Credit: Shutterstock photo

Credit: Shutterstock photoBy Brett Kearney :

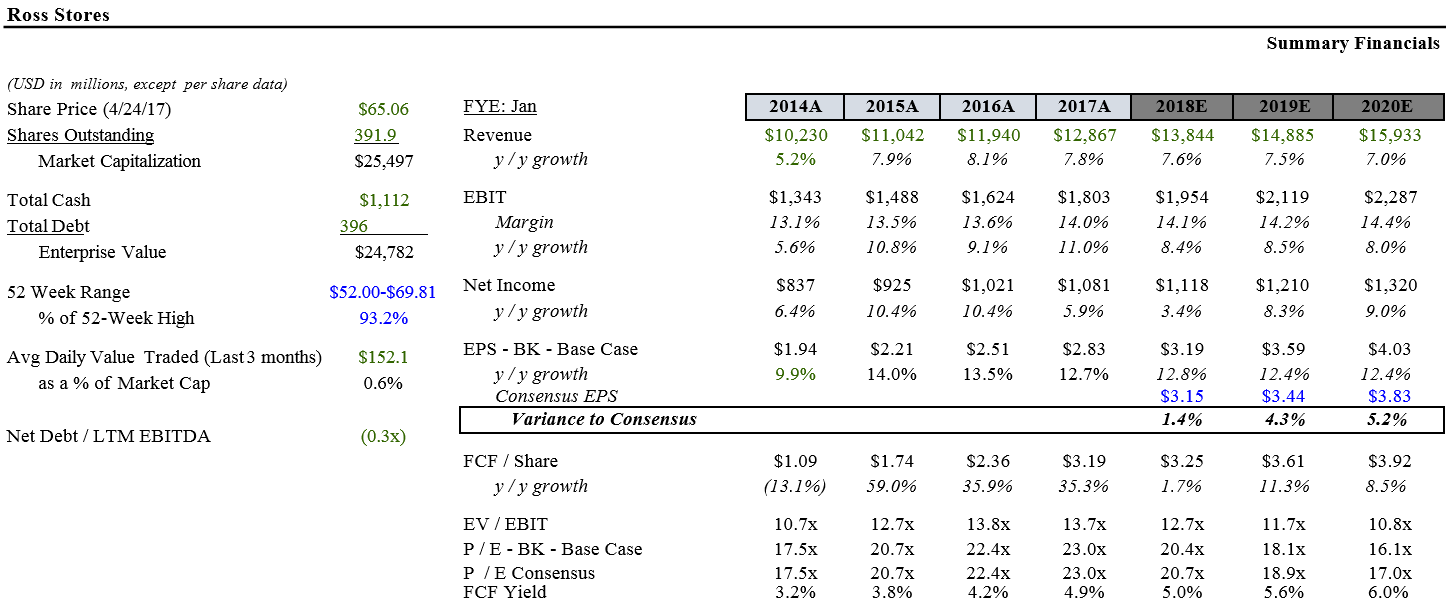

Target Price and Rationale

1.75 Years. Target Price of $83 per share, implying 30% total return (including dividends) and 16% IRR. Based on 20.7x forward P/E multiple (equivalent to the current forward multiple and below the 22x that ROST has traded at, on average, over the past three years).

The company's moat is intact and it is well-positioned to take further share from a deteriorating department and specialty store channel.

Significant white space remains within the underpenetrated U.S. off- price retail market and the company's low price points and treasure hunt shopping environment insulate it from the ravages of e- commerce.

Relevant Comps

- The TJX Companies Inc. (NYSE: TJX ) - currently trades at 20.2x forward P/E multiple and has traded at an average forward P/E multiple over the past five years of 19.5x.

- Burlington Stores, Inc. (NYSE: BURL ) - currently trades at 24.3x forward P/E multiple and has traded at an average forward P/E multiple over the past five years of 22.9x.

Catalyst

- Department and specialty store closures over the next 18 months

- company's expansion to the Northwestern U.S. region and deeper penetration of the Midwestern U.S. region

Ross ( ROST ) is a leading off-price apparel and home merchandise retailer with a total of 1,533 locations across 36 states. The company sources merchandise opportunistically either through acquiring close-outs that have been returned or refunded to vendors by department stores or through purchasing in quantities large enough to enable vendors to lower their own production costs. Ross operates a no-frills store format and passes the combined savings (from sourcing and lean store design) on to shoppers, resulting in prices 20-60% below those of department and specialty stores that sell similar merchandise. Stores receive between 3 - 5 new deliveries per week providing an exciting and fresh selection of merchandise while lean in-store inventories (that turn ~12x per year) create a 'buy now' mentality in the shopper.

Key Thesis Points:

There Remains Significant Runway for Growth

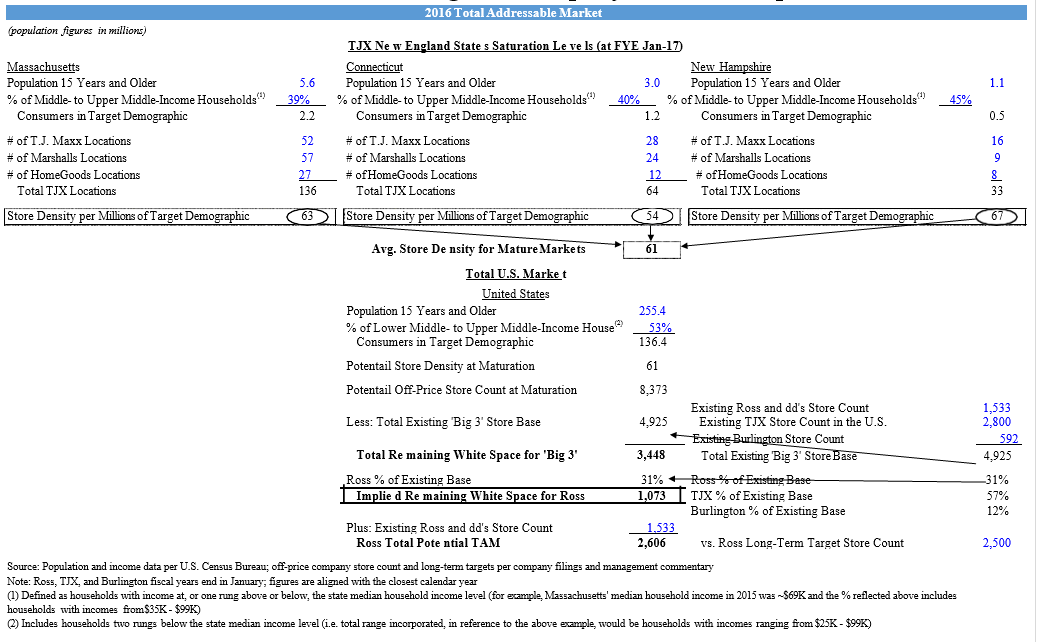

Considerable Remaining 'White Space' in TAM (please see exhibit below right) - assuming the off-price retail industry achieves penetration levels in the U.S. equivalent to those in the more saturated New England States of Massachusetts, Connecticut, and New Hampshire (where Marshalls and T.J. Maxx have been operating for ~50 years), then the TAM for the 'Big 3' off-pricers (Ross, TJX, and Burlington) represents ~8,300 total locations. Backing out the existing base of stores of the combined 'Big 3,' we get to ~3,400 locations of remaining 'white space.' Of the existing base, Ross accounts for ~31%. Assuming the company will at least procure an equivalent share of the remaining 'white space,' then this implies nearly 1,100 stores of additional runway for Ross and a total TAM for the company (adding in its ~1,500 current locations) of ~2,600 total stores. This adds credibility to management's stated long-term target of 2,500 total stores.

- Ample Supply of Merchandise Exists (per primary research contacts) -

- "Still there is a lot of just unplanned excess in the market now. Right now, nobody can sell apparel to save their life except for the Ross and T.J. Maxxs." - Senior Analyst, U.S. Apparel at Kantar Retail

- "Manufacturers know that the department store base is a diminishing area for them. And, so they are looking for how do they stabilize or grow their business. So, they are looking to the off-pricers of the world because they are one of the few segments of retail that is doing well." - VP of Planning & Allocation at TJX Companies

E-Comm is a Less Significant Threat for Ross

- Low Price Points - The company's average unit retail is $10. If you assume the company pays around $6 for that item (based on all-in gross margins - that incorporate distribution & freight and occupancy costs - in the ~30% range) the merchandise margin is $4. This clearly does not leave much room to cover packaging and shipping costs and still generates a profit. Further, returns in U.S. apparel online retailing average 20-40% (source: ASOS ). Processing returns and paying someone to unpackage, inspect and then repackage that merchandise quickly takes the model into the red. This has been evidenced by the spectacular popularity (and impressive capital raises), yet lack of sustained profitability of online off-price type businesses such as Gilt Groupe (ultimately had to be sold last February to Saks' parent company Hudson's Bay Co., which just wrote off nearly half of the $250 million it paid for Gilte) and Rue La La (acquired by eBay ([[EBAY]]) as part of its March 2011 purchase of GSI Commerce, but quickly sold back to GSI's founder due to its noted profit dragging effect).

Primary research contacts provide additional color on this point:

- "With e-comm, the lower the price point the more there is not enough dollar gross margin to cover that and yield a profit." - Former CEO & Chairman of Sears Canada and Lazarus Department Stores

- "Amazon is definitely shooting for the best brands they can get. That gives them immediate fashion credibility. They are going to keep working their way upwards. They will keep going up the value chain." - CEO at Multi-Brand Apparel Vendor

- "A lot of my vendors tell me that Amazon's orders aren't huge. So, they might buy 10 styles, but they are only buying 120 units - 160 units. So, it is not a lot of volume to the vendors yet. And, Amazon competes at all price points, though I have rarely seen anything in my world that is really under where I am at Century 21" - Senior Merchant at Century 21 (Former Senior Merchant at Ross Stores)

Vendor Reluctance to Sell to Online Discounters - While most apparel designers and manufacturers have learned to embrace e-comm as a major component of their overall business, they still remain averse to selling merchandise to online retailers that sharply discount prices. Given that these prices are available for anyone with an internet connection to see, and the increasing propensity of consumers to comparison-shop, the highly visible discounted prices both damage brand value and create conflict with manufacturers' department store customers.

- "Some brands are unwilling to sell to some of those online companies because if you go online, it is tough to hide it. It creates a lot of visibility for brands that are sometimes very sensitive to the pricing. So, that creates a little bit more noise for those manufacturers with the department stores because it is really easy to say - hey, wow this product, they are selling it at this price, why are you guys selling it to them at this price, you are hurting my business." - VP of Planning & Allocation at TJX Companies

- "One of our brands we did sell to Amazon and we pulled out of it because we weren't sure - Amazon has dynamic pricing where they can shift the prices at 2 o'clock on Wednesday and then come back to the regular price, and we just don't know about it. So, we started having some conflicts with some of our high end department stores, Barney's and Neimans, where it shows up on Amazon and they get a little notice about it." - CEO at Multi-Brand Apparel Vendor

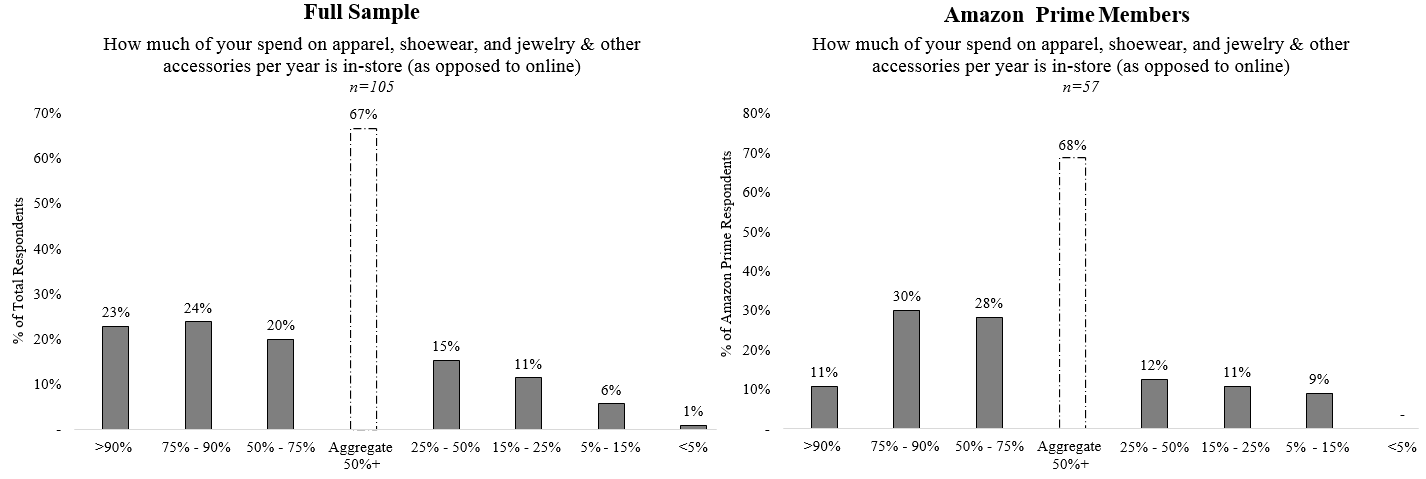

Ross's store shopping environment (the treasure hunt) is unamazonable. The psychological reward from looking, touching, and finding that treasure is not replicable online. This can be seen in the results of a survey we conducted among 105 female consumers across the U.S. with average annual household incomes between $30K and $90K (Ross' target customer demographic is right in the middle of this at $50K-$60K) who have shopped at at least one of Ross, T.J. Maxx, Marshalls, or Burlington Stores at least once in the past two years. As seen in the exhibit below left, approximately 2/3 of this consumer set does 50% or more of their shopping for the items that Ross sells (i.e., apparel, shoewear, jewelry & other accessories) in physical stores vs. online. The strength of this customer sets in-store spending habits, vs. online, even holds across those respondents who are penetrated e-comm shoppers - measured as those with an Amazon Prime membership (see exhibit below right).

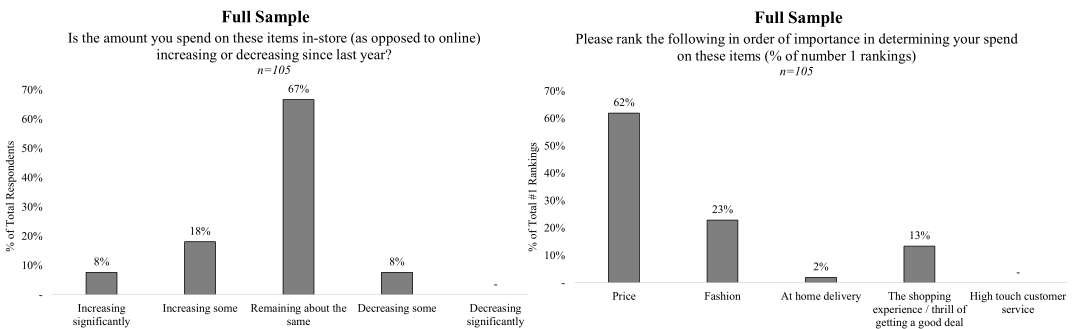

Additionally, of all 105 respondents, a full 93% indicated that the amount they spend on these items in store, vs. online, is at least remaining the same or increasing (please see exhibit below left). Finally, the exhibit below right provides some insight into the purchasing decisions of this customer demographic. Specifically, 62% of all respondents indicated that price was the most important determinant in their spending on apparel, shoewear, jewelry & other accessories. Notably also, more respondents (13% of total) indicated that the shopping experience / thrill of getting a good deal was the most important determinant for them while only 2% ranked at home delivery as the most important factor.

Primary research contacts affirmed that the unique shopping experience that Ross and the off-price retail industry provides is not truly replicable online.

- "If you look at Amazon, it is meant to be easy, it is not meant to be fun. And, it is actually kind of entertainment for her to look and to buy and it is psychologically rewarding to find that treasure. That is difficult to replicate online." - Former company Senior VP of Stores

- "There are a couple of things still that you don't get in the online experience. One of them is that instant gratification of - I am walking out with a purchase." - VP of Planning & Allocation at TJX Companies

Burlington Refining Its Focus to be More Like Ross and TJX Not Going to Disrupt the Sandbox

- BURL has been around since the 1970s. Yes, they have been / are expanding into more categories beyond winter coats, but they appear willing to 'play by the rules' set by the two majors (Ross is ~3x the size of BURL). Burlington today operates ~600 stores and management's long-term target is only 1,000 total locations.

- BURL still has ground to cover in terms of achieving the level of operating sophistication of its larger peers.

- "Burlington has had a lot of growing pains. They have kind of changed their model. If you go out to their stores, sometimes they look great and sometimes they look less than great." - Former company Senior Manager of Purchasing

- "Burlington, they have a larger store size so more space to fill. Their pricing is usually pretty compelling, but not always if they had to buy a lot up-front to fill those larger stores." - VP of Planning & Allocation at TJX Companies

- "Burlington stores tend to be bigger though we are trying to get smaller. Turns are slower though we are trying to speed them up." - Senior Merchandising Manager at Burlington Stores

Growth Algorithm & Path To Profitability:

- 3% Same-Store Sales Growth : Continued solid same-store sales growth of ~3% over the next three years (Company's oldest, California-based, stores have continued to comp at, or above, company average of 4% over the past five years)

- 4-5% Non-Comp Growth : 5-6% square footage growth per year (via management executing on its plan to open ~90 total new stores per year, including deeper penetration of the Midwest and expansion into the Northwest) and new store productivity levels holding at ~80%

- Flattish EBIT Margins in the Low 14% Range : Incremental margins of ~10% on the COGS line as well as ~10% on the SG&A line (consistent with historical levels and conversations with the company) partly negatively offset by greater wage pressures

- Returns of Capital : $850 million of dividends and $2.9 billion of buybacks (in line with the Board's most recent share buyback plan - Ross has repurchased shares in full according to plan each year for nearly 25 years)

= EPS Growth of 12-13% per year

Key Risks:

- Company mislocates stores in new geographic region

- Ross attempts to raise prices into a deeply discounted retail environment and loses customers' love and trust

Metrics To Monitor:

- Same-Store Sales

- New Store Openings

- Margins and Returns

Signposts Of Opposing Thesis:

- Decelerating Same-Store Sales (not as good of a stock, and warranting a lower multiple, if SSS drop consistently to ~1% range)

- Increased Number of Store Closures

- Deterioration in Implied New Store Productivity Levels

Multiple-Based Valuation:

APPENDIX: Unit Economics And New Store ROI

(Editors' Note: This is a republication of an entry in the Sohn Investment Idea Contest . All figures are current as of the entry's submission - the contest deadline was April 26, 2017).

See also Revisiting Taiwan, Japan For Updates On iPhone 8 Launch, Memory Supply, Passive Component Supply, And The TMC Deal on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}