Please see Running Oak's performance update and market commentary below. If you'd like a more thorough understanding of our approach and history, I was recently interviewed by Michael Gayed. Simply search for Michael Gayed on LinkedIn, X (formerly known as Twitter, aka the Prince of social media), and others.

Why Invest in Efficient Growth:

- Top 1 percentile: Running Oak’s Efficient Growth separate account has performed in the top 1% of all Mid Cap Core funds in Morningstar's database over the last 10 years, net of fees.1

- 5 Stars: Efficient Growth has a 5-Star Morningstar rating and received Morningstar's highest quantitative score of Gold.

- Since inception, Efficient Growth has provided 27% more return than the S&P 500 Equal Weight Index and 9% more return than the S&P 500 Total Return Index, given the same level of downside risk, gross of fees. (Ulcer Performance Index)*

Differentiated Approach and Construction

- Mid Cap stocks are at their cheapest in 25 years relative to Large. Efficient Growth provides significant Mid Cap exposure.

- Efficient Growth is built upon 3 longstanding, common sense principles: maximize earnings growth, strictly avoid inflated valuations, protect to the downside.

- Running Oak utilizes a highly disciplined, rules-based process, resulting in a portfolio that is reliable, repeatable, and unemotional.

How to Invest

- Efficient Growth is currently available as an SMA and ETF. (ETF specifics and SMA historical performance can't be shared in the same letter - sorry, it's annoying, I know. Please inquire for the ticker or more information.)

- In just 15 months, The ETF Which Shall Not Be Named has grown over 12,000% since launch – from 2 to 242mm.

Performance update:

Running Oak’s Efficient Growth portfolio was down -0.75%, gross of fees (-0.79%, net), in October versus -1.63% and -0.91% for the S&P 500 Equal Weight Index and S&P 500 Total Return Index, respectively.*

________________________________________

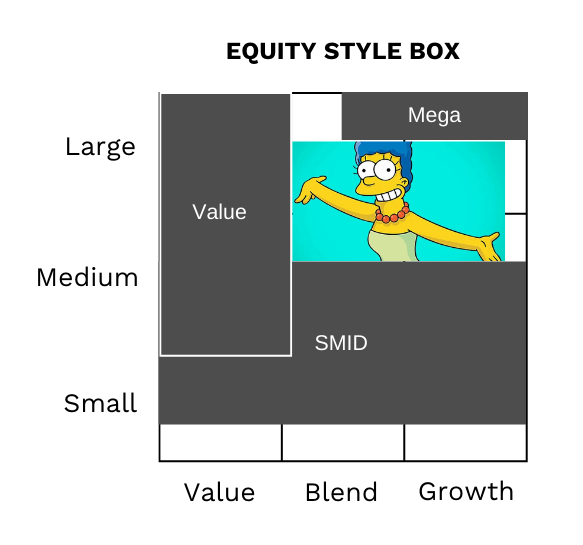

MARGE and in Charge

“Of all the crazy things you have done, this ranks somewhere in the middle” – Marge Simpson

Running Oak’s Efficient Growth strategy is built to be the Marge Simpson of your equity portfolio. Our investment philosophy is common sense (higher earnings growth, rational valuations, lower downside risk), just like Marge. Our investment process is rules-based and highly disciplined, making it repeatable, dependable, and unemotional, just like Marge. I don’t know if Marge was a top 1% performer, like Efficient Growth has been relative to its peers over the last decade, or if she outpaced the S&P 500, gross of fees, but she has exceptionally tall hair. Most importantly, Efficient Growth currently provides exposure to a forgotten, under-invested asset class: MARGE (Mid/Large). It’s “somewhere in the middle… of all the crazy things you have done.”

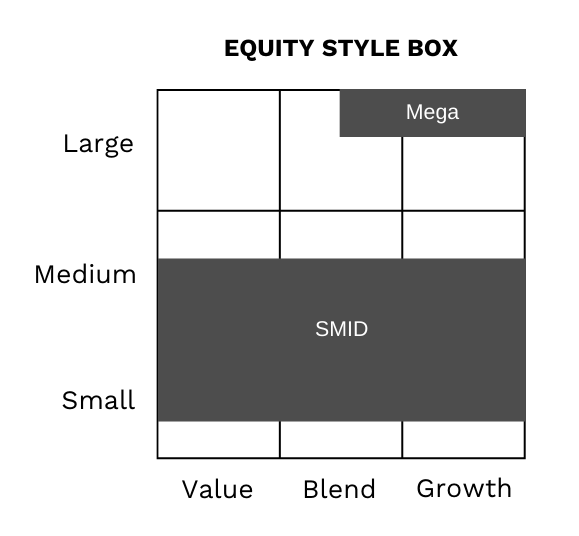

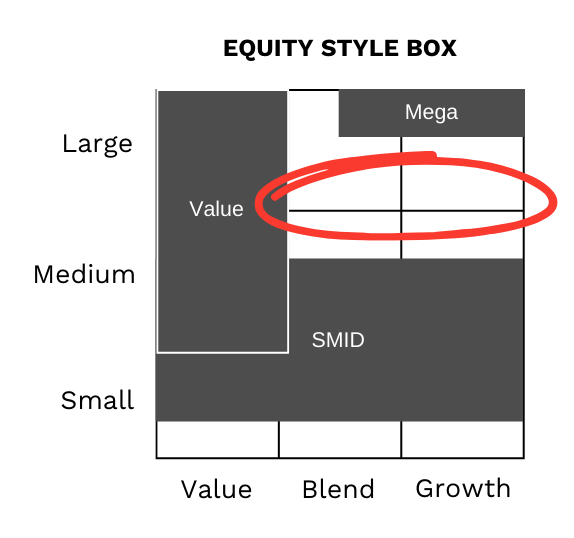

The average advisory client has significant Large Cap exposure, but – due to performance and popularity – much of that is concentrated in a handful of Mega Cap companies. That concentration leaves the smaller end of Large – where many sizable, proven, successful companies sit – under-invested, as illustrated below.

That Mega Cap investment is then often diversified with SMID (Small/Mid Cap), which typically falls at the larger side of Small and smaller side of Mid. Few investors have pure Mid Cap exposure, meaning upper Mid and lower Large are inadequately covered..

Clients are then further diversified with Value/Dividend strategies. Combining the most common allocations, a large gap appears PRECISELY WHERE YOU WANT TO BE INVESTED.

MARGE and in Charge: Running Oak's Efficient Growth portfolio fills that gap in client portfolios like few others. Our All Cap universe (primarily Mid/Large) is constrained only by a minimum market capitalization of $5 billion, enabling our rules-based investment process to systematically take us - and, more importantly, our clients - where the relative value and opportunity is. For the last several years, that has been MARGE, and that opportunity exists precisely because that gap exists. Under-investment means fewer dollars bidding up companies, which means more attractive valuations.

Case in point:

Fiserv, Inc (FI) - Fiserv is a $120B company. Many define Large Cap as companies with capitalizations above 10B. Morningstar has a far higher definition of 25B and above. Even using Morningstar's definition, Fiserv is almost 5x larger than the Large Cap cutoff. It's the 78th largest company in the S&P 500 with a weighting of... wait for it... 0.25%. That's 0.0025. Fiserv is larger than 85% of the companies in the S&P 500 - 85%, and S&P investors get exposure of just 0.25%. Investors have minimal exposure to this huge, well-run company that is up roughly 70% over the last 12 months.

Parker-Hannifin Corporation (PH) - Parker-Hannifin is a $90B company. It's well within Large Cap. PH is the 109th largest company in the S&P 500, larger than 78% of all companies in the S&P. PH's weighting is 0.18% or 0.0018. That's a lot of zeros for a company that is ALSO up 70% over the last 12 months.

These are perfect examples of MARGE that investors have roughly 0% exposure to. They're huge; they're extremely well-run; they're wildly profitable and growing, and most people own none.

"I’m not saying it’s a bad idea, I’m just saying... maybe a really bad idea?" - Marge Simpson

MARGE is precisely where you want to be invested today. The economy and equity market are as uncertain as any time I can recall, best illustrated by interest rates. Here's a brief timeline:

- Yield Curve Normalization - In late August/early September, the yield curve normalized (shorter dated bonds no longer offered higher yields than longer dated bonds). Normalization has accurately predicted every recession since 1970.

- Jumbo Cut - In September, the Federal Reserve cut interest rates by 50bps, which is known as a jumbo cut. Generally speaking, the Fed cuts rates when they believe a recession is likely or imminent.

- Subsequent Rise - The intent of cutting rates is for them to go lower. The 10-year yield went higher... pretty much every day after... for weeks... by a lot. In the words of Marge Simpson's husband, "Doh!"

- Another Cut - In November, the Federal Reserve cut rates again, this time by 25 bps. The 10-year yield, once again, rose but not by much.

In sum, anything can happen over the next few years. Those who like Donald Trump like that there's no telling what he'll say or do next. Those who dislike Donald Trump dislike that there's no telling what he'll say or do next. (Who says our country is divided? Everyone agrees!) If Donald Trump cuts taxes and significantly expands the budget deficit, that would be stimulative, likely resulting in economic expansion but also higher inflation and higher rates. If he cuts government spending considerably and enacts tariffs, that would be restrictive, likely leading to a recession and lower interest rates. It could really go either way.

MARGE and in Charge: Whether interest rates go higher or go lower or the US economy enters a recession or avoids one, MARGE is THE place to be. If interest rates rise, smaller companies will struggle. Roughly 50% of the companies within the Russell 2000 are currently unprofitable, and many don’t generate enough cash to meet their debt obligations. Higher rates for longer will hurt SMID.

Higher rates impact larger companies, like Mega Caps, less, because they were able to negotiate favorable rates and terms on their debt. Upper Mid, Lower Large Cap companies with low debt levels, such as those Efficient Growth invests in, will be impacted less, as well.

If interest rates decline, on the other hand, that ain’t good. Interest rates are most likely to decline due to a recession. Recessions and their accompanying bear markets are the environment in which the most popular, most overcrowded trades come back to reality; that’s Mega Cap. There has arguably never been a larger, hotter, more overcrowded trade, and according to our numbers, many of the Mega Caps are wildly overvalued. If the US enters a recession, those companies won’t simply decline to fair value and stop; they’ll go flying right through. (See Amazon and Netflix in 2022)

While declining interest rates benefit smaller companies for the reasons mentioned above, recessions certainly don’t. Smaller companies are riskier and typically perform poorly in a recession.

Meanwhile, MARGE – with its higher quality balance sheets, larger companies, and relative undervaluation – is likely to perform best.

"You’re learning many lessons tonight. And one of them is to always give your mother [aka Marge] the benefit of the doubt." – Marge Simpson

Allow Us to Introduce You

MARGE is complicated and nuanced. There's no one better to introduce you two. Efficient Growth has delivered top 1% returns versus its peers and outperformed the S&P 500 over the last decade, despite minimal exposure to the Magnificent 7 and being historically out of favor. Efficient Growth has provided the diversification that clients need, particularly at this moment, AND rare performance.

Efficient Growth will ALWAYS:

- Avoid over-valued companies - You don't want mean reversion working against you. The hottest companies very often become the coldest in a recession.

- Avoid over-leveraged companies - Debt is a double-edged sword that tends to turn on its wielder in a recession.

- Avoid over-concentration - Efficient Growth is equally-weighted, diversifying risk across companies and industries.

Efficient Growth’s philosophy is simple, easy to understand, and common sense:

- Above Average Earnings Growth – Because owning a company that is making more and more money is obviously a good thing.

- Attractive Valuations – Because paying a dumb price is, well, dumb.

- Lower Downside Risk – Because losing money stinks. Lower drawdowns mean smaller bounces are required to get back to new highs.

With just the slightest bit of critical thinking, one would theorize that Efficient Growth is likely to outperform due to higher earnings growth and investment in under to fairly valued companies and do so with less downside risk, due to the avoidance of overvalued, unprofitable, and insolvent companies. Efficient Growth would also never have almost 30% of the portfolio invested in just 6 highly correlated companies.

Running Oak's goal is to maximize the exponential growth of clients' portfolios, while subjecting them to far less risk of loss. In other words, we aim to help your clients realize their dreams and avoid their nightmares.

If you appreciate critical thinking, math, common sense, and occasional sarcasm, we would love to speak with you. Please feel free to set up a time here: Schedule a call.

Seth L. Cogswell, Founder and Managing Partner

4519 W 56th St | Edina, MN 55424

P +1 919.656.3712

For Institutional Use only, not for Public Distribution. For additional data and context regarding the claims made within this letter, please refer to the Disclosures and Additional Data document located here.

“All opinions expressed in this newsletter are those of Running Oak Capital’s and do not constitute investment advice.”

Investment Advisory Services are offered through Running Oak Capital, a registered investment adviser.

*Past performance is no guarantee of future results. Performance expectations are no guarantee of future results; they reflect educated guesses that may or may not come to fruition. All indices are unmanaged and may not be invested into directly.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments and strategies may be appropriate for you, consult with us at Running Oak Capital or another trusted investment adviser.

Stock prices and index returns provided by Standard & Poor’s.

Latest articles

This data feed is not available at this time.

Data is currently not available