This article is part of the LatAm Tech Weekly Series, written by Julia De Luca and powered by Nasdaq. Through Nasdaq’s global network, we partner with Latin American companies to support their entire business lifecycle to elevate their brand and access the global markets. Learn more about Latin American Listings here.

People in Brazil usually say that the year only really starts after carnival. Well, despite the fact that my year has started long ago - happy new year to the ones that follow the tradition! It is true, however, that the tech events all start happening after carnival. On that note: I will be a speaker at the Identity Day, organized by anti-fraud startup Caf. Featuring top-notch companies (Vivo, Globo, Itaú, Google, Mastercard) and selected professionals, this full-day event promises in-depth discussions about the evolution of identity, data and the balance between user experience and fraud prevention. It's going to be an in-person event at the Amcham Business Center in São Paulo, on March 16th, and free! Want to sign up? Click here and I’ll see you there!

Thanks for reading Weekly Tech Update - Julia! Subscribe for free to receive new posts and support my work.

Follow me on LinkedIn , Instagram or Twitter for daily updates!

Opinions expressed here are solely my own and does not represent those of people, institutions, organizations that I may or may not be associated with in any capacity, unless explicitly stated.

On to the usual market update: the IPO market remains slow, and the “million dollar question” is when will the comeback to its pre-2022 days happen. The answer, of course, depends on who you ask. But, Pitchbook wrote an interesting piece this weekend on the theme that is worth sharing with you.

First, let’s cover what are the factors needed for a comeback: a) stabilized macroeconomic environment (more clarity on the direction of interest rates); b) greater alignment on pricing between buyers and sellers; c) a company that leads the pack back onto the public exchanges.

As always, I am an optimist and certain factors have already indicated that it will occur sooner rather than later. In 2023, activity has picked up a bit with nine US PE- and VC-backed IPOs so far, up from Q4 2022's five IPOs.

As the article puts well, "no one has a crystal ball" but we do have economists and historical data that generates a well-documented speculative discussion. Looking at history, in the early 2000s, markets took around 2 years to recover from the dot-com crash , with a pick up in IPO activity starting in H1 2001 and recovery following in the second half of 2003. During the global financial crisis, the IPO slowdown lasted around 18 months. In 2009, however, government interference with fiscal and monetary policies helped rebuild the public markets, and the US IPO market came back to life by the second half of the year. Looking most recently to the COVID-19 pandemic - retrenchment period lasted only six months and its recovery took only three, and was then followed by the most active IPO market in the past two decades. So, where do we land now? Some industry leaders anticipate the recovery period will begin in the second half of 2023. And I hope we are all right.

Looking at what has already happened in the local tech industry last month, Itau BBA released a report together with Sling Hub on the Latin American tech activity. In line with what I said earlier, despite all macro headwinds, we are seeing a hesitant but hopeful start to 2023. Global equity markets actually kicked off January strong after a hard 2022, with the S&P up 6% and the tech-heavy NASDAQ surging 10% as Central Banks and markets expect a soft landing. For the time being, data this past month showed that it is taking longer to raise a venture round now than at any point since 2017. Average time from Seed to Series A now stands at 798 days (2.2 years). From A to B, now the median is 2 years – almost one year longer than what was seen 9 months ago. From B to C, founders are taking at least 18 months. Looking forward, we still envision more M&A activity as clear winners look to consolidate their respective markets, and with the IPO window still shut, a merger could be a exit alternative for companies. Want to sign up? please include your e-mail address here.

To wrap up, momentum for private debt funds is building. According to Pitchbook data, private debt is taking on greater importance as banks around the globe are tightening lending conditions and more companies are seeking liquidity amid increased economic uncertainties. Despite challenging market conditions, capital raised by private debt funds topped USD 200 billion in 2022 for the third consecutive year in which capital raised for this asset class topped the USD 200 billion mark, with fund managers amassing USD 200.4 billion across 159 vehicles. Recently, two fund managers—Crescent Capital Group and Willow Tree Credit Partners—have lined up a combined $10 billion in commitments to their flagship private debt vehicles, underscoring investors' growing appetite for private market loans.

Monday

-

Mexican startups Minu and Plerk merge to strengthen the benefits market.

Both startups work in the flexible benefits market and are now merging to strengthen their platform focused on financial health. Combined the new company now has 500 clients – among them, Grupo Modelo, Rappi, Coppel and others.

-

Belvo announced a new account-to-account payments product that relies on their open finance infrastructure to help companies in Colombia accept Pagos Seguros en Línea (PSE) with a simplified UX (only 4 steps vs. 10 with the current flow). Already more than 20K companies in the country accept this account-to-account (A2A) payment method – which is overtaking credit cards for online purchases.

-

Chilean startup Datamart, that offers a platform that expedites the processes of evaluation and obtaining credits, based on a technology of exchange of private data between the holders of information and financial institutions, raised a USD6.3mm seed round. Banco Santander, Bice Inversiones, Falabella, and Moonvalley Capital participated in the round.

Tuesday

-

Itau Clients are already able to use their new product Pix in installments, mentioned in last week’s newsletter. The amount can be split in up to 72 installments. If you want to understand how it works, watch this video (PT only).

-

Chile-based Buk, a human resources software specialist, raised a USD 35 million Series B led by Base10 Partners and Greenoaks.

-

Nubank, through Instituto Nu, its social impact initiative, announced seven thousand openings for a technology education program.

Wednesday

-

Brazilian Stark Bank announced that it will grant BRL 300mm in credit to selected corporate clients. The capital will come from their Series B of USD 45mm that occurred in April 2022.

-

In less than one year, Brazilian fintech ICred has already granted BRL 400mm in payroll loans. The company anticipates a gross revenue of BRL100mm in 2023.

-

Evertec, a Latin American electronic payment processing and technology company based in Porto Rico and listed at the NYSE announced the acquisition of paySmart, a Brazilian fintech that allows other companies to offer financial products. Evertec is currently present in 26 Latin American companies and the acquisition is focused on increasing penetration in Brazil.

Thursday

-

Avenue Securities, online brokerage firm intended to provide easy access for international retail investors interested in securities traded on U.S. exchanges, talked about the strength of its B2B strategy. The company has currently more than 5k registered investment advisors plugged to their platform, in around 350 offices. Itau Unibanco bought a 35% stake in the company in the middle of last year. Before the deal, Avenue was raising around BRL 600mm per month in AUM – currently the figure is at around BRL 1.5bn.

-

Tijana Jankovic, Rappi’s Brazil CEO, affirmed in an interview that the RappiPrime feature is one of the most important growth levers in the country. It has helped increase the customer base in the app by +20%. According to her, going against market rumors, Rappi never intended to shutdown its Brazil operations. The company cut costs and pursued local adjustments. The goal is to focus on engagement in 2023 – both on the consumer side and the business side.

-

Dattos, Brazilian startup that offers a platform for accounting reconciliation and fiscal conciliation, announced a USD3.9mm Series A round with Igah Ventures.

-

MercadoLibre posts record profits, but company remains cautious of expanding credit offering. Operating margin in Q4 was 11.6%, above the 6.8% expected by analysts, while revenues topped $3 billion, in line with projections.

-

ContaFuturo, Brazilian startup that offers financial solutions that focus on expense management, raised a USD3.9mm seed round with Empirica.

Friday

- Bradesco, Brazilian bank, announced that they will focus in 4 areas when investing in startups through their corporate venture capital: regulation, emerging tech, client experience and changes in the traditional banking model. In 2022, the bank invested in 14 companies – such as Teddy, Ololu, LegalBot and Semantix. CVC in defenetly a trend in Brazil – research shows that only las year, close to BRL 2bn was announced as resources to be invested by such vehicles – and that there are more than 100 corporates engaging in the strategy. Innovabra announced this week its third investment in 4intelligence, artificial intelligence platform. To date the fund has injected BRL 24mm in the company.

What did I learn from readers?

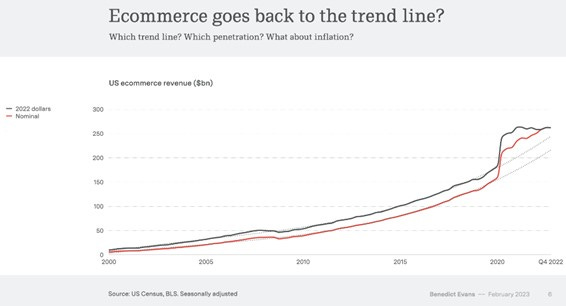

I received from a reader the link for Ben Evans’ presentation 2023 as a must see. It is indeed, very good. The title is The New Gatekeepers – and it covers several interesting topics. It is a must read! Below you will find a TL;DR version with a couple of bullet points and graphs.

- The end of “free money” greatly impacts the tech market. Macro matters for the first time in a decade. Most major markets saw several years of future ecommerce growth compressed into the pandemic. Now, ecommerce tends to go back to the trend line:

- In the pandemic, venture capital also surged dramatically – now going back to historical levels.

- While layoffs are indeed occurring, in perspective, tech companies hired at a huge scale in the last decade. The layoffs now seem natural to a certain extent given the hiring spree.

- On one hand, it is true that there was an over-investment period and a loss of discipline in the last 24 months. This, coupled with an uncertain macro-economic outlook, brings uncertainty. However, it is also true that 5bn people have a smartphone – and that every market and value chain in being remade around the internet.

With that – who are the “New Gatekeepers”?

- Department stores dominated retail for a century, now, they have almost disappeared. The same happened to newspapers.

- Now, on a GMV basis, Amazon has overtaken Walmart’s revenue and software is eating advertising – on a digital pure-play.

Founders: How do you reach your customers?

- Rent, advertising and pricing we all separate budgets. They now merge into one.

- Retail media gained around 10% of share within the US advertising spending.

- Amazon ads represented 7.5% of 2022 retail revenue.

- Chinese manufacturers are bypassing US retailers and brands and going directly to the consumer (Shein, for example, as mentioned last week in the newsletter). They are also building their brands on Amazon (such as Anker, USD2bn phone accessory business on the Amazon marketplace).

- Shopify powered USD 200bn of sales in 2022, which represents 45% of the Amazon marketplace.

- New channels + new tech = new SKUs

Bundling & Unbundling

The future:

- Metaverse is no longer “a thing” – now it’s all about AI.

Conclusion: Putting things into perspective -

What am I reading?

-

Inteligencia Financeira – I just became a columnist on this portal that aims to provide educational finance content. In my debut, I wrote about Open Finance in Brazil, as it completes its second year anniversary.

-

CB Insights: Emerging Tech Research report on gaming

What am I listening to? What am I watching?

Quote of the week:

“The older I get- just take the time, be kind, be available - it pays off...” -Bill Gurley

Originally published on my Substack.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

IPOs Technology

Julia De Luca

Julia De Luca is part of the investment banking team focused on tech coverage at Itau BBA. With more than 10 years of experience in finance, her focus is to connect global players to the Latin American tech ecosystem – with content, intel and opportunities. Julia co-authored the book Brazil Fintech and constantly writes columns on the topics of open banking, venture capital investment, regulation and LatAm tech trends. Julia started her career as Global Investor Relations at Gávea Investimentos and also spent a couple of years at Stone Co. She holds a degree in Economics from Pontificia Universidade Católica (PUC-Rio). She is also a columnist at MIT Tech Review, ION and Inteligencia Financeira.

Read Julia's Bio