the USA may sit around 9.6 billion in the calendar year 2015.

The same report showed the volume of checks deposited by image in 2012 was 3.4 billion (17% of all check deposits) with businesses depositing 93% and consumers just 7%. Businesses have been depositing checks using computer image technology for over a decade while Mitek launched their remote deposit consumer product in 2008, but only got real traction after 2012.

In 2012, consumer mobile deposits accounted for 0.6% of total check deposits, which implies 114 million checks were deposited through mobile in 2012. I believe consumer check deposits may now account for 6% of the market. This number was crudely derived by compounding this 114 million checks by the quarterly quantitative comments around Mitek's Mobile Deposit growth.

Consumer check deposit growth has been strong albeit slowing and there may be 573 million checks deposited in the US through mobile devices in calendar year 2015. This volume of checks processed in 2015 at 8 cents per check (gross) and Mitek Systems dominating (65% market share) the consumer market, broadly reconciles with my valuation model below.

Valuation

I'm happy to focus 90% of my valuation on Mobile Deposit, which is essentially driving the majority of the current revenues, cash flow and profitability. I am implicitly assuming that Mobile Deposit represents 100% of the historical free cash flow generation while the combined value of the identity products Photo Fill, Photo Verify and the recent acquisition IDchecker are valued at $10.5 million, which is in line with the total cash and scrip price paid for IDchecker.

The IDchecker business generated just $121K revenue in the June 2015 quarter, so Mitek is largely buying intellectual property in the identity and facial recognition technology space. Mitek guiding that the group operating expenditure will rise to $5.5 million in the September quarter, up from $4.8 million in June. Simplistically, this suggests IDchecker is losing $2.3 million at the operating profit level in the 2016 financial year.

The combined Mitek identity products will be a drag on reported profitability in 2016 and 2017, but the IDchecker acquisition appears a logical extension to the existing identity business, which rationally could become profitable in the future. I don't believe penalizing the Mitek valuation for this loss making business is sensible and will keep it at book value for the time being. This forms the rationale for using a sum of the parts valuation in valuing Mitek.

Investors today are getting a dominant and cash generative US business in Mobile Deposit, which has a few years of growth remaining in my opinion. Investors are getting $23 million cash in the bank, while I'm valuing all the identity products very conservatively at just the price paid for IDchecker or $10.5 million.

The following key assumptions drive the sum of the parts valuation model:

- Transaction software revenue growth of 30%.

- Maintenance revenue growth of 22%.

- Selling and Marketing costs falls from 25.4% to 25% of sales (2016).

- Research and Development costs rises from 21.7% to 22.5% of sales (2016).

- Administration costs fall from 31% to 25% of sales (2016).

- Shares on issue rising at current dilution rates from 31.9 to 32.9 million shares (2016).

- All Identity products including IDchecker valued at $10.5 million going forward.

- Cash in the bank $23 million (June 30, 2015).

- Ample tax losses mean no income tax will be paid in the foreseeable future.

- Losses associated with Identity products ignored (currently estimated at $2.3 million per year) and incorporated into $10.5 million book value.

- Model reconciles with estimated US market of consumer image deposits, using 8 cents gross per transaction, and 2 cents paid away to resellers, with Mitek having 65% market share.

The above table forecasts Mitek's Mobile Deposit revenues hit $31.1 million in 2016 with free cash flow generation of $8.9 million or cash earnings per share of 27 cents. I have recharges representing 75% of initial license fees & recharges by 2016 rising to 100% in 2017, as most of the US banks by volume have been already signed so initial license fees dry up.

The below metrics in my opinion suggest the Mobile Deposit business as a standalone easily justifies the capitalisation of Mitek Systems today with a 2016 valuation of $4.05. Investors can then add $0.76 for cash in the bank and $0.33 for Identity Products arriving at a sum of the parts valuation of $5.14 which is more than 50% upside.

The above valuation metric forecasts are all very credible. It's genuinely reasonable value paying just 2.7 times 2016 revenue for a software company, while a cash price to earnings ratio of 12.6 times for 2016 is cheap when compared to US listed peers.

In terms of valuation methodology valuing Mitek at 15 times 2016 free cash flow generation after accounting for share dilution seems very reasonable, especially in considering cash earnings per share is growing 20% in 2017.

The contentious part of the valuation is valuing the loss-marking part of the business or identity at the acquisition cost of IDchecker of $10.5 million or 33 cents. This part of the valuation can however significantly increase should these loss-making products start to gain commercial traction, so watch this space for news updates.

Mitek with its tentacles into over 4000 banks is very well positioned to provide a range of innovative mobile products to the banking sector in the future.

See also With Continued Insider Selling, Is It Time To Sell Patrick Industries? on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}