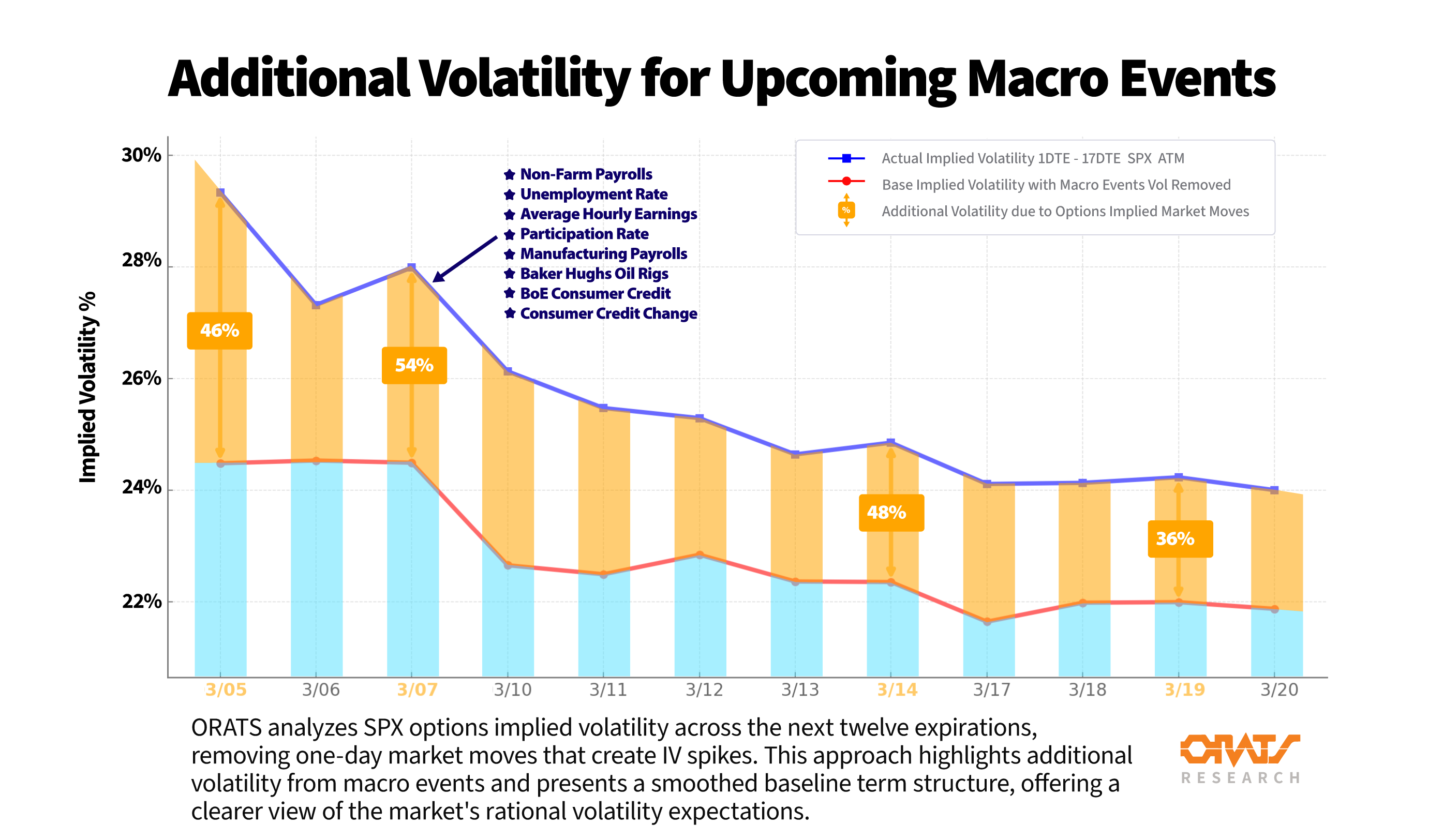

Options traders tracking implied volatility shifts know that macroeconomic releases drive market expectations well before the numbers hit. March 7th stands out as a key event-driven expiration, with SPX options pricing in a 54% implied volatility increase—one of the most significant expected moves in recent weeks. With the current high volatility situation in the market, traders are already pricing in major moves. The bump in the implied volatility term structure for Friday the 7th indicates even more volatility on the horizon.

At ORATS, we analyze SPX options’ implied volatility (IV) across multiple expirations beyond zero-day options, filtering out short-term fluctuations to isolate the true impact of macroeconomic events. Our methodology provides traders with a rational baseline term structure while highlighting additional volatility pricing ahead of key economic releases.

What’s Driving the March 7th Volatility Spike?

SPX options market makers are positioning for significant moves tied to high-impact economic reports. Based on our analysis, the following releases have historically caused notable IV shifts.

ORATS Macro Calendar

ORATS provides a Macro Calendar that tracks upcoming economic events and displays them against historical averages for implied macro move (IMM) and ORATS calculated one day historical volatility (orHv1d). ORATS uses a modified Parkinson historical volatility calculation that allows a one day reading, as opposed to close to close measurements that require more days. This dashboard helps traders correlate macro releases with options market expectations, identifying key dates where volatility spikes are expected.

March 7, 2025: High-Impact Macro Events

Traders should compare these historical volatility averages to the current additional IV of 54% priced in for this expiration.

Why This Matters for Traders

Traders who understand how macroeconomic reports influence implied volatility can identify trading opportunities, hedge risk, and position for potential market moves.

With March 7th shaping up as a high-impact volatility session, traders should be closely monitoring how options pricing evolves leading up to these economic releases.

Want to stay ahead of volatility shifts? ORATS delivers the data you need to trade with precision.

Read more: https://orats.com/blog/significant-volatility-events-for-next-week

Latest articles

This data feed is not available at this time.

Data is currently not available