Credit: Shutterstock photo

Credit: Shutterstock photoNote: This article is part of the ETF Strategist Channel on ETF Trends .

By Micah Wakefield

Everybody loves math, right? Such an exciting topic, said very few people ever. Many schoolchildren dislike math because they think it's boring and they'll never use it in the real world. I know I felt that way as a kid. This feeling generally changes somewhat for kids as they grow older and they start to have to deal with bills, paychecks, taxes, and investments. Math starts to matter.

Whether you enjoy math or not, math and statistics are key components of some of the most common and longstanding concepts in investment management such as standard deviation, the efficient frontier, correlation, and asset allocation. But for many, understanding all the math and statistics involved in investments can be a bit challenging at times and some simplification of the concepts of math is necessary.

Investors often feel this way as it relates to all things math and finance; "just please simplify it where I can actually understand it." There is a need today to break down and simplify some of the important math concepts in finance and especially equity investments in order to be able to grasp and understand how they can be applied to investing.

This is a challenge in today's environment, as there seems to be an engrained mindset amongst most investors today toward equity investments and returns; perhaps formed by a lack of understanding about how mathematical principles impact investing. What is this engrained mindset that most investors have today? They tend to get stuck on return, especially near-term return. This is apparent from their expectations, reactions, emotions, and choices when it comes to investing. Shortsightedly, it's usually the first and last thing that is considered when making investment decisions.

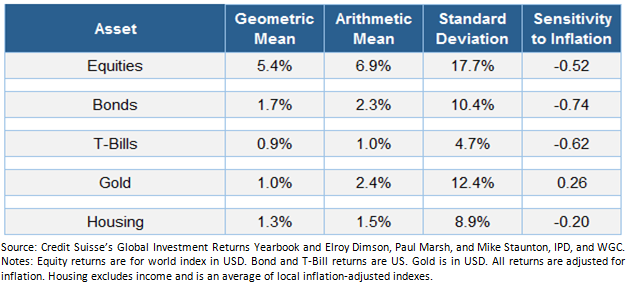

Although we know that there are other asset classes to consider besides equities, it is still a widely accepted practice for equities to be a large portion of investor's portfolios. Almost all portfolio allocations have at least 30% to 90% in equities, from conservative to aggressive investors. For hundreds of years, investors have looked to equities to provide growth and to help offset inflation, achieve their financial goals, and prepare for retirement. This is because, over the long-term, equities have provided relatively good growth despite high volatility and downside risk.

So if equities is a good place for investment growth over the long-term, but also one of the more volatile asset classes as seen above, how should someone invest in equities and is there any approach that mathematically gives some advantages to the investor?

This topic is the focus of Swan's latest white paper that seeks to simplify four important mathematical principles that investors need to understand in order to change how they view equities, investment returns, and what drives their equity decisions. It also reviews four different ways to invest in equities and how these mathematical principles apply to these equity approaches.

If investors understand and focus on these four mathematical principles instead of just on return and short-term outcomes, they might make better, more informed decisions as it relates to their equity investments or their investments in general. The four principles are:

- The importance and power of compounding returns

- The importance of avoiding large losses

- The importance of variance drain

- The importance of distribution of returns

Let's take a brief look at one of these principles, variance drain.

Volatility drag, also known as variance drain, is the drain that occurs from the arithmetic return to the geometric return from volatility. Arithmetic average is just referring to the simple sum of each occurrence of return, divided by the total number in the series. Geometric or compound refers to geometrically linking each return to the next and compounding the returns.

Lowering volatility is key to achieving better compound growth as volatility diminishes the rate at which an investment grows over the long-term. When two investments with the same average return are compared, the one with the greater volatility, or variance, all other things being equal, will have a lower compound return.

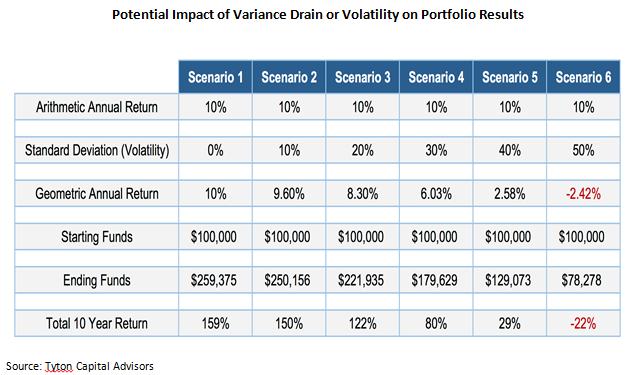

This table shows 6 different scenarios, all having an arithmetic annual return of 10%. However, each scenario has a 10% increase in its volatility of returns. Notice the drain on the geometric annual return and the ending dollar value as the volatility increases.

Obviously, averages don't tell the full story. The S&P 500 has averaged roughly 9.5% per year since 1928. You would want that investment, right? Especially in the current market environment, 9.5% sounds pretty great. But how many years did the market actually have a return in the 9%-10% range? The answer might surprise you. Over the last 87 years, in only 2 years was the market near its long-term average returning 9 or 10% and only 4 years within 2% of its long-term average - that's only 5% of the time (Source: Morningstar). More often than not the market's return in any given year was much greater or much lower than 9.5%. And that is the problem with averages and focusing on them. Averages, by their very nature, mask volatility.

Of course, in reality, not everyone wants an investment that grows at an "average" 9.5% if it involves multiple -40% to -80% drawdowns and sometimes decades of negative return in order to get there, as has been seen with the S&P 500. This type of ride makes it very difficult for investors to stay the course and actually achieve that return and sequence of returns or withdrawal risk also becomes a bigger factor.

Swan believes these basic mathematical principles are mostly misunderstood or overlooked by many investors today. It is of vital importance that investors study and understand the mathematical principles behind investment returns in order to have proper expectations for their investments and to help them find the best possible solutions for reaching their financial goals. At Swan, we believe that an ETF-managed solution like our hedged equity Defined Risk Strategy (DRS) has some mathematical advantages to traditional equity. By seeking to avoid large losses and lower volatility, the DRS looks to take advantage of these mathematical principles and their important impact on long-term results.

We believe that the majority of an investor's portfolio should be structured to avoid large losses, not exposed to undefined risk. No matter the portfolio construction though, we want to help investors think outside the box and expand their mindset past focusing on short-term returns by simplifying difficult mathematical concepts to a more understandable level.

Swan's efforts to expand investor's understanding of how math impacts their portfolios is explored in further detail in a piece titled "Math Matters: Rethinking Investment Returns and How Math Impacts Results". Both an executive summary and comprehensive version are available.

Micah Wakefield is Director of Research and Product Developmentat Swan Global Investments , a participant in the ETF Strategist Channel .

Trending on ETF Trends

Housing Recovery - The Next Generation Joins In

Central Banks Policies… Everyone Gets a Trophy

International Portfolios: How Thoughtful Diversification Can Reap Bene...

Do ETFs and Moving Averages Mix?

Do Emerging Markets Equities Still Make Sense in a Diversified Portfol...

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

This article was provided by our partner Tom Lydon of etftrends.com.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.