Lockheed Martin Corp.’s LMT steady inflow of orders for its diverse defense products is likely to boost its revenues. The company holds a strong solvency position as well as a solid presence in the international defense market.

However, this Zacks Rank #3 (Hold) company faces risks like the shortage of skilled labor and sanctions imposed by China, which act as a headwind.

Tailwinds Favoring LMT

In the second quarter of 2024, Lockheed kept up with its tradition of securing several significant contracts from the Pentagon and other American allies. One of these contracts, worth $4.1 billion, requires Lockheed to design new capabilities for its command and control, battle management and communications system. Such contracts culminate into a solid backlog count, which boosts LMT’s revenue generation prospects.

Lockheed Martin's products not only have an impressive domestic market presence but also gain international recognition. International customers of the company have shown a great deal of interest in its THAAD system and PAC-3 missiles, with 15 countries having selected the PAC-3 Missile Segment Enhancement and PAC-3 Cost Reduction Initiative to improve their missile defense capabilities.

At the end of the second quarter of 2024, Lockheed had $2.52 billion in cash and cash equivalents. As of June 30, 2024, its current debt came in at $0.14 billion and was much less than its cash reserve. Thus, it is reasonable to say that the stock boasts a solid solvency position in the near term.

Headwinds Faced by LMT

Industry participants like Lockheed continue to be at risk from the labor crisis, particularly with regard to skilled workers. These labor shortages may make it difficult for manufacturing companies like Lockheed to deliver finished products on schedule, which might affect its operating performance going forward.

In 2023, the China Ministry of Commerce declared that Lockheed had been placed on its list of "unreliable entities" in relation to certain foreign military sales made by the U.S. government to Taiwan involving LMT’s products and services. In this regard, China declared that it would impose certain sanctions against Lockheed. If China imposes further sanctions on LMT, the company's business may suffer.

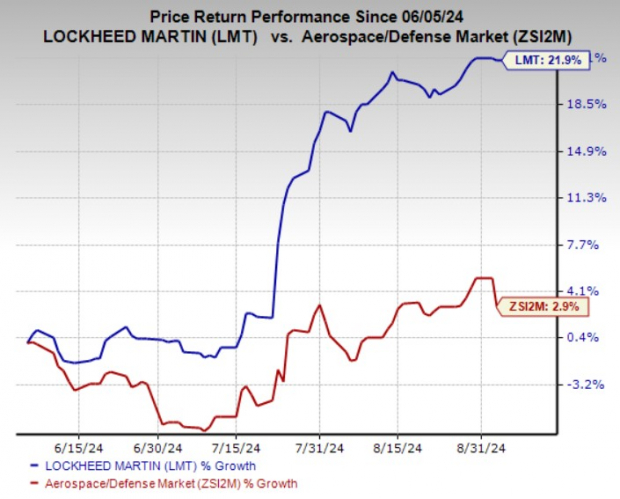

LMT Stock Price Movement

In the past three months, shares of LMT have risen 21.9% compared with the industry’s growth of 2.9%.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks from the same sector are Leidos Holdings, Inc. LDOS, Curtiss-Wright Corp. CW and Leonardo DRS, Inc. DRS, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Leidos’ long-term (three to five years) earnings growth rate is 12.5%. The Zacks Consensus Estimate for LDOS’ 2024 sales suggests an improvement of 5.4% from the prior-year reported figure.

Curtiss-Wright delivered an average earnings surprise of 11.52% in the last four quarters. The Zacks Consensus Estimate for its 2024 revenues suggests a rise of 7% from the 2023 reported sales figure.

Leonardo DRS’ long-term earnings growth rate is 16.4%. The Zacks Consensus Estimate for DRS’ total revenues for 2024 indicates year-over-year growth of 11.4%.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Lockheed Martin Corporation (LMT) : Free Stock Analysis Report

Curtiss-Wright Corporation (CW) : Free Stock Analysis Report

Leidos Holdings, Inc. (LDOS) : Free Stock Analysis Report

Leonardo DRS, Inc. (DRS) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.