Digital payments continue to scale globally as commerce shifts toward online and mobile channels, while value-added services, tokenization and data-driven capabilities reshape how transactions are processed and monetized. Within this evolving landscape, Mastercard Incorporated MA and PayPal Holdings, Inc. PYPL offer distinct models for capturing this growth, making them relevant comparables amid ongoing shifts in competitive dynamics and revenue mix.

Mastercard operates a network-centric model with high-margin revenue streams tied to transaction volumes and cross-border activity, whereas PayPal follows a platform-driven approach built on branded checkout, digital wallets and merchant services. These differences reflect contrasting strategies around scale, engagement and monetization as the payments ecosystem continues to evolve.

Let’s dive deep and closely compare the fundamentals of the two stocks to determine which one has more room to run.

The Case for Mastercard

Mastercard’s core strength remains its global payments network, which continues to deliver steady volume growth across geographies and spending categories. Cross-border volumes, a key profitability driver, up 15% year over year in 2025, remained robust, supported by travel recovery and rising international commerce. The scale of its network not only supports transaction growth but also enhances acceptance and data generation, reinforcing its competitive positioning. Its global GDV rose 9% year over year in 2025.

Beyond core payments, Mastercard is increasingly monetizing its ecosystem through value-added services such as cybersecurity, fraud prevention, analytics and consulting. These offerings are growing faster than the underlying network and are often tied to transaction activity, creating a layered revenue model. Around 40.6% of the company’s net revenues in 2025 came from the value-added services and solutions segment. This shift supports margin expansion while reducing reliance on pure payment processing fees.

MA is also broadening its exposure to new payment flows, including commercial payments, B2B transactions and cross-border money movement. Solutions like Mastercard Move and virtual cards are helping capture opportunities beyond traditional consumer card spending. This diversification expands its addressable market and provides additional levers for long-term growth. The company beat earnings estimates in each of the past four quarters, with an average surprise of 5.5%.

Mastercard Incorporated Price, Consensus and EPS Surprise

Mastercard Incorporated price-consensus-eps-surprise-chart | Mastercard Incorporated Quote

Additionally, it continues to invest in innovation to stay relevant in a rapidly evolving payments landscape. Tokenization, AI-driven insights and early-stage initiatives in areas like agentic commerce and digital assets are aimed at strengthening its role as a foundational infrastructure provider. These efforts position the company to adapt as new payment technologies and use cases emerge.

MA’s strong cash position enables substantial share buybacks and dividend payouts and supports inorganic growth and financial stability. With $10.6 billion in cash, the company maintains a solid capital position. Its return on invested capital of 41.93X is higher than the industry’s average of 23.29X and PYPL’s 14.53X. It repurchased $11.7 billion in stocks and paid $2.8 billion in dividends in 2025.

However, the upside was partly offset by escalating operating expenses and higher rebates and incentives. In 2025, rebates and incentives (a contra revenue item) rose 16.4% year over year; we expect them to rise 15.3% in 2026. The company anticipates adjusted operating expenses to witness low double-digit growth year over year in 2026.

The Case for PayPal

PayPal continues to see strong momentum in Venmo, which is evolving into a more monetized commerce platform rather than just a peer-to-peer payments app. In 2025, Venmo revenues grew around 20% year over year to $1.7 billion, while total active accounts surpassed 100 million, reflecting rising engagement. Growth in debit card usage and “Pay with Venmo” is driving higher everyday spend, with the latter seeing 32% TPV growth, reinforcing its increasing role in commerce.

Also, the company is strengthening its merchant-facing infrastructure through its PSP business. Enterprise Payments has delivered seven consecutive quarters of profitable growth, with double-digit volume growth in the fourth quarter of 2025. Margin expansion is being driven by better pricing discipline and increasing adoption of value-added services, with 16 offerings now contributing to improved processing yields and merchant stickiness. It is also expanding its monetization levers through Buy Now, Pay Later and broader platform capabilities. BNPL processed over $40 billion in TPV, which increased 20% year over year in 2025 and is increasingly integrated into checkout and merchant offerings. It beat earnings estimates in three of the past four quarters with an average surprise of 7.8%.

PayPal Holdings, Inc. Price, Consensus and EPS Surprise

PayPal Holdings, Inc. price-consensus-eps-surprise-chart | PayPal Holdings, Inc. Quote

Additionally, PayPal is investing in omnichannel capabilities, including in-store payments via partners like Verifone, targeting the large offline payments opportunity. At the same time, newer initiatives such as agentic commerce integrations and wallet interoperability aim to position the company within next-generation shopping experiences, even though these are unlikely to materially impact near-term growth.

PYPL’s near-term focus is on revitalizing its branded checkout business, which has faced slower growth due to execution challenges and competitive pressures. Online branded checkout TPV grew just 1% in the fourth quarter (currency-neutral), reflecting a sharp deceleration, with pressure concentrated in U.S. retail spending and international markets such as Germany, alongside softer trends in key verticals like travel, ticketing, crypto and gaming. The company is reworking its approach around improving user experience, strengthening merchant integration and increasing visibility at checkout, but scaling these changes and restoring momentum remains a work in progress.

PayPal continues to forge strategic partnerships to expand its offerings and global presence. The company exited the fourth quarter of 2025 with cash and cash equivalents of $8 billion. It returned $6 billion to its shareholders by repurchasing shares of common stock in 2025.

How Do the Estimates Compare for MA & PYPL?

The Zacks Consensus Estimate favors MA at this stage. The consensus estimate for MA’s 2026 earnings indicates a 14.8% increase from a year ago. Meanwhile, the consensus estimate for revenues suggests 12.7% growth. On the other hand, the consensus estimate for PYPL’s 2026 earnings indicates 0.2% growth from a year ago, while the same for revenues suggests a 3% rise.

Valuation: MA vs. PYPL

Coming to the valuation story, it seems that investors are willing to pay a premium for Mastercard compared to PayPal. This is reflected in MA’s forward 12-month price/earnings (P/E) of 25.53X compared with PYPL’s 9.30X. Both are currently trading below their five-year median P/E value.

Image Source: Zacks Investment Research

Price Target

Mastercard currently trades below its average analyst price target of $652.66, implying a 25.9% potential upside from current levels. Meanwhile, PayPal currently trades below its average analyst price target of $50.67, implying a 1.7% potential upside from current levels.

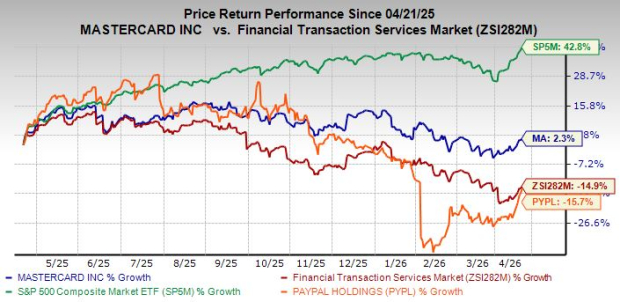

Price Performance Comparison

Over the past year, shares of Mastercard have outperformed PayPal and the industry. Meanwhile, the S&P 500 has increased 42.8% during this time.

Price Performance – MA, PYPL, Industry & S&P 500

Image Source: Zacks Investment Research

Conclusion

Overall, MA appears better positioned at this stage, supported by its resilient network-driven model, consistent cross-border strength and faster-growing high-margin value-added services. Its diversified revenue streams, strong cash generation and disciplined capital allocation provide greater visibility into sustained earnings growth.

In contrast, PYPL is still navigating execution challenges in its core checkout business despite progress across Venmo, PSP and BNPL. While PayPal’s platform transformation offers long-term potential, Mastercard’s current fundamentals, growth trajectory and profitability profile suggest it has comparatively more room to run in the near to medium term.

Currently, MA carries a Zacks Rank #2 (Buy), while PYPL has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Mastercard Incorporated (MA) : Free Stock Analysis Report

PayPal Holdings, Inc. (PYPL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.