By Benjamin Truitt

I have always looked at accumulation and movement of capital as indicators of things to come. I have seen several articles discussing the recent flat lining or decline in M2 and it being of concern. Let’s look a little bit at M1 and M2, what they mean, and how we should view the recent M2 trend.

M1 is an estimate of money circulating within the economy, plus checking account deposits and more recently savings accounts. M2 includes M1 plus money in money market accounts and mutual funds. M2 is often viewed as an indicator of future inflation and economic growth potential.

Let’s put on some blinders and look at the declining M2 trend in the below “The Sky is Falling” chart:

From this very narrow view of historical M2 growth and how it typically trends, some could draw the conclusion that the economy is in for some pain ahead and it’s likely inflation may start to decline. Some good, some bad.

Now, let’s take the blinders off and see how the longer M2 trend compares to the recent M2 movements.

This appears to be even more concerning. M2 is 6% below the trend since the start of 2021 but is 32% above the trend since 2005.

From Investopedia): “M2 is closely watched as an indicator of money supply and future inflation, and as a target of central bank monetary policy.”

M2 being 32% above the trend must be what the Fed is so concerned about, and why they are so quickly increasing rates. It sounds scary. Let’s take a deeper look.

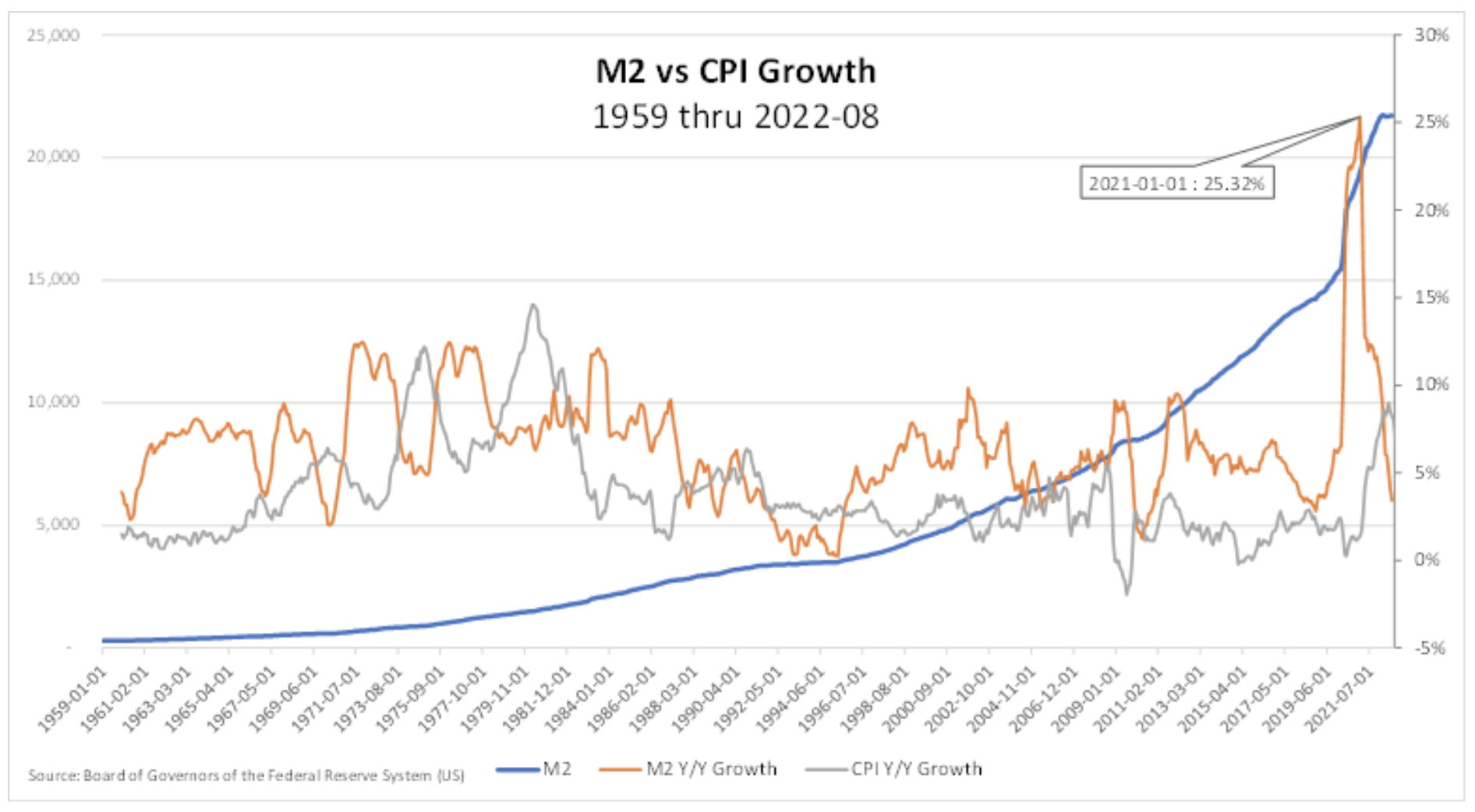

Below is an M2 chart, since 1959 alongside its monthly year-over-year (Y/Y) growth and monthly CPI inflation Y/Y.

The Y/Y lines seem to show some correlation, but it’s very difficult to say if M2 growth is indeed an indicator of future CPI inflation. A correlation analysis yields a correlation coefficient of 0.077. A coefficient of 1.0 is perfectly correlated. 0.077 represents pretty much zero correlation. Okay, this isn’t really fair because the Fed uses M2 as an indication of “future” inflation, so there should be a lag and, if true, the recent 25% spike in M2 should be very concerning. If you apply a lag to the correlation calculation, the peak correlation coefficient of 0.49 comes with a 31 one-month lag between M2 Y/Y growth and CPI Y/Y inflation. With a correlation coefficient of 1.0 being perfectly correlated, I’m not that concerned about 0.49. Even if this was a reliable indicator of future inflation, the spike in inflation should come 2.5 years after the January 2021 spike in M2, which is not now.

In my opinion the Fed has done their job in reining in inflation. I also think the cause of inflation was much more related to the constrained labor and product supply given some extraordinary circumstances that includes a pandemic versus M2 growth. I do believe M2 can be a more reliable indicator of future economic activity. I feel the growth in M2 has just started and it is likely capital markets will greatly expand from further increases in M2. As an example, the correlation coefficient between M2 and the S&P 500 is 0.93 showing near perfect correlation.

Yes, M2 has recently declined, but is still 32% above the trend. I view this increase in M2 as rocket fuel thrown into an already strong economy by many measures. The Fed’s recent rate increases and management of future expectations has significantly impacted many areas of CPI inflation, most notably housing. If just the decline in housing begins to show in CPI readings, CPI inflation will begin to decline and if this leads to the Fed taking their foot off the brakes, this rocket fuel should be put to action. During the 10-year period following the peak of inflation in 1980 the S&P 500 was up 221% and that was without such significant growth in M2. We could be in for an amazing bull market across many asset classes for the decade(s) to come.

Benjamin Truitt, a data scientist, is the founder and CEO of Spire Fund Advisory, LLC and investment manager for BYTZ Fund, LP., an algorithmic-based equity hedge fund which utilizes the applications of machine learning artificial intelligence. An avid researcher, Benjamin is always seeking to better understand the markets and movements by tracking data patterns. To learn more, please visit his LinkedIn profile.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.