Lucky 13! 13-Year Investment Returns

- U.S. stocks have performed extremely well in the past 13 years, but bonds have not

- Stock performance is in the top decile of all 13-year stock returns over the past 96 years

- Quantitative Easing (QE) has been the driver. What will happen when QE ends?

It’s official. The return in the 13 years following the 2008 stock market crash has been terrific. In this article I examine the history of 13-year returns on stocks and bonds to put the most recent 13-year period into perspective. It has indeed been extraordinary.

A phenomenal recovery

Aside from a quick down blip in the first quarter of 2020, the U.S. stock market as measured by the S&P500 has skyrocketed since 2008, growing about 600% when dividends are included. In addition to the steepness of this recovery, it’s the longest recovery on record if you don’t view the 2020 blip as ending the recovery.

It should feel to most investors like this past 13 years is the best ever because it almost is. The following section examines all 85 13-year time periods ending in December.

13-year investment return history

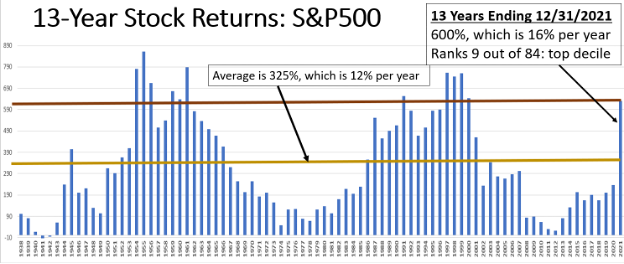

The following exhibit shows all of the 13-year returns on stocks. The U.S. stock market as measured by the S&P500 returned 600% in the 13 years ending December 2021 (far right bar in the exhibit), which is 16% per year. It ranks 9th out of 84 13-year periods, so top decile.

The highest 13-year return is 863% earned in the 13 years ending December of 1955, averaging 19% per year.

As you can see in the last 2 bars on the right, moving from 2020 to 2021 replaces 2008’s 37% loss with 2021’s 30% gain, propelling the 13-year return upward.

Returns average 323% (12% annualized) over the full history, so the recent return is 185% of average.

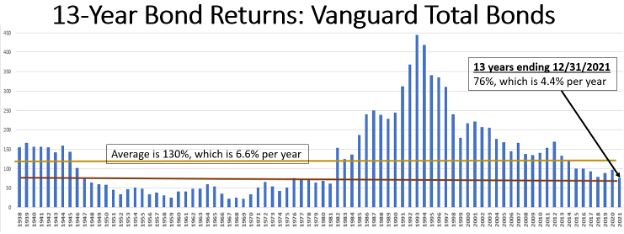

By contrast, bond returns have been below average, returning 4.4% per year versus the average 6.6%. Bonds earn their coupon plus capital gains or losses. Falling coupons generate capital gains, but in this case total returns have been below average because coupons have fallen well below average.

What’s next

Investment returns over the past 13 years have been driven by an experiment called Quantitative Easing (QE). Warren Buffet observes that QE is an experiment of magnitude and consequence that has never been conducted before. No one knows how it will end and what its effects will be, but it appears at this time that QE will be gradually reduced starting in 2022.

Much of this recovery has been orchestrated by the Federal Reserve with its Zero Interest Rate Policy (ZIRP), an aspect of QE. ZIRP has required massive money printing of around $5 trillion to buy up bonds, manipulating their prices above natural levels. But inflation is now forcing the Fed to “taper” -- reduce their bond buying. As the manipulation ends, bond yields will increase, especially if inflation persists as it likely will.

Increases in bond yields drive bond prices down. It should also drive stock prices down as analysts discount future earning at a higher discount rate, and bonds regain their position as a lower risk alternative to stocks.

The end of ZIRP is the end of stock and bond price manipulation. As Warren Buffet observes “When the tide goes out, we see who has been swimming naked.” Without this “invisible hand” stock and bond prices will be determined by investors, as was the case before QE.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Ron Surz

Ronald Surz is co-host of the Baby Boomer Investing Show and president of Target Date Solutions and Age Sage, Target Date Solutions serves institutional investors, namely 401(k) plans. Age Sage serves do-it-yourself individual investors. His passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book Baby Boomer Investing in the Perilous 2020s and he provides a financial educational curriculum.Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path, Soteria personalized target date accounts, and Age Sage do-it-yourself investing. He is also co-host of the Baby Boomer Investing Show.

Read Ron's Bio