Credit: Shutterstock photo

Credit: Shutterstock photoBy Adam Xiao :

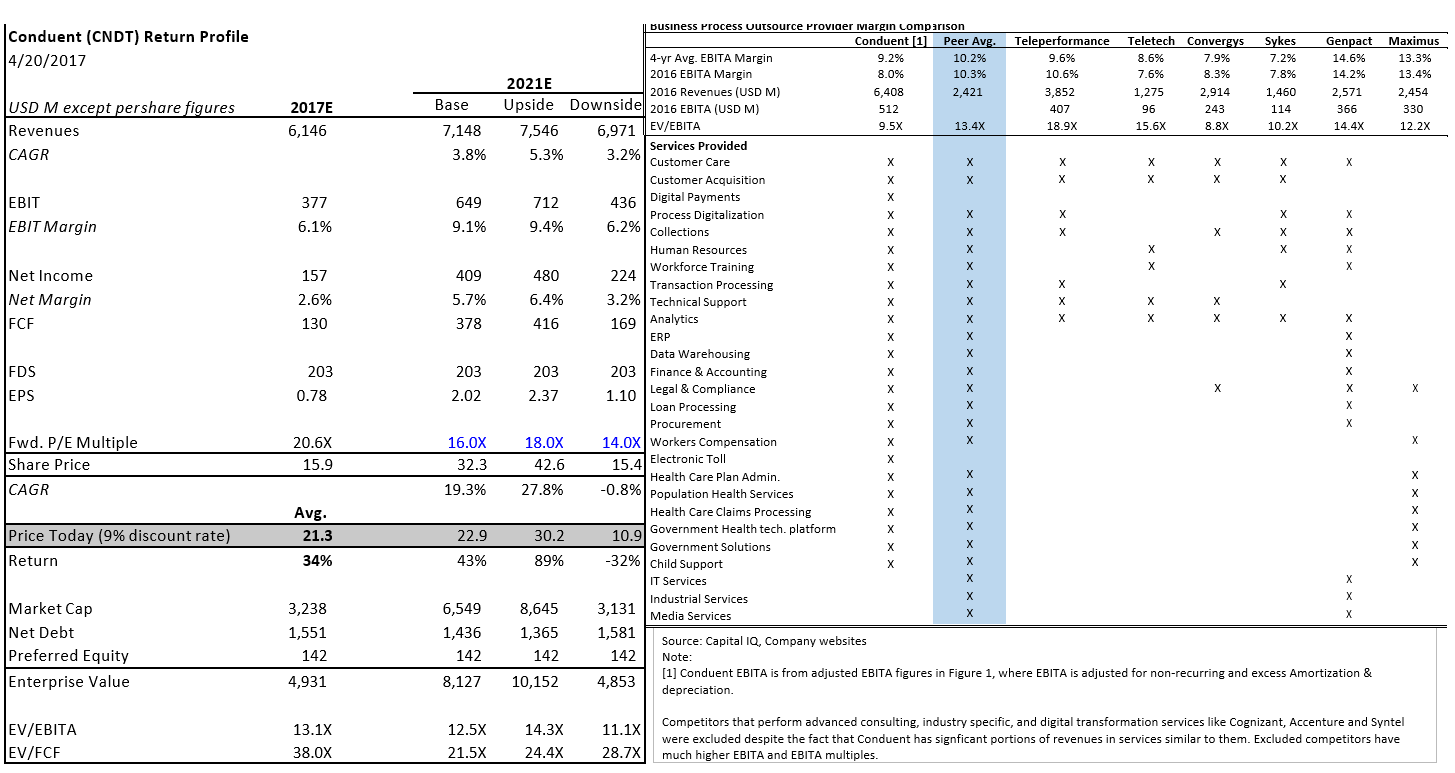

Target Price and Rationale

$21.3 today from discounting a weighted scenario average exit price of $30.1 in 2020 equivalent to roughly 15X price to forward EPS of $2 I forecast in my base case for 2021.

Relevant Comps

Most comparable businesses for the segments of Conduent's ( CNDT ) businesses are:

- Teleperformance ( TLPFY ): 17.5X FWD P/E, 18.9X EV/EBITA

- TeleTech ( TTEC ): 18.4X FWD P/E, 15.6X EV/EBITA

- Convergys ( CVG ): 11.9X FWD P/E, 8.8X EV/EBITA

- Sykes ( SYKE ): 14.4X FWD P/E, 10.2X EV/EBITA

- Genpact (G): 15.5X FWD P/E, 14.4X EV/EBITA

- Maximus (MMS): 19.3X FWD P/E, 12.2X EV/EBITA

- Peer Avg: 16.2X PWD P/E, 13.4X EV/EBITA

- Conduent: 21.3X FWD P/E, 9.5X EV/EBITA

Catalyst

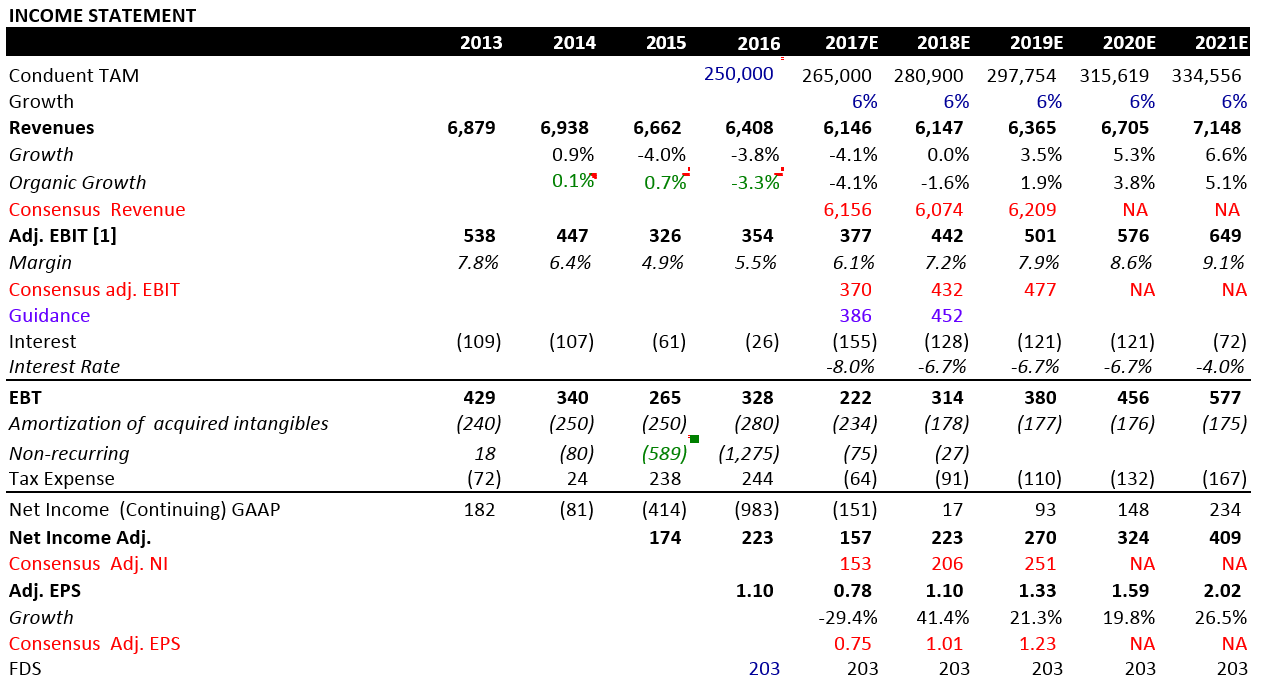

Margin improvement - Renegotiations and rolling off of loss-making contracts signed under prior management returns EBIT margins from 5.9% today back to normal levels of ~8% seen in 2013

Growth reigniting in 2018 - CNDT is expected to shrink revenues this year from rolling off bad contracts. In 2018, CNDT will return to growth because of (1) sales team efforts of increasing spend and clearly defining hunter/farmer roles, and (2) roll-up acquisitions of service lines to cross-sell to existing clients, a strategy that worked particularly well for Healthcare/Government service peer Maximus.

Debt refinancing - CNDT established financing for the spin-off last second, leading to paying rates significantly above the market yield to maturity pricing of the bonds. A refinancing in late 2017 (as allowed by the covenant) could reduce interest expense rate from 8% to 6.7%.

Summary

Conduent is the Business Process Outsourcing ((BPO)) arm of Xerox (XRX) spun off in January 2017. Ashok Vemuri, a BPO industry veteran with >20 years' industry experience, and has previously successfully turned around iGate (IGTE), an IT/BPO company, has taken over from Xerox. I estimate the intrinsic value per share today is $21.3 (see return profile pg. 4) . Conduent is under-appreciated for three primary reasons:

Just renegotiating and running off loss-making contracts signed under prior management would allow leadership to hit 2018 EBIT growth guidance. Despite this, Consensus has Conduent underperforming 2018 EBIT guidance by $20M.

Conduent's business mix including niche leaders and a broad service portfolio should have normalized margin > average ; however, because of current below avg. margins, sell-side analysts are applying a discount in multiple to peers.

Use of proven playbooks previously effective for similar peers.

Business Description

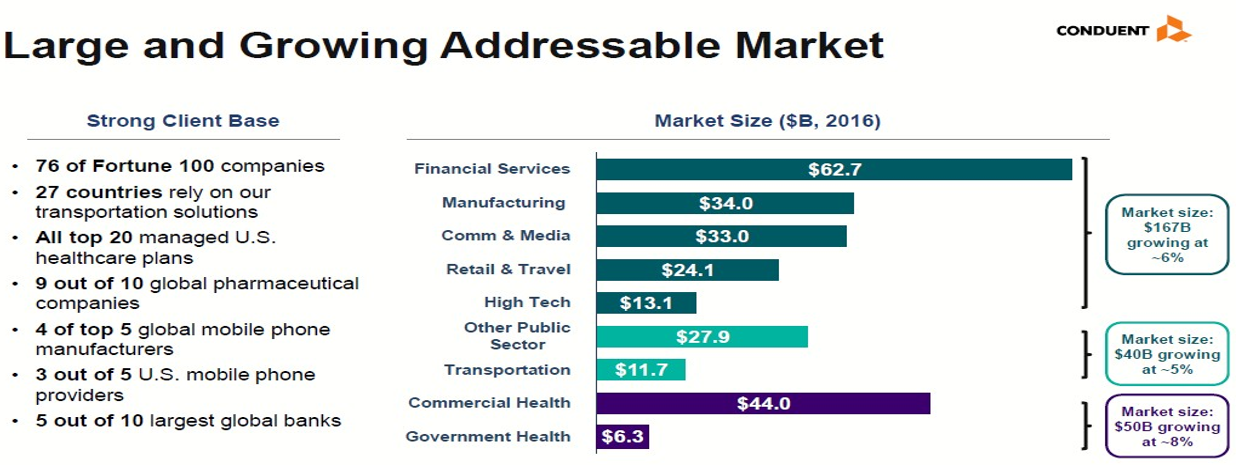

Conduent provides outsourcing services to its client base, taking over the non-core recurring business activities that clients are at a competitive disadvantage to the BPO provider in either HR scale, process knowledge, technology platform, or experience curve. Activities in Conduent's portfolio range from commoditized (i.e. customer care, workforce training) to highly niche and profitable (i.e. electronic toll, health claims processing, government healthcare eligibility). Conduent client base includes 76 of the Fortune 100, all 50 US states, and 500 government entities globally.

Thesis

Thesis 1: Running off and renegotiating loss-making contracts should safely allow management to hit 2018 EBITDA target of ~$130M cumulative improvement over 2016 despite Consensus doubts. Loss-making contracts signed under prior management with no BPO industry experience is currently costing Conduent $134M annually (-38% of 2016 adj. EBIT). Planned cost cutting of $700M ($170M earmarked to be given to customers) can discretionarily be reinvested or delivered to EBIT.

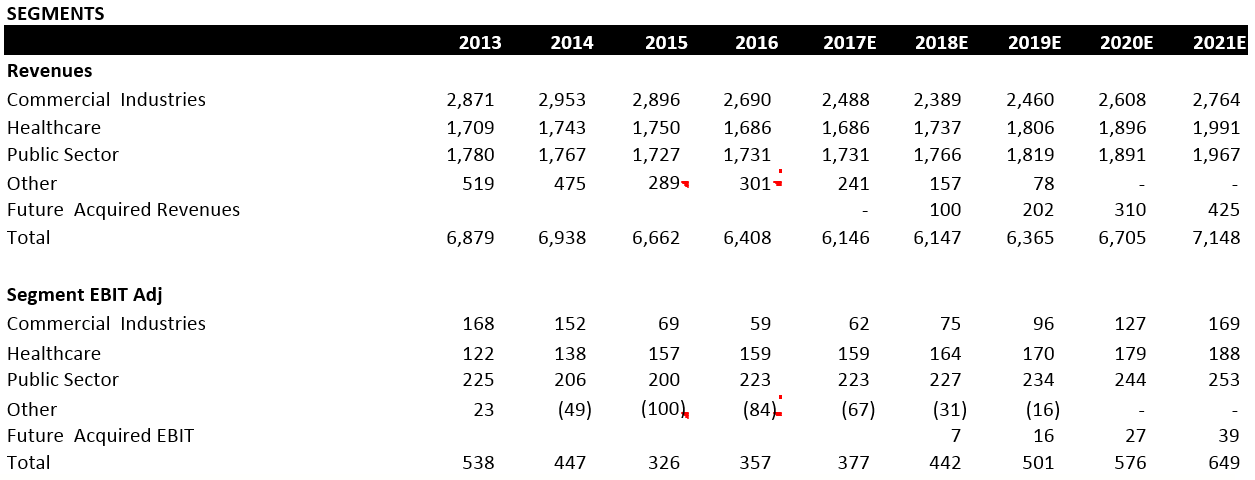

Loss-making contracts appear in two of the business segments of Conduent: Commercial and Other.

Commercial losses (-$49M) - Only 33% of this segment (Customer Care) is loss-making, bringing down the balance, which is operating at 6% margin. New management through renegotiation, cost cutting, reinvestment and operational improvement aims to bring the -5.4% margin for customer care to pure-play customer peers' average margin of 7.5%.

Other Losses (-$84M) - The bulk comes from three ambitious failed updates of 30-yr old Medicaid reporting software platforms that Xerox signed with Montana, California and New York. A small amount is student loan processing contracts Conduent is in the process of running off. New CEO Ashok showed willingness to shrink revenues to grow profit when he aborted the software update of the NY contract post-spin, a contract signed in 2015 for ~560M in revenues. In 2016 the NY contract had $60M of revenue, but $90M of costs. Giving up on the software updates and returning to simply processing the claims through legacy software should allow breakeven over the course of 3-4 years.

Cost cutting ( 530M incremental, 700M total ) - Beyond contract remediation, consists of IT infrastructure savings, workforce reduction, vendor budget rationalization primarily budgeted towards organic investments to reignite sales growth - but should be discretionary to management to give back to EBIT.

Thesis 2: Conduent is trading significantly below peers despite having an above-average mix of business in terms of niche leadership and breadth of service portfolio. Morgan Stanley has explicitly given Conduent a one-turn EBITDA multiple discount in valuation to peers because of lower margins. As can be seen in the table below, Conduent's four-yr aggregate EBITA margin of 9.2% is not significantly below peers, and in fact 2013 EBITA margins was 11.1% while today it is 8.0%. Therefore, as margins improve over time and return towards normalized levels, sell-side will readjust its valuations.

Conduent has both leadership in niches and has a broad service portfolio. Both comparable niche market leaders and broad service providers have high ROICs + sales growth. One particularly good comp for Conduent's Public Sector segment (27% revenues, 13% EBIT Mgn.) and Healthcare segment (26% of revenues, 9% EBIT Mgn.) combined is Maximus, which offers the same services as Conduent in health claims processing and idiosyncratic government processes (i.e. welfare program administration). Meanwhile, Genpact is a good example of an outsourcing/consulting provider with a large range of services provided to many clients.

Thesis 3: Strategic and capital allocation plan of new management team is credible and can bring Conduent growth back in line with industry growth. A particularly successful acquisition strategy over the past four years executed by Maximus was to acquire niche services to cross-sell to existing government and healthcare clients. IR indicates Conduent plans on mimicking this with ~$200M of bolt-on service line acquisitions a year starting 2018. From cross-selling, Maximus organic CAGR was >15% in four yrs. Conduent has an impressive client base (see pg. 4, bottom slide), and this strategy is highly appropriate.

Another playbook that Ashok plans to execute on from his commentary is in focusing sales efforts on recurring-type contracts in verticals and geographies that Conduent has scale and proprietary capabilities. This is the same strategy that Genpact executed after spinning off from General Electric (GE), moving from 23 verticals to 9. This strategy ultimately leads to mid-teens EBITA margins and high-single-digit sales growth.

Risks

Border adjustment tax, H1B Visa rule changes - This risk is partially an opportunity for Conduent, which sponsors no change-of-location work permits and has 50% of workforce onshore vs. a set of competitors that have >70% workforce in India and focuses on labor cost arbitrage. Potential share gain opportunity.

Management is overaggressive in cost cutting, renegotiating - Looking at trends on Glassdoor, morale seems to have been affected by the workforce cuts. However, there are plans to increase the sales force from the current 300 people. Right-sizing will probably not mean indiscriminate cuts. Ashok from presentations appears to be a good communicator, and has BPO experience to handle renegotiations.

Contingent liabilities - CA and MT Medicaid software update contracts settled for ~$150M total cash under Xerox pre-spin. The New York exit could potentially lead to liabilities up to ~$300M (4% hit on upside) given the relative size to other two contracts. Underfunded pensions represent $34M.

(Editors' Note: This is a republication of an entry in theSohn Investment Idea Contest. All figures are current as of the entry's submission - the contest deadline was April 26, 2017).

See also Macy's: Your Platform Is Burning on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}