Credit: Shutterstock photo

Credit: Shutterstock photoBy Kerrisdale Capital Management :

We are long shares of Luxoft ( LXFT ), as we believe the company is poised to double revenue over the next five years, and then do so again over the subsequent five. Luxoft stock has declined in 2016, as investors have become concerned with slowing growth. The recent move by the U.K. to leave the European Union exacerbated the weakness as the European banks (including Deutsche Bank ( DB ), Luxoft's largest customer) are being pushed to multi-year lows. However, Luxoft remains a premium vendor whose services are mission-critical for clients. The recent renewal of a five-year Master Services Agreement (( MSA )) with Deutsche Bank illustrates customers' reliance on Luxoft despite a challenging market environment.

With a revenue base of over $680 million, Luxoft resembles Cognizant ( CTSH ) 10 years ago, highlighted by a comparable growth trajectory. Cognizant's revenue exhibited a remarkable 37% CAGR over a 15-year period, developing from a modest $89 million in 1999 to a $10 billion offshore powerhouse. We think LXFT can grow at a similarly high rate over the next 10 years. Our view is underpinned by management's recent guidance of 20% compounded revenue growth, $1.5 billion in revenue by FY 2020, and a resulting market capitalization of $3 billion within five years. In fact, we think that forecast is conservative. A more likely scenario: LXFT multiplies its revenue base by 4-5x supported by its position as a best-in-class provider of high-end software developers serving a massive total addressable market. Our DCF analysis suggests shares are worth ~$108 today (105% upside) and likely more in time.

Luxoft's differentiated focus on high-end software development is executed via engagement of leading programming talent in the science-centric Central and Eastern European (( CEE )) region. Unlike the large Indian vendors deriving value primarily from labor arbitrage, LXFT's value proposition is predicated on an exceptionally skilled employee base to deliver sophisticated domain expertise. The company employs nearly 9,000 offshore programmers in the CEE geography, a region deeply rooted in science and technology; these emerging economies produce nearly one million engineering graduates annually. It has already achieved success with this strategy, growing revenue at a 27% CAGR over the last five years, while building out proficiency in sectors such as financial services and automotive. Furthermore, Luxoft commands a premium bill rate and generates the highest revenue per employee within the offshore industry. In an industry that competes aggressively for talent, LXFT boasts the lowest attrition rate amongst its peers.

The offshore IT services industry is well positioned to grow, fueled by a significant enduring cost differential between U.S. and non-U.S. IT employees. The current climate of hyper-paced digital advancements within every industry, coupled with a shortage of talent in the U.S. will result in continued outsourcing of labor to countries with a cheaper and more abundant workforce. While the total offshore IT industry is expected to grow at 9% through 2019, the application outsourcing sub-segment in which Luxoft operates is projected to grow at 14%. The company's ~9,000 IT employees represent a mere fraction of the hundreds of thousands employed by the Indian vendors, and its LTM revenue of $681 million is a tiny portion of a thriving $60 billion industry. If LXFT and its CEE peers attain a quarter of the success realized by their Indian counterparts in the late '90s and early 2000s, LXFT will not remain only a $1.7 billion, or even $10 billion, company for much longer.

I. Situation Overview

Weakness in Luxoft shares began in early 2016 due to concerns of slowing growth and the perceived risk of losing Deutsche Bank, the company's largest customer. The sell-off of Luxoft was exacerbated by Brexit and the overall weakness of the banking sector, leading to all-time lows for DB shares. The market now completely ignores fundamentals and Luxoft's significant growth opportunity, evident by the recent direct correlation of LXFT shares with DB. We believe these concerns are overblown. Even in the most turbulent times (the financial crisis of 2008-2009 and the European debt crisis of 2012), the company managed to grow within its largest clients. We believe over the long term, current concerns around Luxoft's relationship with DB will prove to be short-lived as the business continues to execute, grow and diversify.

Luxoft's projects for Deutsche Bank are mission-critical

Luxoft focuses on Deutsche Bank's front-office rather than back-office functions, with its projects supporting entire processes that are critical for operations. Furthermore, as a result of increased regulations, the majority of its services help to keep Deutsche Bank in compliance with regulatory bodies in both the EU and the U.S. An example of a project that Luxoft assists with Deutsche Bank is Arena. Arena was a platform that was co-developed by Luxoft about 10 years ago and is a critical trading platform used for equities (acts as an order management system for DB's equity traders). This has been an ongoing project for years and is just one of many that Luxoft's ~2,600 engineers at DB help to manage (more examples of specific projects are available later in this report).

We find it unlikely that the company faces any imminent risk of completely losing this account given the renewal of the DB MSA earlier this year which runs through 2020. DB, which has utilized Luxoft since 2003, plans to reduce costs significantly through " Strategy 2020 ," but based on our conversations with management, we don't expect those cuts to impact LXFT.

Deutsche Bank historically consolidated smaller IT vendors and shifted more work to Luxoft

In previous financial crises (the financial crisis of 2008-2009 and the European debt crisis of 2012), Deutsche Bank consolidated many of its smaller IT vendors and shifted more work to Luxoft. In 2012, the bank undertook a major vendor consolidation and reduced the number of large IT vendors from 12 to 4. Luxoft benefited from that consolidation and attained Key Strategic Vendor status, which led to an expanded footprint within the investment bank. While Luxoft is certainly larger today at DB than it was in 2012, we believe that given Luxoft's critical role within DB's core operations, any potential consolidation will likely occur with smaller, less-strategic vendors.

Today, non-strategic vendors account for about ~40% of Deutsche Bank's IT offshore budget (equivalent to ~$800 million of total ~$2 billion). We think any further consolidation would result in re-allocating more of the budget to strategic vendors. Luxoft's CEO believes that going forward the share of strategic vendors could grow from 60% to 80%, positioning the company favorably as a top strategic vendor.

Luxoft has minimal exposure to the British pound

Despite the significant European exposure, Luxoft will not be impacted by the recent devaluation of the British pound. In the latest fiscal year, revenues from the pound accounted for 7% of total revenue, while expenses accounted for 12%. With a greater exposure to the pound in expenses, we actually expect the company's margins to improve y-o-y as a result of the currency's devaluation. As evident by the chart below, Luxoft is paid by clients primarily on a USD and euro basis.

Revenue and Expenses breakdown by Currency (FY 2016)

Source:LXFT FQ4'16 earnings presentation

Strong growth outside of Top 5 accounts

With Luxoft still in its nascency, customer concentration isn't an immediate concern for us at a current revenue base of $681 million, because we believe the company will be many times larger in the future, and it's rapidly expanding beyond its top five customers. Luxoft reported 56% revenue growth in the FY 2016 from accounts outside the top 5; we are confident that customer concentration will not present an issue in the not-too-distant future.

Revenue Growth Excluding Top 5 Customers

Source: Company filings

Our revenue projections call for 15% top line CAGR over the next 10 years. We believe Luxoft's 20%+ growth over the next 1-3 years will be supported by proliferation in accounts outside the top 5. For DB, we assume little to no growth over our projection period. Management has made it clear that its base case is for DB to stabilize around $200 million over the next few years. For UBS Group (UBS), we have revenue reaching around $200 million, per management guidance. We do not assume significant growth for Harman (HAR) beyond the $50-60 million threshold, and expect Credit Suisse (CS) to be on a similar trajectory as UBS. Outside of these large clients, we arrived at 30-35% growth, a hurdle which we think Luxoft will easily surpass given recent performance as well as the growing portfolio of high-potential accounts ("HPAs").

Revenue Projections

Source: Company filings and Kerrisdale analysis

The number of high-potential accounts increased from 12 at the IPO in 2013 to more than 40 at present. Clients are classified as HPAs if management believes the accounts have the potential to reach at least $5 million in recurring annual revenue within the short to mid-term. During the 9-month period ending 12/31/15, revenue from this account base grew at 177% y-o-y and comprised at least 25% of revenues in FY2016.

Overall, we foresee the slowdown of the top accounts being offset by a large and diverse customer base experiencing strong growth. While much attention is focused on Luxoft's work in the financial services sector, there's likely additional upside from the developing automotive segment (more detail on this sector later in the report), which continues to grow at 40%+. Luxoft CEO Dmitry Loschinin said automotive remains a high priority, and the firm's investments appear to be paying off, as an automotive OEM account added last year is already a top 10 account. The company has demonstrated a willingness to allocate capital for M&A, and with its unlevered balance sheet, future tuck-in acquisitions provide yet another avenue of growth in excess of our base scenario.

Excess demand at other clients

Through our diligence with management, former executives and current customers, we discovered that demand far outpaces supply, and Luxoft struggles to hire enough talented engineers as fast as it would like. Historically, the company had excess demand to allocate an additional ~1,000 engineers for current customers. We think even in the unlikeliest scenario that projects get scaled down significantly at Deutsche Bank, Luxoft's revenue base would be protected by its ability to reallocate personnel to other customers.

The company publishes very detailed job postings on its careers website , and we believe the number of job postings is a good proxy to measure excess demand. Throughout 2016, the number of job postings stayed in the ~620 area, implying that demand remains very strong.

Historical Job Postings

Source:Luxoft's Russian language careers website, online web archive service the Wayback Machine and Luxoft's English language career website

Concluding thoughts on current Deutsche Bank situation

Despite the challenges Deutsche Bank faces in an uncertain economic environment, Luxoft has proved resilient in similar macro environments, and we believe Luxoft will ultimately grow out of this perceived issue as management continues to expand within other customers. Given the 20%+ growth and long-term potential to compound, we think the company is too cheap at 18x earnings. Its projects are long-term in nature, with average engagements of at least 3-5 years; moreover, Luxoft is entrenched with DB until at least 2020, and growth from accounts outside the top 5 is resilient. We anticipate that the recent sell-off of in the stock price will prove temporary, and expect to see a significant return on our investment, as Luxoft shares are currently trading at bargain prices.

II. Investment Highlights

- Unique Central and Eastern European-based IT outsourcing firm focused exclusively on high-end software services. Luxoft has over 9,000 offshore computer programmers and serves clients primarily in North America and Western Europe. Relative to its peers in India, the company does not compete on price, but on providing teams of programmers who understand clients' businesses and industries intimately and are capable of providing advanced, customized application development and other IT solutions. Rather than compete with Indian offshore providers that leverage labor arbitrage to undercut rivals, Luxoft focuses on high-end software services and hiring skilled engineers. Indian vendors oftentimes fill their ranks with novice developers, heavily recruiting recent college graduates; in contrast, 80% of Luxoft's employees have a master's degree and at least five years of professional experience. This approach has enabled its developers to command a premium bill rate relative to the prevailing industry standard, as well as cultivate a reputation for unrivalled quality of work.

LXFT Commands High Bill Rate

- Significant growth opportunity supported by Luxoft's focus on application services. While global offshore IT services are expected to grow 9% annually through 2019, Luxoft operates in the application outsourcing sub-segment which is projected to grow 14% annually over the same period. Growth of the offshore IT industry will be supported by the cost differential between U.S. and non-U.S. IT employees. Furthermore, as U.S. companies scramble to fill gaps in areas such as mobility, Big Data, analytics and automation, the dearth of engineering talent should only become more pronounced over the next decade.

Application Outsourcing Projected to Outgrow Overall IT Spending

Source: IDC worldwide offshore IT services forecast

- Total firm headcount of 11,000 highlights LXFT's relatively small position in the industry and potential growth opportunity. HCL Technologies (HCL), which is only the sixth largest Indian offshore player, boasts an employee base that is still 10x that of Luxoft. With $680 million in revenue, LXFT accounts for barely a sliver of a mammoth $60 billion industry. If it can multiply its headcount by ten and deploy those new programmers at similar margins, the company's valuation could also easily multiply by a factor of ten. Given the abundance of high-quality engineers available in the CEE region, Luxoft's ability to source new talent shouldn't be a formidable challenge. In the science-centric CEE geography, nearly 1 million students graduate annually with a degree in engineering. The company has a high concentration of employees in Russia and Ukraine, which together account for nearly 600k engineering graduates

Headcount vs. Indian Players

Source: Company filings and press releases

Countries with Most Engineering Graduates

Source: World Economic Forum 2015 / UNESCO Institute for Statistics

Note: Excludes China and India.

- Extremely compelling valuation vis-à-vis growth opportunity. For an emerging IT services player with a unique niche in the growing offshore IT services industry supported by a favorable demographic (i.e., a high concentration of smart engineers in CEE), we think the current share price undervalues LXFT's opportunity to multiply its revenue base by at least 4-5x over the next 10 years. We project that if LXFT's IT employee base grows at only an 11% CAGR (identical to the overall offshore application outsourcing industry), the company's revenue base would be 4x larger in 10 years. Our DCF suggests an intrinsic value of ~$108/share, implying 105% upside.

Discounted Cash Flow Analysis

Source: Company filings and Kerrisdale analysis

- Attrition rate of 10.3% lowest in the industry. In the IT outsourcing industry, talent is amongst a company's most valuable assets. As such, we consider employee attrition a key metric when analyzing the sector. Luxoft's employee attrition is one of the lowest in the field, due partly to its mature and highly experienced workforce in addition to its comparatively high pay for the region.

Attrition Relative to Industry

Source: Company filings and press releases

- Success with Deutsche Bank and UBS Demonstrates High Customer Value Proposition. Luxoft's enormous success with marquee clients such as Deutsche Bank and UBS (its largest clients) is representative of the company's ability to exponentially scale each new account. As a result of these long-term relationships (DB has been a customer since 2003, UBS since 2008) and focus on front-office assignments (revenues mostly generated in investment banking and wealth management), Luxoft has developed in-depth subject matter expertise in the financial services industry. Revenue from both clients nearly doubled in the two-year period between FY'13 and FY'15.

Revenue from DB and UBS

Source: Company filings

III. Significant Growth Opportunity Translates to Compelling Valuation

Since FY 2011, Luxoft posted an impressive 27% revenue CAGR, and we believe the business will continue to compound 15-20% on the top line over the next 10 years. Given projected growth for the application outsourcing sub-segment (14% through 2019), as well as Luxoft's relatively small scale (~9,500 engineers), we're very bullish that the company can exceed overall market growth by a significant margin over the next decade.

Application Outsourcing Projected to Outgrow Overall IT Spending

Source: IDC worldwide offshore IT services forecast

Luxoft's staff of 11,000 is miniscule relative to the size of the Indian offshore players. Despite being the sixth largest Indian offshore vendor, HCL still boasts an employee count 10x greater than LXFT's. Even if Luxoft's headcount increased at a 20% CAGR over the next 10 years to ~57k, it would still represent an immaterial fraction of the offshore industry. While we're not arguing that the company's employee base will approach the scale of its Indian competitors anytime soon, the growth opportunity remains quite compelling. Luxoft's total addressable market - namely, the demand for organized teams of sophisticated programmers - is massive.

Headcount vs. Indian Players

Source: Company filings and press releases

Offshore IT services growth will be supported by the material cost differential between U.S. and non-U.S. IT employees. Based on Susquehanna research, U.S. IT personnel are expected to command a 66% and 25% premium to Indian and Eastern European employees, respectively. We believe this cost delta will continue to drive demand for outsourcing work to these geographies. Luxoft employees not only cost less, but have proven domain expertise, particularly in the financial services and automobile sectors.

Hourly Rates: U.S. vs. India and Eastern Europe

Source: Susquehanna research

Furthermore, the shortage of engineering talent in the U.S. will be exacerbated over the next decade. According to the 2012 Report to the President , there is a significant gap between the supply and demand of science, technology, engineering and mathematics ((STEM)) graduates in the United States.

The legacy of the Soviet educational complex focused on mathematics and engineering is evident throughout the CEE region. According to the UNESCO Institute for Statistics, Russia and Ukraine churn out nearly 600k engineering graduates annually (LXFT's engineers are predominantly concentrated in these countries). While the U.S. ranks second in number of engineering graduates, the statistic is marginal relative to density per population. Ukraine currently produces ~130k annual engineering graduates, nearly half of the total U.S. number. Yet, the population of Ukraine is only 44 million, compared with 319 million in the U.S. With Luxoft strategically focused on this STEM-centric geography, we believe future growth will be supported by access to this talent-rich resource pool.

Countries with Most Engineering Graduates

Source: World Economic Forum 2015 / UNESCO Institute for Statistics

Note: Excludes China and India.

Conservative Revenue Analysis Suggests Compelling Growth Opportunity

For our revenue forecasts, we project that Luxoft's employee base tracks the overall offshore application outsourcing market (about 14% CAGR over projection period). Based on the recent 18-20% growth of the employee base, we modeled 15% for FY 2017, eventually receding to ~10% per year beginning in FY 2022. In terms of revenue per employee, we project a 3% increase in productivity over the projection period, about 100bps lower than the 4% CAGR between FY 2011 and 2015. Management's goal is to reach $100k/employee, and we have modeled in a scenario where that is nearly achieved by year 10. Aggregating these estimates results in a revenue CAGR of ~15% and a business that is 4x larger by 2026 - and that's just if we model employee growth at an 11% CAGR. The forecasts appear even more attractive as growth rates approach those achieved by the Indian offshore industry between 2000 and 2010. For reference, CTSH grew sales from $137 million in 2000 to $4.6 billion in 2010, and Infosys (INFY) sales increased from $414 million in FY'01 to $4.8 billion in FY'10.

Illustrative Revenue Analysis

Source: Company filings and Kerrisdale analysis

Valuation Too Compelling Considering Growth Opportunity

We think Luxoft is too cheap at its current valuation of 18x FY17E P/E given its long-term growth potential. It is a well-managed operator with a sticky customer base, a differentiated product and a massive and rapidly growing total addressable market. We think the current share price undervalues LXFT's potential to multiply its revenue base by at least 4-5x over the next 10 years.

Current Valuation

Source: Company filings and CapitalIQ

The evolution of the Indian IT industry provides a cautionary study of how investors fixated on current free cash flow yields can miss out on a long-term growth story. While "value investors" may balk at Luxoft's seemingly high valuation, we would argue that a P/E multiple of 18x is a significant discount to where Indian vendors such as CTSH have traded since 2000. At the height of the tech bubble, CTSH traded as high as ~73x P/E (1-year forward basis), and between 2001 and 2007, it averaged 37x P/E. Investors who avoided the stock on account of its optically high 30x+ valuation multiples missed out on a tremendous opportunity: a CTSH investor who bought shares in 2000 and held to today would have earned 30x his investment, representing a 23% IRR over a 16-year period.

Cognizant: Historical Multiples and Stock Price Performance

Source: CapitalIQ

Despite valuation multiples consistently above 30x between 2000 and 2007, investors earned outstanding returns because the Indian IT companies succeeded in compounding at very high growth rates. CTSH, INFY and Wipro (WIT) achieved 36%, 31% and 20% CAGRs, respectively, over a 15-year period.

Historical Revenue: Cognizant, Infosys and Wipro

Source: Company filings and press releases

Note: Fiscal year ends March 31 for Infosys and Wipro.

Note: FY '13 not comparable for Wipro due to business divestiture.

Luxoft and EPAM Systems Inc. (EPAM), the preeminent CEE players, exhibit similar revenue trajectories.

Revenue Trajectory of CEE IT Services Players

Source: Company filings

To value Luxoft, we use a discounted cash flow analysis. A DCF properly captures the long-term opportunity as compared to a 1- or 2-year forward valuation multiple metric. Our conservative analysis suggests an intrinsic share value of ~$108, implying 105% upside.

The revenue build-up is identical to our previously discussed revenue analysis. We project top line growth of 15% CAGR, with EBIT margins expanding by approximately 370 basis points over the projection period. Similar to other IT services businesses, Luxoft's operating margins should have room to increase as the business scales. Historically, CTSH reinvested incremental earnings above a 19-20% EBIT margin threshold, so we believe a 350 basis point expansion to ~19% for LXFT by 2026 is reasonable. Our other assumptions include:

- A 10% discount rate. Normally we would model using a lower cost of capital, but given political instability in key geographies like Ukraine, we applied a slightly higher premium. Note that since Luxoft's sales are primarily to Western companies, investors should not look to Ukrainian or Russian interest rates, but instead, should look at eurozone and American rates as a point of reference.

- Purchase of intangibles at 1% of revenue. Under IFRS, LXFT capitalizes a portion of its software development costs. Purchase of intangibles as a percentage of revenue has historically approximated 0.3-1.5% of sales.

- Capex at 3.5% of revenue. As a people-oriented services business, LXFT is not capital-intensive.

- Terminal FCF multiple of 17.5x.

Discounted Cash Flow Analysis

Source: Company filings and Kerrisdale analysis

IV. High-Quality and Differentiated Business Model

Luxoft has succeeded in establishing a unique edge in offshore IT services, an industry where many key players have failed to differentiate themselves. Given the small scale of Eastern European companies relative to the Indian heavyweights, investors often overlook the differences between some of the small Eastern European players and the Indian providers, assuming the services of Luxoft and its larger peer EPAM are comparable to those of Indian vendors Infosys, Cognizant, Wipro, etc.

However, Luxoft is focused exclusively on application services and advanced, customized IT solutions. Specifically, the company's forte is application development, as opposed to more mechanical application maintenance and testing. Clients turn to Luxoft for complicated tasks, customized solutions and adept programmers who take ownership of deliverables, not simply an army of bodies. The more rudimentary offerings of the Indian providers present a poor substitute.

Focus on High-End Application Development

The IT services industry can be segmented into three areas: business process outsourcing ((BPO)), infrastructure services and application services. Indian providers such as Cognizant, Infosys, HCL Technologies and Wipro provide services across the entire spectrum; Luxoft focuses exclusively on the application services sub-segment.

Overview of Offshore IT Services

Source: Company filings and press releases

Buzzwords applied in the IT industry can be confusing, often obscuring what some of the services actually encompass. While we've divided the IT outsourcing industry into three distinct sub-segments for illustrative purposes, the different functions are separated by more of a "dotted grey line," as projects could entail both labor-intensive BPO work and bespoke application development. For instance, Cognizant might be hired to build software from scratch, and a different vendor might be engaged to help with the maintenance. With that said, the differences between BPO, infrastructure outsourcing and application services could be simply defined as follows:

- Infrastructure services: A 3rd-party IT vendor (like HCL or Wipro) monitors and manages the hardware and software of the client's underlying technology assets and users (i.e., data centers, end-user management, security, help desk).

- Business process outsourcing: A 3rd-party IT vendor manages a specific business activity (i.e., payroll, HR, accounts receivable, etc.).

- Application services: A 3rd-party IT vendor provides customized software solution tailored to a specific business purpose.

The chart below outlines the various sub-segments and provides some high-level examples. We will follow with specific examples.

Snapshot of Various Types of IT Outsourcing

Source: UBS initiating report on Accenture (04/03/2013)

Infrastructure Outsourcing

Infrastructure outsourcing consists of services related to helping an enterprise manage its IT assets (i.e., data centers, network hardware, security services) and end-user support. Services may include management of help desks (i.e., assist end-users with basic IT issues), end-user devices, data centers, network services and IT spend. Specific examples of infrastructure outsourcing services include the following:

- Large global bank hires IT outsourcer to help integrate different IT systems of numerous acquired entities.

- Current IT infrastructure includes multiple voice, data and IT networks with limited integration.

- Each brand and office ran on a separate network, serving 100,000 end users and more than 10,000 call center agents.

- Aging equipment and separate carrier contracts exacerbate issues in integrating under one consolidated network.

- IT vendor forms an agile cloud-based network to support all voice and data needs on global scale and replaces all old and legacy systems.

- Large global corporation hires IT outsourcer to help manage the demand for 24/7 technical support due to a significant increase in the number of applications and device usage.

- IT outsourcer takes over the entire service desk and provides a single point of contact for all technology incidents and requests.

- Provides support to over 100,000 end users.

- Outsourcing this function allows corporate to minimize the cost of downtime.

Business Process Outsourcing

Exponential growth in the offshore outsourcing industry in the late '90s through early 2000s was largely attributable to U.S. and European corporations taking advantage of cheap labor in countries like India. The industry grew very rapidly as global corporations realized significant cost savings from outsourcing non-complex, non-strategic tasks, such as those related to human resources, financial processes (i.e., A/R, A/P, billing and document management), other administrative processes and customer services (i.e., customer call centers). These fairly mundane tasks, outsourced to 3rd party vendors, can be categorized within the BPO umbrella. The chart above provides some high-level categories within BPO; additional examples include the following:

- Customer service / tech support: Large U.S. wireless operator outsources inbound customer calls to delivery centers based in India.

- Large retail bank outsources document management services such as printing and mailing of statements. 3rd-party vendor manages the flow of customer data into a centralized database that can print out and mail customer statements.

- Target (TGT) decides to outsource the revenue cycle management process. 3rd-party vendor handles collection and maintenance of all data for the company's accounts receivables.

- T-Mobile UK hires Infosys to manage all activities related to the finance department , including customer finance (credit referrals, billing and commissions, fraud), procurement & control (accounts payable, procurement ops and support, IT capex), accounting and commercial finance (reporting, planning, marketing controlling).

- Large Australian bank hires Infosys to fix errors in its payroll process.

Application Outsourcing

Companies rely on 3rd-party vendors to build software from scratch when requisite packaged software does not exist. Large banks like Deutsche Bank and UBS benefit from outsourcing to specialty vendors such as Luxoft and EPAM, which possess a thorough understanding of their clients' industries and can quickly develop software tailored to address a specific need. Luxoft focuses predominantly on application development, a service that is primarily project-based and involves customizing a solution from scratch. Unlike the Indian vendors that work across the IT services spectrum (BPO, infrastructure and application outsourcing), Luxoft focuses on the industries in which it has the greatest expertise to develop unique and sophisticated software solutions for clients. The company's high-quality output is best exemplified by real projects; we have provided a selection of these initiatives below.

1. Designed a market data analysis system to pull real-time and historical equity and equity derivatives data for a global top 10 investment bank.

- DB required an application to execute time-series analysis on equity and equity derivatives market data to help develop internal trading strategy and portfolio management

- The requirements included:

- Real-time capture of every tick from multiple exchanges

- Maintain a database of historical quote and trade data

- Provide data filtration capabilities to remove unwanted data, such as block trades and off-exchange trades

- Calculate multiple price-related values, including VWAP (volume-weighted average price), TWAP (time-weighted average price) and average spread

- Luxoft ultimately delivered a solution which reduced costs for the client through:

- Real-time integration between exchanges and bank's operations

- Improved performance, latency and stability of real-time market data retrieval

2. Prime brokerage client portal for a large global investment bank.

- Luxoft created an online portal for prime brokerage clients, which provided access to accounts, investment products and customer service.

- The portal allows customers to receive information on:

- Executions linked to orders, allocated trades, cleared trades, current positions and balances, cash and securities collateral, margin and margin calls

- The portal allows self-service functions such as:

- Make queries on missing trades, not-recognized trades

- Withdraw and deposit cash

- Create fx requests

- Withdraw and propose new securities collateral

- Receive alerts (expired trades, forthcoming expirations)

The project required 40+ Luxoft staff and over 1 year of development time.

3. Liquidity management and analysis system for a large global investment bank.

- Following the global financial crisis, this client hired Luxoft to develop a new system that would measure and analyze end-of-day liquidity in a way that complied with Basel II requirements.

- This bank originally began the development with support from an Indian vendor, but as the system's complexity and size hit critical levels, it selected Luxoft as the new partner.

- Luxoft delivered the project on time and within the budget, and the system was able to provide the following functions:

- Management of short-term liquidity gaps against existing limits

- Management of overnight funding exposure

- Collateral management

- Maintaining liquidity reserve in the form of liquid assets

- Analysis of liquidity drivers (ratings, regional crises, insecure funding, insufficient collateral, etc.) for stress testing

4. Virtual data room (VDR) for a leading financial print and media company in the UK.

- Luxoft developed a secure, controlled-access VDR to facilitate due diligence for M&A transactions, IPOs and audit transactions.

- Ensuring confidentiality of the documents in a virtual repository extremely important.

- Client required high-quality, reliable software to eliminate risk of financial or legal consequences resulting from data leaks.

5. Loan collection management system for a large Russian corporate and retail bank.

- Luxoft developed a loan collection management system to monitor unpaid debt and to automate and streamline the collections process.

- High growth of Russian corporate and retail lending resulted in increased risk of delinquent debt.

- Luxoft's solution included functionality for the following:

- Debt management

- Automated credit agreement tracking for assignment or removal of bad debt status

- Segmentation of debtors with recommended collection approach

- Ability to track employee performance on assigned recovery

Developing Industry Expertise Results in Deeper Client Relationships

Luxoft's go-to-market strategy is to continue developing proficiency in its core industries. The success of this approach is demonstrated by the revenue generated from clients in financial services and automotive; these two verticals account for nearly 80% of total revenue. Between FY 2011 and FY 2015, revenue from financial services and automobile grew at a CAGR of 37% and 40%, respectively. While Luxoft is well known for its financial services expertise, thanks in large part to Deutsche Bank and UBS (which we discuss later in this report), revenue from automobile clients continues to account for significant growth.

The company's expertise in the automobile sector is human machine interface (HMI). In a consumer vehicle, HMI is essentially a tool that presents information to the driver (e.g., a digital cluster that shows how fast you're driving, how much gas you have left, etc.). Luxoft has relationships with Tier 1 auto suppliers (like Harman) and plays a vital role in ensuring functionality of software for the affiliated hardware to be implemented in a vehicle.

Human Machine Interface

Source:Luxoft presentation on automobile

A good example of HMI technology is the heads-up display (also known as HUD), which is a transparent display installed right above the driver's side of the dashboard or integrated directly into the windshield, allowing the driver to see data (current speed, speed limit, directions from navigation, gas tank indicator, etc.) without looking away from their direct viewpoint.

Heads-up Display

Source:Luxoft presentation on automobile

The coding required to build the software behind this kind of technology is extremely complicated, and manufacturers rely on Luxoft to ensure that this technology works seamlessly. While revenue from the automobile segment accounts for only 12% of total revenue, the industry is rapidly expanding and evolving to incorporate sophisticated components like the HUD. The market for the HUD alone is expected to grow from 6.6 million units in 2012 to over 75 million units in 2020, per LXFT.

Other examples of the company's projects in automobile are below:

1. Interactive tutorial for in-car infotainment system for Ford (F).

- Ford decided to develop an interactive tutorial to help new drivers and auto dealers learn the in-car communications and entertainment system as quickly and conveniently as possible.

- Luxoft created the MyFord Touch Guide as a multi-platform application that is able to run on iOS, Android and Windows devices.

- Virtual avatar provides narrative and video instructions on exactly how to engage various features.

- The company completed the project within the 6-month requirement as set forth by Ford.

2. Augmented reality navigation system for BMW (BAMXY).

- Luxoft designed solution for a BMW's new 7 Series line.

- The system provides driving and navigation guidance with the interaction system overlapped directly to the environment (i.e., directly on the windshield).

- Numerous functions, including:

- Recognition of current car position and orientation on road

- Filtering and tracking of detected vanishing points

- Vanishing point and lane borders detection for camera position estimation and road width estimation

- Example of road modeling, speed limit, actual speed and next action hint

3. 3D digital map data processing for a European manufacturer of automotive infotainment, multimedia and navigation systems.

- Luxoft brought in to develop algorithms for processing and visualization of major types of 3D objects required for digital map compilation.

Screenshot of 3D navigation map

4. Car infotainment system for a large vendor of automotive electronics, multimedia and related systems (which we suspect to be Harman, Luxoft's 3rd largest customer).

- The client looked to the company to jointly develop a universal car infotainment and multimedia system that would include telephony, internet communications, onboard navigation and interactive speech control as a platform for a number of high-end vehicle manufacturers (think BMW, Mercedes, etc.).

- Luxoft cooperated with several other hardware and software vendors to deliver a complex solution with multiple applications, including:

- Telephony communications (hands-free and mobile internet), navigation, TV, emergency calling

- The system design encompassed functionality across numerous tasks (see below)

At the company's Investor Day last November, Harman's CEO made several remarks that confirmed Luxoft's reputation for providing high quality services in the automobile sector. Harman's CEO suggested that Luxoft will play an increasingly larger role in the automotive space and he will remain a long-term customer. Some of his quotes are below.

Luxoft Stands Out Due to Unique Approach

Quantitative metrics reinforce the positive qualitative commentary above. Relative to the rest of the industry, the company boasts the highest billing rate at $77k per IT employee. We believe Luxoft's unique approach to software development is a meaningful contributor to the premium its engineers command over the competition.

Luxoft Commands High Bill Rate

More impressive still is that the bill rate has grown over the past five years, from $62k per employee to $77k per employee. We attribute this growth to two factors: (i) a growing proportion of fixed-price contracts, and (ii) deeper penetration of clients. In recent years, Luxoft has restructured its pricing with large customers like Deutsche Bank and UBS from time-and-materials (T&M) contracts to fixed-price ones. Under a fixed-price arrangement, Luxoft has more control and flexibility to scale staffing requirements, prompting opportunities for increased margins and revenue per employee. In addition, the company has made tremendous strides in further penetrating large clients. During our due diligence, we learned that projects become more predictable as relationships with vendors lengthen, enabling LXFT to streamline project management.

Bill Rate Growing

Source: Company filings

The importance of focusing on application development was also highlighted in Cowen's Mid-Year 2015 IT Spending Survey published on May 26, 2015. The survey included respondents across a variety of sectors and titles. In terms of spending, Cowen found that application development was considered the top priority, garnering 34% of the votes, materially greater than the 20% received in each of the prior two surveys.

Cowen Survey Highlights Application Development as Top Priority

Source: Cowen Mid-Year 2015 IT Spending Survey

The survey was particularly relevant to Luxoft because participants from the financial services sector comprised the largest group of respondents, at 36% of the sample size (followed by manufacturing at 25% and healthcare pharma at 16%). With Luxoft generating two-thirds of its revenue from the financial services sector, we believe this survey supports our thesis that its market opportunity in financial services will grow as companies respond to new government regulations.

Abundant Talent in Central and Eastern Europe

Based in Eastern Europe, Luxoft benefits from the highly educated workforce prevalent in this geography. Nearly one in five students in the CEE region will graduate with degrees related to science, technology or engineering. This excerpt from EPAM's 10-K provides additional color on the quality of talent in Eastern Europe:

Demographic Comparison: CEE vs. India

Source: J.P. Morgan report on LXFT

Luxoft benefits from this attractive demographic, as 80%+ of its employees have at least a master's degree. Additionally, 79% of employees have at least five years of professional experience.

Attrition Relative to Industry

Source: Company filings and press releases

Employee attrition is a critical metric when analyzing companies in the IT outsourcing space. Luxoft's low attrition is especially impressive when measured against revenue growth over the past twelve months. Compared to peers, the company stands out with the lowest attrition and highest LTM revenue growth rate.

Attrition vs. LTM Revenue Growth

Source: Company filings and press releases

The low attrition is attributable, in part, to the higher salaries offered by Luxoft relative to competitors. For the fiscal year ended 3/31/2015, we estimate that the average employee was paid ~$41k in USD terms, significantly higher than the GDP per capita in the company's largest geographies.

Average Salary Relative to GDP / Capita

Source: CIA World Factbook

Note: Romania and Poland metrics as of FY 3/31/2014.

Note: Estimated salary calculated by dividing total COGS by average IT employees in FY 3/31/2015.

V. Deutsche Bank and UBS Demonstrate High Customer Value Proposition

Luxoft's multi-year relationships with its two marquee clients, Deutsche Bank and UBS, are a paradigm for its potential to augment growth via new client acquisition.

Deutsche Bank

The company's history with Deutsche Bank demonstrates its ability to establish deep customer relationships. Luxoft's engagement with Deutsche Bank began in 2003 through a referral. Initially, it provided a 30-person team to assist DB with application support for the cash equities desk. Upon successful completion, Luxoft was engaged for numerous other projects. Ultimately, its mandate expanded to encompass areas such as fixed income and derivatives as the company was recognized for its innovative and scalable solutions.

Examples of projects that Luxoft has completed for Deutsche Bank include:

1. Development of a web-based lending tool called COMPAS (comprehensive approval system) .

- The Risk Management Advisory ((RMA)) group at DB wanted to develop an internal, automated credit decision engine which would assist in evaluating credit risks of potential new clients.

- Luxoft developed COMPAS, an advanced web-based lending tool used as a credit assessment tool and scoring model for clients ranging from large corporate borrowers to middle-market and commercial accounts as well as retail customers.

- Goals for COMPAS included:

- Automation and structuring of loan origination

- Risk quantification (score, rating)

- Approval processing

- Some specific functions include:

- Identifying historical and existing exposure to client (on DB's entire system)

- Expected loss calculation

- Collateral analysis

2. Project StRIDe

- Large-scale effort aimed at automating and optimizing the financial infrastructure of the global banking unit.

- Created central warehouse for all of the investment bank's risk and finance data

- DB has many different data streams from numerous systems (risk systems, business info systems, systems from various units, desks, geographies)

- Over 1,000 data streams from more than 100 transaction systems

- The implementation involved multiple segments across the organization, including retail banking, commercial and investment banking and asset management.

- Luxoft is overseeing 100% of the development.

- Project StRIDe helps DB create better internal financial reporting (P&Ls, end-of-day flash reports).

- Optimizes compliance process, as management is required to sign documents to attest to accurate records of the firm.

- Extremely complex project with hundreds of thousands of man hours already spent since launching in 2012.

- The budget for this project went from tens of millions to over hundreds of millions of euros.

3. Client clearing tool for the investment bank (corporate finance).

- Luxoft helped to re-develop and upgrade a proprietary DB system that's been used by the investment bank for over 20 years.

- The core function of the system is to manage conflict clearing in the investment bank.

- A banker must clear the client in this system prior to engagement.

- Example: DB banker must make sure that in an M&A engagement, DB isn't representing both sides of the transaction.

- Luxoft manages/maintains this system and is responsible for upgrading the system, which occurs 3-4 times annually.

4. Credit risk management system for global lending.

- Luxoft created a credit risk modeling system used by DB's credit officers and certain investment bankers.

- The credit decision model would assist in evaluating credit risks of potential new clients and monitoring existing clients.

- A complex interface with numerous inputs allows for testing of various scenarios.

- Example: DB considers making a loan to a South Korean corporation that exports products primarily to China and Russia. The credit model forecasts how a change in the South Korean Won and Chinese Yuan would affect this potential client's earnings and ability to pay.

- The model has hundreds of data points including commodities, currencies, fixed income exposure.

- Very integral to the core lending function, and Luxoft handles a majority of the work.

- This project is integrated with Project StRIDe mentioned previously.

5. Developed customer relationship management ((CRM)) solution for Deutsche Bank's global banking business.

- DB looked to Luxoft to develop a comprehensive CRM platform which would aggregate customer data from numerous existing systems.

- Legacy systems included Dealogic, BoardEx, Lotus and other proprietary systems

- Users included sales managers, global relationship managers, and senior executives within Global Banking (both commercial and investment bank).

- Over 5,000 users globally

- The project required over 30 Luxoft staff and over 5 years of development and maintenance work.

In 2012, DB came under immense pressure to reduce costs amid the European debt crisis. During that time, the bank undertook a vendor consolidation and reduced the number of IT services vendors from 12 to 4. Luxoft survived that consolidation and gained business previously given to other IT outsourcers. DB also restructured its pricing arrangement with the company to move away from T&M to fixed price, forcing Luxoft to temporarily sacrifice margins. Luxoft fulfilled DB's requests during the course of that turbulent transition and, consequently, was named a key strategic vendor in 2012, leading to an expanded footprint within the investment bank. As a result, ~70% of Luxoft's DB revenue is now generated from the investment bank, while the other 30% comes from the treasury services segment that offers cash and liquidity management services for mostly large corporate clients.

UBS

Luxoft's success with UBS began with a history that mirrors the Deutsche Bank story. This relationship began around 2006, when UBS opened its Moscow office and management looked to bring in local IT resources for application support on the equities trading desk within the investment banking division. As Luxoft repeatedly impressed UBS, the relationship soon grew out of the Moscow office to other business segments and geographies. The relationship reached a turning point in 2012, when UBS began to wind down its fixed income business and relied on Luxoft for IT support as a majority of the existing employees were laid off in that division. Luxoft's performance on that transition was well received by UBS management and resulted in its recognition as a strategic vendor. Luxoft's headcount at UBS more than doubled, increasing from 600 to roughly 1,300 over the two-year span from 2013 to 2015. In FY 2015, the company generated $105 million of revenue from this relationship alone, counting UBS as its second-largest client.

Snapshot of Deutsche Bank and UBS

Deutsche Bank

UBS

Revenue

Customer Since

2003 (13 years)

2006 (10 years)

Allocated Resources

2,600 Employees (30 in 2003)

1,300 Employees (600 at LXFT IPO in 2013)

Other Vendors

Accenture and TCS

Accenture, CTSH and EPAM

Revenue by Bank Segment

~70% Investment Bank / ~30% Treasury/CFO & Other

~80% Investment Bank / ~20% Wealth Management

Other

MSA renewed in 2016

- 5-year term

Currently in 5th year of contract.

Admittedly, the level of concentration at DB and UBS (which together accounted for 56% of total revenue in FY 2015) appears concerning at face value. However, we perceive the concentration risk to be less pronounced given Luxoft's deeply embedded position with these clients amid an uncertain and complicated regulatory environment. In the post-financial crisis era, regulators have unleashed an avalanche of compliance and regulatory demands, and the implementation of final rules is not even complete and the list continues to grow - as of December 2015, only 75% of rule proposals have been finalized .

Banking Industry: Overview of Regulatory Timeline

Source:Analyst Day presentation

Dodd-Frank: Overview of Rules Pages Published Over 5 Years

Source:Davis Polk

Considering both these regulatory trends and feedback from former Deutsche Bank and UBS employees, we feel confident that Luxoft will remain deeply entrenched with its core banking customers. Earlier this year, CIO magazine published an article discussing StRIDe, a major internal IT initiative at DB aimed at creating a central warehouse for all of the investment bank's risk and finance data. Interestingly, Luxoft was listed as the sole software developer for this large-scale engagement designed to aggregate information from all of the bank's legal units (~1,000 data streams and more than 100 transaction systems).

Overview of Project "StRIDe" at Deutsche Bank

Source:CIO

Growth Outside of Top 5 Customers

With Luxoft still in its nascency, customer concentration is not an immediate concern, particularly as the company expands beyond its top five customers. In fact, LXFT has been experiencing solid revenue growth in its smaller accounts, with sales from clients outside of the top five growing from $56 million in FY 2011 to $228 million in FY 2016. In FY 2016, revenue outside of the top 5 grew at an astounding 56%.

Revenue Growth Excluding Top 5 Customers

Source: Company filings

Luxoft's portfolio of high-potential accounts ("HPAs") grew from 12 at the IPO in 2013 to more than 40 today. Clients are classified as HPAs if management believes the accounts have the potential to reach at least $5 million in recurring annual revenue within the "short to mid-term." On the FQ3 2016 earnings call, management disclosed that HPA customers generated more than 177% growth year over year in the 9-month period:

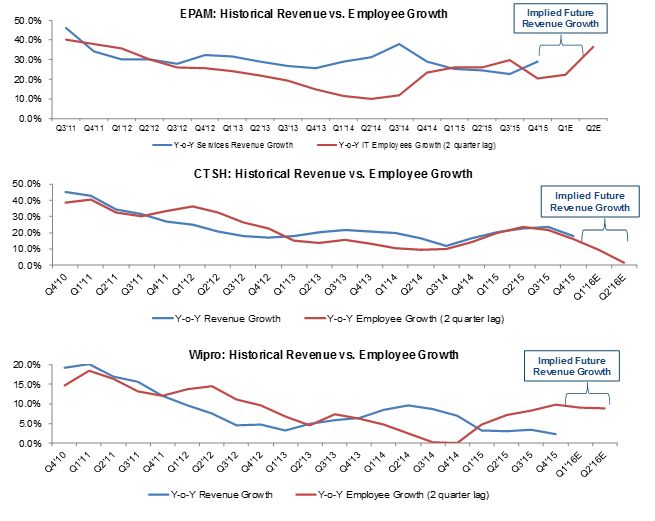

VI. Employment Growth a Good Indicator of Future Revenue Growth

In the IT services industry, as in other asset-light and people-oriented businesses, talent is one of the most valuable resources. As such, employee growth is a vital metric when analyzing businesses like Luxoft, which rely on human capital. We have observed a strong correlation between employee and revenue growth for IT outsourcing vendors. Specifically, employee growth on a two-quarter lagging basis appears to have historically been a fairly predictive indicator of future revenue growth. The correlation coefficient (a measure of linear correlation) between the two variables was 79% for CTSH and ~60% for Wipro, also suggesting near-term employee growth may be a relevant indicator of revenue growth.

Quarterly Employee vs. Revenue Growth

Source: Company filings

Unfortunately, Luxoft's publicly available quarterly growth data is only obtainable starting in 2013, making it difficult to determine whether a strong correlation exists, as we'd prefer more data. The chart below shows what the historical correlation has been since FQ1 2015.

However, the company posted robust employee growth over the past few quarters (22% in FQ3'16 and 23% in FQ2'16), giving us confidence that the pipeline of current activity remains extremely strong.

LXFT Employee Growth

Source: Company filings

One data point we employ to track current demand for employees is Luxoft's Russian language careers website . The page lists job postings by function and geography, and listings are updated on a daily basis. Historical data is accessible via the Wayback Machine , an online web archive service.

Before July 2015, the number of job postings consistently remained around 350 for total employees. Beginning in July and through late August of 2015, we saw total job postings and development positions grow to ~400-450. Recently, we saw this spike to ~600, implying that demand remains very strong. This data may prove a reliable proxy for future employee growth - and thus, future revenue growth - with sudden spikes or declines signaling fluctuation in the current state of customer demand.

Historical Job Postings

Source:Luxoft's Russian language careers website and the Wayback Machine

VII. LXFT vs. EPAM

EPAM Systems is Luxoft's primary CEE competitor in the emerging IT services industry. Like Luxoft, EPAM focuses predominantly on application development and employs talent in similar geographies, principally Belarus (Luxoft has no presence), Ukraine (#1 Luxoft location) and Russia (#2 Luxoft location). Revenue per employee is higher at Luxoft ($76k vs. $65k), but attrition levels have historically been similar, between 10% and 12%. At a high level, the firms appear fairly similar, even sharing some customers: UBS is EPAM's largest customer and Luxoft's second largest. Admittedly, this overlap in value proposition and edge makes us bullish on EPAM's prospects (i.e., focus on application development, access to talent in CEE, etc.). With that said, our work clearly demonstrates Luxoft to be the higher-quality provider.

At a Glance: LXFT vs. EPAM

Source: Company filings

One way to distinguish Luxoft from EPAM is by comparing the revenue generated from T&M versus fixed-price contracts. For the latest LTM period, LXFT generated 55% of revenue from fixed-price contracts as compared to 13% for EPAM. Under a T&M pricing structure, clients are billed at a pre-determined rate for the total hours worked. Vendors sign a MSA with clients that includes a rate card outlining the hourly rates for each level of employee (i.e., the rate set for entry level, experienced programmer, project manager, etc.). Under fixed-price contracts, vendors are paid a pre-arranged fixed price and are responsible for managing their own resources. The primary difference between the two arrangements is that with fixed-price contracts, the vendor can potentially make a greater profit (relative to T&M, where margin is fixed), while also facing the risk of exceeding the estimated cost.

Luxoft and EPAM have different contract structures due to their different delivery models. There are two widely adopted delivery models for offshore IT vendors: staff augmentation and managed services. EPAM derives most of its revenue using the staff augmentation model, while Luxoft generates ~55% of revenue from managed services. The most widely adopted model for offshore IT services is staff augmentation; however, the industry is gradually shifting to the managed services model. Under the staff augmentation model, pricing is based on T&M, and companies pay for each staff member at an agreed-upon rate. Staff augmentation is beneficial to companies looking for rapid access to temporary employees with specific capabilities and skills. Additionally, there's no waste of time or resources for companies trying to recruit new employees to fill needs that may only be temporary. When considering an offshore vendor, customers seek the lowest cost per contractor, encouraging stiff competition among suppliers.

While staff augmentation is ideal for short-term solutions, the model does not work well for customers seeking a long-term partnership. When used as a long-term solution, the staff augmentation model is more expensive. The cost benefit gained in the short term (through avoidance of HR costs associated with hiring) is lost. Perhaps even more significant is that reliance on staff augmentation as a long-term solution could lead to poor management of resources. Under this model, the company is responsible for managing the vendor's resources. This gives the vendor limited incentive or accountability for the outcomes and quality, as no specific requirements or deliverables are specified in the staff augmentation contract.

Another significant issue with the staff augmentation model is the risk that knowledge will be retained with the contractors and not with the hiring organization. As contractors spend more time on a specific project, they accumulate knowledge and capabilities that become invaluable. The vendor could potentially use this knowledge to hold the customer hostage, leading to a more permanent engagement utilizing an expensive delivery model.

The alternative delivery model is known as managed services. Under this model, vendors agree to deliver a specific capability or functionality with a desired level of results for a fixed price. This differs significantly from staff augmentation, which revolves around defining cost inputs; with managed services, the vendor is committed to delivering an outcome at a fixed price. This model requires a higher level of trust as customers cede more control to the vendor. The customer defines the requirement and desired outcome, but the vendor is responsible for managing all resources, assuming the risk of meeting the delivery commitment. Since engagements are on a fixed-price basis, vendors are highly incentivized to maintain high productivity, as any delays would result in cost overruns borne solely by the vendor, not the customer.

Managed Services vs. Staff Augmentation

Source:CGI white paper

Based on our discussions with former customers and executives in the industry, the utilization of one model over another is the best way to distinguish Luxoft from EPAM. Staff augmentation was the primary delivery model for Luxoft several years ago, but between FY 2011 and FY 2015 revenue from T&M declined from 91% of total revenue to 41%.

Luxoft's success in implementing this model with clients is evident in its enduring relationships with DB and UBS, customers since 2003 and 2008, respectively. Due to the long-term nature of these relationships, projects become more predictable, creating an opportunity for the company to maximize efficiency. We think this explains, in part, why LXFT's gross margins are higher than EPAM's. While EPAM's gross margins have declined over the past 7 years (EPAM management attributes the decline primarily to wage inflation), Luxoft has managed to keep gross margins stable at 42-44%.

VIII. Conclusion

As corporations increasingly look to utilize technology to boost their competitiveness, the world will turn to providers of high-end developers such as Luxoft. Who programs the dashboard in your car? Who builds the capital adequacy reporting software of our leading financial institutions? How do local retailers build their online marketplaces? The United States simply does not graduate enough software engineers to satisfy the burgeoning demand for customized application development. This shortage of talent will result in the continued outsourcing to companies like Luxoft that specialize in recruiting, training and mobilizing teams of highly talented and experienced programmers. We believe Luxoft is in the early stages of a rapid, long-term growth trajectory that its Indian peers experienced in the late '90s and early 2000s. If the company repeats even a quarter of those achievements, its shares will be a tremendous investment.

See also Twitter: Sale Or Nothing on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}