MasTec, Inc. MTZ has been witnessing growth in its Pipeline Infrastructure segment since the beginning of 2025, with the third quarter showing incremental growth. This segment’s estimated 18-month backlog has been increasing in the first, second and third quarters by 45.1%, 82.5% and 123.8%, respectively, on a year-over-year basis. Increasing multi-year spending across grid reliability, LNG expansion and energy transition infrastructure is primarily fueling the growth of this segment.

During the third quarter of 2025, revenues in the Pipeline Infrastructure segment grew 20% year over year to $597.8 million. The growth resulted from its overcoming of the challenging comparisons regarding the MVP project. The segment’s EBITDA margin showed sequential growth of 390 basis points to 15.4%, paving the path for continued margin improvements in the fourth quarter and 2026. As this segment has historically been volatile, the current margin strength reflects genuine operational progress rather than one-off benefits.

Improved bidding discipline, a more favorable mix of midstream projects, better project execution and healthier backlog conversion are the key to the growth of MasTec’s Pipeline Infrastructure segment. Moreover, these aspects are faring well given the increasing government funding initiatives in favor of the energy, power and infrastructure markets.

If MasTec can maintain stronger execution while capitalizing on rising midstream investment, the pipeline rebound may be in its early innings. The 15.4% EBITDA margin may not just be a quarter’s outperformance, but a first signal directing toward MasTec’s most cyclical businesses turning the corner.

Market Competition for MasTec

In the pipeline infrastructure and broader energy market, MasTec competes from a position of scale and programmatic backlog strength. The key market players, including Fluor Corporation FLR and EMCOR Group, Inc. EME, offer it substantial competition.

Fluor occupies the opposite end of the spectrum on project complexity. Its century-long pipeline pedigree and full-service EPC capability let it pursue the largest and technically complex transmission, LNG and industrial energy transition projects where heavy civil, subsea and process integration matter. On the other hand, EMCOR is more focused on distributed electrical and mechanical work, facilities services and regional growth through targeted acquisitions. This offers the company with on-the-ground scalability for utility interconnection, solar balance-of-system and electrification projects where speed, local relationships and maintenance contracts drive repeatable revenues.

MTZ’s backlog and integrated execution win bundled midstream and interconnection work, Fluor’s engineering depth wins large brownfield and complex greenfield projects, and EMCOR’s service network captures distributed, O&M and retrofit flows.

MTZ Stock’s Price Performance & Valuation Trend

Shares of this Florida-based infrastructure construction company have gained 13.5% in the past three months, outperforming the Zacks Building Products - Heavy Construction industry, the broader Zacks Construction sector and the S&P 500 index.

Image Source: Zacks Investment Research

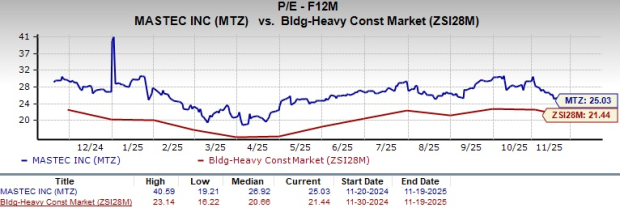

MTZ stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 25.03, as shown in the chart below.

Image Source: Zacks Investment Research

EPS Trend Favors MTZ

For 2025 and 2025, MTZ’s earnings estimates have trended upward to $6.35 per share and $8.06 per share in the past 30 days. The revised estimated figures for 2025 and 2026 imply 60.8% and 27% year-over-year growth, respectively.

Image Source: Zacks Investment Research

MasTec stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpFluor Corporation (FLR) : Free Stock Analysis Report

EMCOR Group, Inc. (EME) : Free Stock Analysis Report

MasTec, Inc. (MTZ) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.