Lit Markets Provide Price Improvement Too

In the past we’ve talked about how liquidity providers very efficiently adjust their routing to account for queue length, wide spreads and even opportunity costs. Each time, liquidity-providing traders weigh the random effects of opportunity costs (markouts, missed fills and wait times) against the more certain effects of spread costs and exchange charges.

Today, we look at this from the opposite perspective: How liquidity takers also efficiently route for optimal price improvement across venues, even when they can’t see hidden orders.

In doing this, we build upon data that already exists that shows that the broker conflict related to routing passive orders to maker-taker exchanges, and even the need to collect data on access fees in a pilot, is well and truly overstated.

Our data also suggests that there are many occasions where investors trading off-exchange are missing better prices. NBBO fills in the dark add to over 9% of all trades, and miss as much as $136 million a year in price improvement available on Nasdaq alone.

The hidden advantage of trading on maker-taker

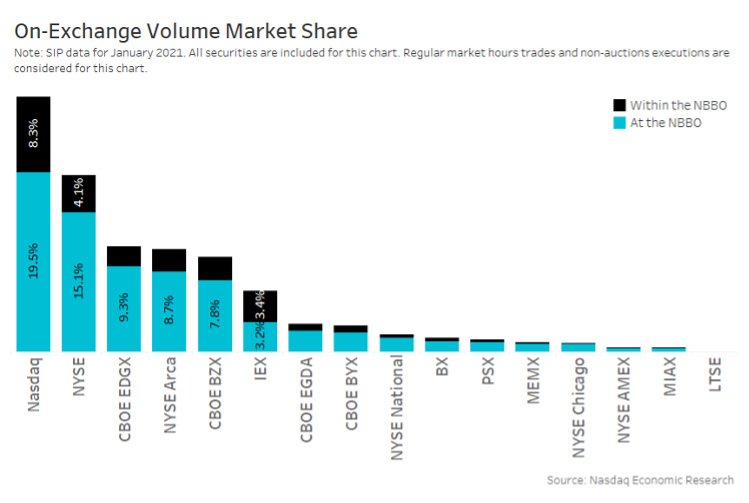

We’ve already talked about how liquidity takers receive price and size improvement on Nasdaq. The reason is that there is a significant proportion of hidden orders at the NBBO-or-better that takers will trade with as they cross the spread. In fact, as Chart 1 shows, Nasdaq not only has the largest pool of lit liquidity in U.S. markets, it also has the largest amount of non-displayed liquidity.

We calculate that roughly 30% of Nasdaq volume is executed within the NBBO.

In contrast, most trades on inverted venues happen at the NBBO. But more on that later.

Chart 1: Non-displayed liquidity makes up 26% of all on-exchange trading volume

This also highlights the benefits of rebates for liquidity providers and a more centralized pool of liquidity.

- Firstly, rebates encourage competitive lit quotes, which is important to compete with the customer tiering in off-exchange markets.

- That makes it more likely that takers will route orders to the NBBO on Nasdaq.

- That, in turn, means hidden orders inside the Nasdaq quote wait less time, on average, for a fill, reducing their opportunity costs.

- This simultaneously results in price improvement for the takers.

It’s a win-win situation that fragmented or intermediated markets can’t do nearly as well.

The benefits are bigger for higher-priced stocks

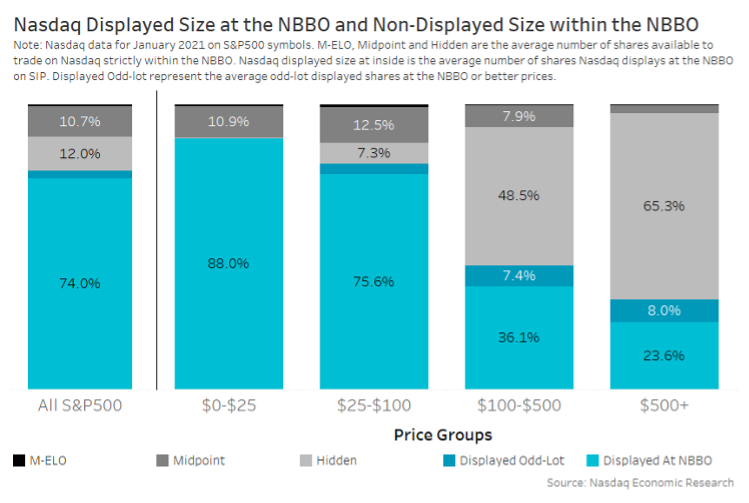

However, this effect is not equal for all securities. As we see in Chart 2:

- Midpoint orders are much more likely on low-priced stocks (dark grey).

- Hidden limit orders (light grey) and odd lots inside the quote (dark blue) are more likely for high-priced stocks.

- Very high-priced stocks, where posting 100 shares to the bid signals a large trade, see less than 25% of the liquidity being advertised (light blue).

Chart 2: Routers place orders very differently for higher-priced stocks

This lack of price transparency in high-priced stocks is a key reason why the SEC proposed smaller odd lots in its new NMS II rules. However, given the data shows most of the quotes are hidden (not odd lots), the benefits of the rule change could be much smaller than expected.

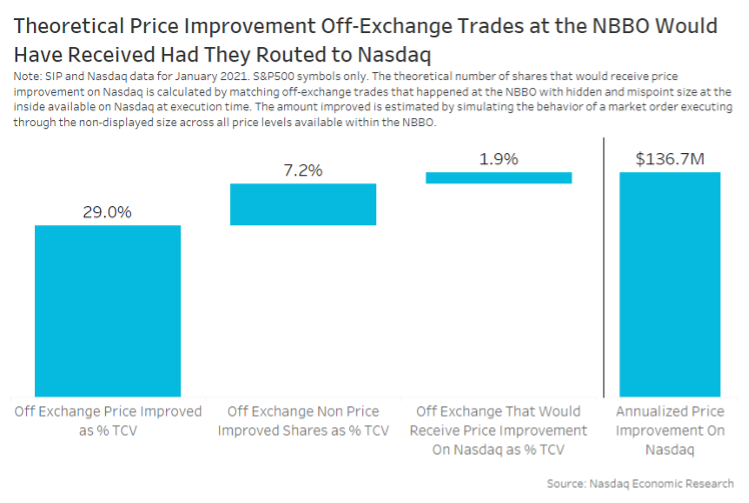

Off-exchange investors may be missing $136 million in price improvement

Those hidden orders on-exchange add up to a significant amount of price improvement. But because the orders are not advertised, it’s hard for someone who stays off-exchange to measure, just like other opportunity costs.

However, as we know what orders are resting hidden during the day, we can quantify the missed price improvement on orders that cross the spread on reported off-exchange trades.

According to our calculations (Chart 3), in January 2021, off-exchange orders totaled over 38% of all shares traded in S&P 500 names. Almost a quarter of those shares traded off-exchange were also executed at the NBBO, adding to over 9% of all volume.

Not all those off-exchange trades would have been price improved on exchange. But we estimate that one of every five shares, representing 1.9% of the total consolidated volume, would have been price improved on Nasdaq alone.

The total price improvement those orders missed added to $136 million per year.

A similar academic study just looked at odd-lots being traded through by far-touch ATS fills and estimated market wide costs of those trade-throughs at around $27 million per year.

Chart 3: Nasdaq can potentially provide price improvement on one in five far-touch shares, adding to $137 million each year

Some active traders, however, do cross spreads on-exchange pretty frequently. And although these orders are hidden, they are able to extrapolate the economics of taking on each venue based on average experiences. For the stocks above, this average amount of price improvement added to 0.7 basis points (bps). That includes both shares that do and shares that don’t price improve on liquidity-taking sweeps.

Although that sounds small, it represents a saving of $0.007 on a $100 stock, which more than makes up for Nasdaq’s taker fee. That is very important to the old access fee pilot debate.

Price improvement busts another myth of the access fee pilot

The access fee pilot was predicated on a belief that brokers were harming buy-side investors by routing passive orders to maker-taker exchanges in order to earn revenues they (the brokers) could keep, even though buy-side investors had higher opportunity costs and shortfall from being placed lower in the queue resulting in missed fills. This is described as a classic conflict of interest.

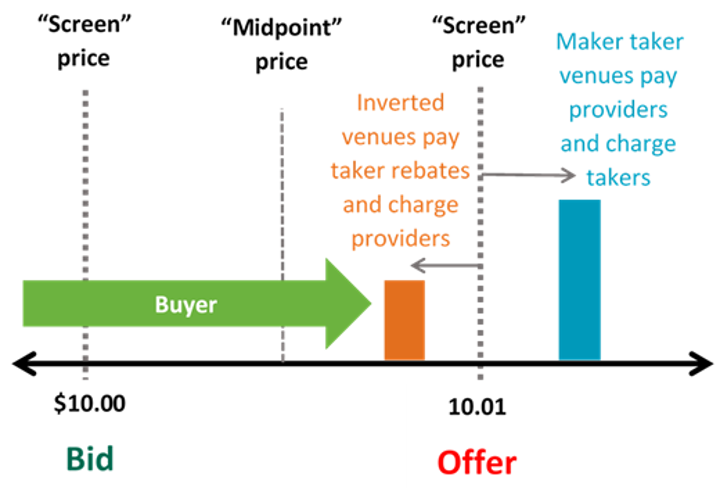

At a high level, the theory makes sense. Inverted venues offer a rebate to takers, making them much cheaper to take from (Chart 4).

Chart 4: Inverted venues pay rebates to takers, giving them cheaper expected “all-in” costs for the buyer, which should make them the first venue traded (and top of the queue)

For a buyer, the all-in costs of trading with an inverted venue (which pays a rebate to the taker) are actually less than the price you see on the screen. Whereas for a maker-taker venue, the all-in cost is more.

That, in theory, should make inverted venues the first choice for a spread crossing order, resulting in better queue priority for passive investors resting in inverted venues.

That, in turn, gives inverted passive orders queue priority. Over time, passive orders in inverted venues should capture more spread. In contrast, orders deeper in the queue (or still resting in maker-taker venues) might need to chase stocks when the prices move away from an unfilled order still resting in the market.

Takers do not always prefer inverted

Although that all makes theoretical sense, data shows that traders rarely use inverted venues (even the majority of traders who don’t have broker conflicts).

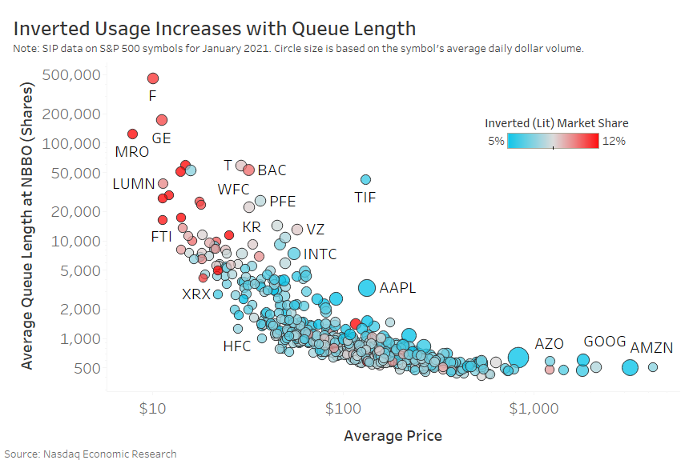

In fact, we find that inverted venues are mostly used for very low-priced stocks where spreads are wide and queues become exceptionally long (Chart 5). What do they know that the theory above doesn’t?

Chart 5: Inverted venues are used much more for low-priced stocks, which also have longer queues

Importantly, research has shown that the market actually prices these opportunity costs very accurately. In essence, the cost of queue priority equals (and offsets) the shortfall improvements.

That means a buy-side investor should be indifferent to where they rest passive orders, provided their commission rate accounts for the difference in routing costs.

Price improvement on the maker-taker turns everything on its head

In our price improvement research (above), we found that price improvement is often larger than the take fees charged by a maker-taker venue.

Given the queue priority of inverted venues is all based on economics (of takers), we wondered if the price improvement we see has an effect on the broker conflict and investor harm that drove the access fee pilot.

The answer is, absolutely: Yes. The implication is that the broker conflict that drove the access fee pilot is actually much smaller than many assumed.

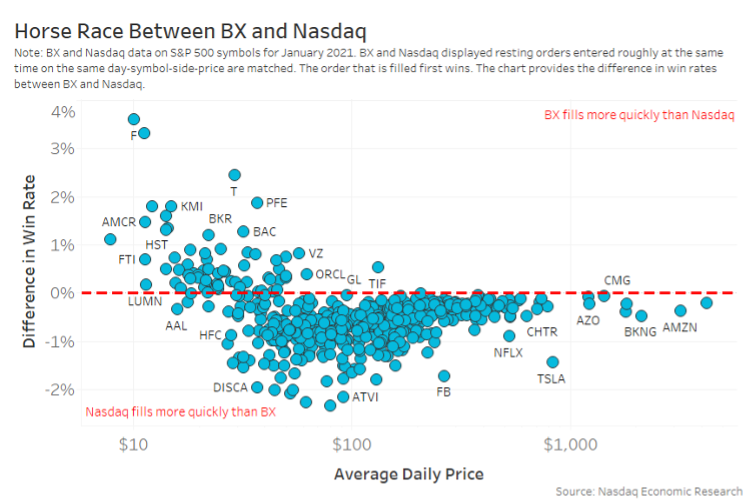

To show that, we basically ran horse races similar to what Battalio, Corwin and Jennings did back in 2013. We find Nasdaq (maker-taker) and BX (inverted) displayed orders that are entered on the same side, price and symbol and are live at the same time. We then calculate which venue fills first.

According to the broker conflict theory, investors are harmed by resting in maker-taker venues because they fill last.

In our results, we find the opposite, especially for many higher-priced stocks.

Chart 6: Resting orders on maker-taker fill faster for all but lower-priced names

Despite the extra take fees and deeper queues on Nasdaq, we found that for high price stocks, near-touch orders filled faster than on an inverted venue.

Now we know that routing economics include more than take fees and opportunity costs. They also need to include the average expected price improvement from hidden orders on all take trades.

Clearly, smart traders knew that already, as seen in the low inverted market share in Chart 5.

What does this all mean?

This data adds important new information to address a few different market structure debates:

- Concerns about access fees and the level of harm brokers cause the buy side is likely overblown (regardless of how they route).

- Trading at the far touch off-exchange likely misses price improvement available on exchanges, which in turn raises a question about whether copying the NBBO in the dark is actually “best ex.”

- Smart traders include all costs of trading in their routing decisions, including costs that are not explicit at the time of the route.

- We can see in the market today how maker-taker fees affect behavior. When incentives to reward liquidity fall (in bps) in higher-priced stocks, quote quality falls, hidden orders increase and spreads widen. Conversely, when spreads are too wide, access fees likely add to lit queues and exacerbate fragmentation to jump those queues. There is an argument for intelligent ticks tied with intelligent rebates.

- Our data also shows that the NMS II odd-lot plan may be less impactful than previously believed because hidden orders outweigh odd lots in high-priced stocks.

The data is out there. Regulators just need to use it.

Eugenio Piazza, Research Specialist for Economic and Statistical Research at Nasdaq, contributed to this article.

Other Topics

Stocks

Phil Mackintosh

Nasdaq

Phil Mackintosh is Chief Economist and a Senior Vice President at Nasdaq. His team is responsible for a variety of projects and initiatives in the U.S. and Europe to improve market structure, encourage capital formation and enhance trading efficiency.

Read Phil's Bio