By Phil Mackintosh, Senior Vice President, Chief Economist, Nasdaq

Economy at a Glance

Figure 1: Key Indicators and Trends

Sources: Nasdaq Economic Research, FactSet

Tariffs Have Become a Reality for Companies to Deal With

Since President Trump won the election, new tariffs on goods imports have been a high probability. Trump campaigned on a flat 10% across the board tariff. By February, extensive new tariffs were proposed for Mexico, Canada, and China.

Tariffs are intended to strengthen U.S. manufacturing and the economy, helping U.S. companies compete, grow, and increase profits. However, stock market returns suggest that investors have different opinions on tariffs. The U.S. stock market has already started to underperform compared to most countries.

Figure 2: Share of U.S. Goods Imports

Sources: Nasdaq Economic Research, FactSet

The economic reasoning behind this reaction is that tariffs add inefficiencies and costs. Moreover, tariffs increase the price of imports, which adds costs to local producers when they need foreign components or machinery. That, in turn, makes them less competitive for exports and reduces local demand for their products.

U.S. companies that import goods have two choices. They can absorb some of the tariffs, which hurts profit margins. Alternatively, companies can increase prices, which impacts incomes for U.S. workers and may slow consumer spending that has kept the economy so strong.

If the rest of the world resists raising tariffs on each other, they avoid these costs. In some instances, like Europe agreeing to reinvest in its own defense industry, the response could boost local economies.

Liberation Day Shocked Companies and Markets

On April 2, “reciprocal” tariffs became a reality. Many countries announced their own tariff rates—often well above the 10% proposed before the election. The rates were clearly structured to reduce the U.S. trade deficit, with countries having larger trade deficits facing larger tariff rates (Figure 3). Many of the U.S.’s largest trading counterparts saw tariffs of 20% or higher. For example, Vietnam, one of the beneficiaries of the 2018 trade war with China, saw a proposed tariff rate of nearly 50%.

Figure 3: April 2 Proposed Tariff Rates

Sources: Financial Times, White House, U.S. Census Bureau, USTR

Markets plunged on fears that some companies might not be able to operate profitably with such high tariffs. Higher costs would also reduce demand in many export-oriented industries, leading to less output and job losses. In turn, it was feared that would stall the consumer spending recovery and push countries into a recession.

Currency markets also started to react. The U.S. dollar began to fall, with logic being that if U.S. imports became more expensive, demand would fall and there would be less U.S. dollar trading. Some feared that might even affect the U.S. dollar’s position as the global reserve currency and the “exorbitant privilege” bestowed on U.S. bonds (via unusually low interest rate costs).

A Pause While Deals Are Struck

Within a week, a 90-day pause on higher reciprocal tariffs was announced, leaving all countries paying the 10% rate on imports. This pause helped buy time to work through trade deals and announce final tariff rates.

The UK was the first country to officially strike a deal, with many other countries working on compromises. Figure 4 suggests that the markets expect the tariff war to de-escalate from here, while also showing potential impacts from prolonged uncertainty and escalation by other countries.

Figure 4: Markets Are Pricing for a De-Escalation of the Tariff War

Sources: Michael Kantrowitz, Piper Sandler

What Companies Should Be Thinking About

One thing we learned from the trade war with China in Trump’s first presidency is that companies can expect events to unfold in four likely—but discrete—steps over time:

- Tariffs are announced and implemented.

- Other countries negotiate compromises or introduce retaliatory tariffs.

- Companies adjust their supply chains to account for new costs, supply, and demand.

- Labor and resource constraints cause own supply chain bottlenecks as companies execute on new supply chains.

For example, in 2018, China retaliated by taxing soybean imports from the U.S. Data suggests that U.S. soybean exports decreased by half and prices fell. Exports still have not recovered. It is likely that farmers now plant different crops that they can sell to other countries.

With a global implementation of tariffs, all companies will need to reconsider supply chains and import costs. This is the whole point of the tariffs. As a result, the U.S. government wants to bring more engineering and factory jobs back to U.S. soil. However, with tariffs on all countries, it may be more cost-effective to relocate some production and build new factories in the U.S.

The 90-day delay for negotiations also extends the uncertainty for many companies.

Sentiment Indicators Are Markedly Different

A wide range of market survey results and sentiment indicators have fluctuated dramatically. They suggest that companies might slow or stop their spending while they await clarity on new trade deals. This is supported by the Future Capex Expectations tracker and the Michigan employment expectations indexes, both of which fell to levels typically seen only during recessions.

Figure 5: Sentiment Has Changed Dramatically

Sources: (1-8) Bloomberg, data as of April 3, 2025; CEO confidence is Chief Executive Magazine; CEO economic outlook is U.S. Business Roundtable

Economic Data Has Not Weakened Yet

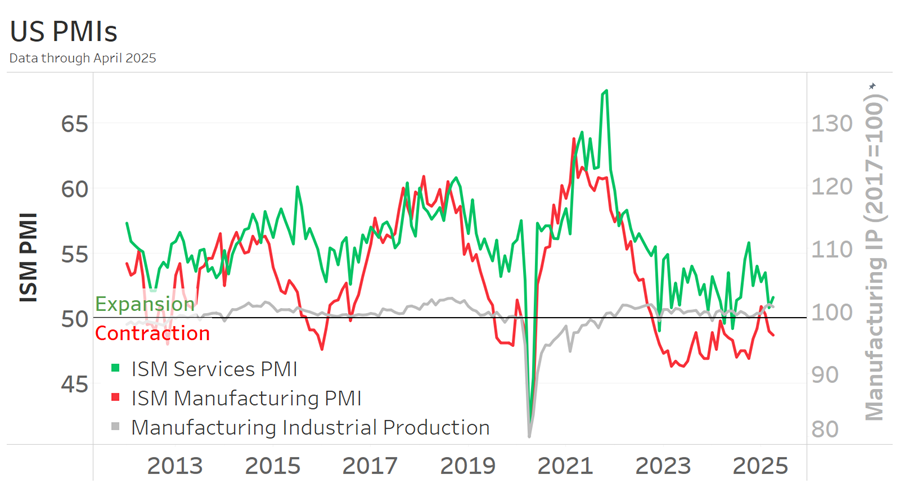

Despite the uncertainty, “hard data” remains robust. Even data from April, the month of highest uncertainty, shows resilience. PMI data suggests that the services sector, which accounts for around 80% of the U.S. economy, is still growing. Even the manufacturing sector, despite reporting weak forward orders and expectations, has seen small but consistent growth in industrial production over the past few years.

Figure 6: Services Sector and Industrial Production Remain in Growth Mode

Sources: Nasdaq Economic Research, FactSet

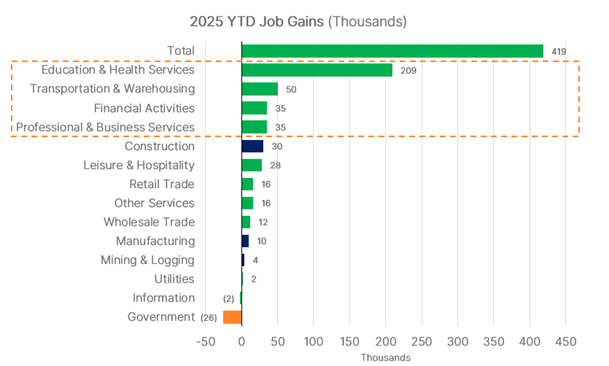

Despite the fall in employment expectations, layoffs remain low and payroll numbers (new jobs) remain robust—essentially unchanged. Even the rash of government layoffs initiated by the Department of Government Efficiency (DOGE) have subsided. In fact, data suggests the healthcare and hospitality industries still have a shortage of hired workers, supported by their continued leadership in new hires based on payroll data.

Figure 7: Job Losses Remain Low; Healthcare, Education, and Supply Chain Are Hiring Aggressively

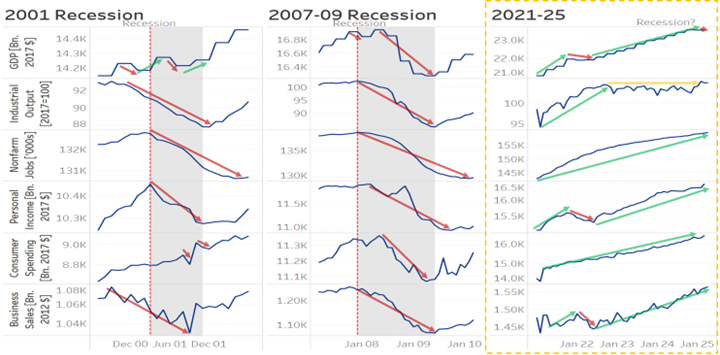

Although many economic models suggest adjusting to tariffs increases the chance of a recession, it is the National Bureau of Economic Research (NBER) that determines when a recession has occurred using six different data points (Figure 8). Importantly, none of these indicators are falling, unlike during the past two major slowdowns when almost all economic factors were weak.

Figure 8: Most Hard Data Are Positive

Sources: FactSet, NBER

Tariffs Create Winners and Losers: Being Dynamic Will Be Important

The significant changes observed so far in Trump’s second presidency have considerably altered the trade and geopolitical landscape. However, not all countries (or companies) will be losers. Some economists are discussing scenarios where countries that are forced to invest in securing their own supply chains may improve their economic performance and employment. That is the hope of the U.S. government, too.

MUFG created a useful matrix highlighting industries and companies more or less exposed to the trade war (Figure 9). To date, relative movements in stock returns support this early thinking, with consumer staples, industrials, and utilities sectors outperforming consumer discretionary and energy sectors.

Figure 9: Tariffs Will Create Challenges and Opportunities

Source: MUFG

As observed after the 2018 trade war against China, some industries saw gains, and companies that were able to move supply chains often benefited. The new trade war, affecting all countries, makes 2025 more complicated to navigate. However, for companies and workers willing to adapt, it may also offer opportunities.

5 Questions Board Members Should Ask Today

- What does our supply chain look like now?

- Have we investigated alternative suppliers in different countries?

- Is someone keeping track of all the rules and details of the new trade deals?

- Have we identified international opportunities?

- How does our supply chain compare to our competitors?

To receive an exclusive video with further insights from Nasdaq’s Chief Economist and Senior Director of Economic Research, join the Nasdaq Center for Board Excellence. For the latest market insights, explore the Nasdaq Center for Board Excellence Resource Library and subscribe to Market Makers.

The views and opinions expressed herein are the views and opinions of the authors and do not necessarily reflect those of Nasdaq, Inc.

Latest articles

This data feed is not available at this time.

Data is currently not available