Credit: Shutterstock photo

Credit: Shutterstock photoBy Morningstar :

By Michael Rawson, CFA

Last October, iShares launched its so-called "core" series of ETFs . iShares, and its parent company, BlackRock( BLK ) , have long been well-regarded by institutional investors and financial advisors. However, the firm has been less successful with individual investors, as evidenced by years of market share losses to Vanguard. The launch of the iShares "core" series is part of a broader push by BlackRock and iShares to boost brand recognition among individual investors. But what's the result? Is this just a marketing gimmick, or has iShares created a truly useful set of "core" portfolio building blocks?

What Constitutes a Solid 'Core'?

Most investors' portfolios tend to follow either a strategic or tactical asset-allocation approach, or some combination of the two. The strategic approach is rooted in the efficient markets hypothesis, which suggests that investors weight all assets by their market capitalization and attempt to achieve optimal diversification. Investors' strategic asset allocations will differ on the basis of risk tolerance and income needs. On the other hand, tactical asset allocation allows for the selective overweighting (or underweighting) of certain asset classes or securities that are expected to outperform (or underperform). A portfolio employing a tactical asset allocation will look different than the market portfolio, and different tactical investors will hold different portfolios depending on their market outlook.

Ideal strategic "core" portfolios give broadly diversified exposure to an entire asset class. Highly correlated securities with similar risk and return characteristics are grouped together to eliminate idiosyncratic risks. Index inclusion rules should be liberal. The idea here is to hold the entire market. Turnover should be very low. For stocks, we want to own the entire market from mega-cap to micro-cap. Good fixed-income and commodity indexes can be harder to find, but our options are better today than ever before. These funds should allow us to "set and forget," meaning that the exposure they provide today will be stable over time. Whereas active portfolio managers may "drift" as they feel conditions warrant, a good "core" index fund, by definition, does not stray from its stated objective. Perhaps most importantly, the costs of a solid "core" portfolio should be extremely low.

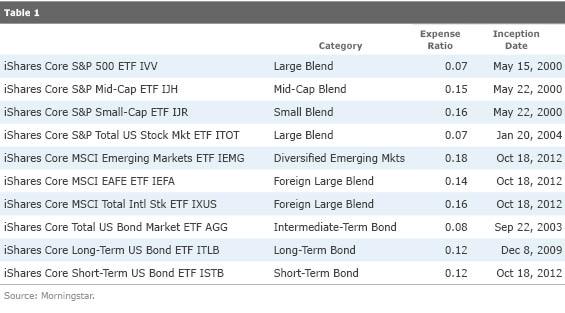

The Core 10

How does iShares' "core" series measure up against the criteria outlined above? It comes pretty close to the ideal. The core series includes 10 ETFs covering three broad asset classes: United States stocks, international stocks, and taxable bonds. The indexes these funds follow are comprehensive, each holding over a thousand securities. While the stock funds exclude micro-caps, this is a very small omission as micro-caps make up only about 2% of the equity market. Meanwhile, the bond funds exclude Treasury Inflation-Protected Securities and high-yield and international bonds. These omissions reflect the construction of the Barclays Aggregate Bond Index, the most commonly used bond benchmark. S&P, MSCI, and Barclays provide the indexes for the core series. Each offers stable exposure to their target asset class and are among the highest-quality indexes available. Finally, all of these funds are extremely low-cost, charging annual expense ratios ranging from 0.07% to 0.18%.

If You Build It...

As the "core" in their names implies, investors can build a fairly comprehensive and well-diversified portfolio using just three of these ETFs. Such a portfolio could be comprised of iShares Core S&P Total US Stock Market ETF( ITOT ) (30% allocation), iShares Core MSCI Total International Stock ETF( IXUS ) (30% allocation), and iShares Core Total US Bond Market ETF( AGG ) (40% allocation). The resulting 60/40 stocks/bonds portfolio would have a weighted average expense ratio of just 0.10%.

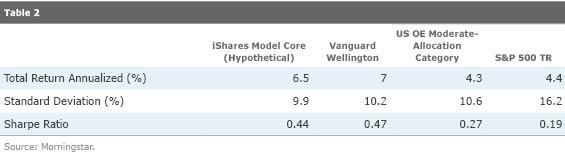

Using historical index data for these funds, this hypothetical portfolio, rebalanced annually, would have returned 6.5% per year over the past 15 years with a Sharpe ratio of 0.44. Using index data ignores the 0.10% expense ratio and costs of rebalancing, but these should be small compared with the total return. The Sharpe ratio is a risk-adjusted return measure that penalizes returns for volatility. The smoother the ride, the more likely you are to stick with your investment plan and ultimately experience returns more reflective of the averages detailed above.

With a 60% allocation to stocks and 40% allocation to bonds, this model portfolio would fall squarely into Morningstar's Moderate Allocation category. Looking at its historical performance, our hypothetical portfolio has fared pretty well when compared with actively managed funds in the category that have a Morningstar Analyst Rating of Gold, such as T. Rowe Price Capital Appreciation( PRWCX ) , Dodge & Cox Balanced( DODBX ) , and Vanguard Wellington( VWELX ) .

Morningstar's Moderate Allocation category has a total of six funds with a Morningstar Analyst Rating of Gold. Over the past 15 years, the average Sharpe ratio for these funds was 0.45. These funds' current average annual expense ratio is 0.61%. Had the ETFs been available historically, we could have mimicked that performance with just three iShares ETFs for a cost of 0.10%. Of course, the return numbers are net of fees, so the core series did no better than the Gold-rated funds despite the cost advantage.

By Asset Class: U.S. Stock

The broad U.S. stock market is represented by ITOT, which follows the S&P 1500 Index. While iShares calls this a total stock market fund, it's really more of a broad market fund as it excludes most micro-caps as well as a handful of other companies on the basis of S&P's strict index inclusion rules pertaining to domicile, required float, and IPOs. Examples of well-known firms currently excluded from the benchmark include General Motors( GM ) , Las Vegas Sands(LVS) , and Facebook(FB) . Despite these differences, the S&P 1500 is highly correlated to and has had long-term returns similar to total market indexes such as the Russell 3000.

Within the iShares core series, the U.S. stock category is further broken along lines of size to include ETFs covering the large-, mid-, and small-cap spectra of the U.S. market. When iShares announced the core series, they cut the expense ratio on iShares Core S&P 500 ETF(IVV) to 0.07% from 0.09%. Investors can rest assured that this fund is going to give returns highly similar to the index. For the 10 years through February 2013, IVV returned 8.17% compared with 8.24% for the S&P 500 Index, nearly spot-on the ideal index return less expenses.

Meanwhile, iShares Core S&P Mid-Cap ETF(IJH) had its expense ratio cut to 0.15% from 0.20%. Its new annual fee undercuts the more heavily traded SPDR S&P MidCap 400(MDY) by 10 basis points.

Finally, small-cap stocks are covered by iShares Core S&P Small-Cap ETF(IJR) , which tracks the S&P SmallCap 600 Index. While S&P's strict index inclusion criteria don't have much impact in a broad stock market index, their impact is more pronounced in the small-cap space, where quality can be more of a concern. The S&P SmallCap 600 Index has trounced the Russell 2000 Index by 82 basis points per year over the past decade. That outperformance is attributable at least in part to holding higher-quality stocks during a difficult economic environment.

International Stock

IXUS is decomposed into a pair of ETFs that track stocks from developed and emerging markets. Unlike the existing and hugely popular iShares MSCI EAFE Index(EFA) and iShares MSCI Emerging Markets Index(EEM) , the new core international ETFs track indexes that include small-cap stocks, making them more comprehensive. While the inclusion of small caps might elevate volatility slightly, if they follow their historical pattern, small-cap stocks could provide higher returns and should be included in a strategic portfolio.

Taxable Bond

For investors that want to more closely monitor and manage their interest-rate risk, the taxable bond asset class is further subdivided into two buckets on the basis of duration. IShares Core Long-Term US Bond ETF(ILTB) and iShares Core Short-Term US Bond ETF ISTB offer more-targeted exposure to different parts of the yield curve. Unlike the indexes that the stock ETFs in the core series follow, these two bond ETFs do not sum up to the broader index tracked by AGG, the Barclays U.S. Aggregate Bond Index. ISTB includes bonds with maturities between one and five years, while ILTB includes bonds with maturities greater than 10 years. In addition, both exclude mortgage-backed securities.

It's Not All Sunshine, Lollipops, and Rainbows

Lower expense ratios are almost always a good thing for investors, so there's a lot to like about iShares' new lineup. However, iShares chose to launch the new iShares Core MSCI Emerging Markets ETF(IEMG) rather than cut the expense ratio on the existing EEM. EEM has $50 billion in assets, so cutting the expense ratio to 0.18% would result in a revenue loss to iShares of $255 million.

Additionally, the core series represents just 10 out of iShares lineup of 280 ETFs. We would have liked to see fee reductions on more ETFs, particularly in iShares international and fixed-income lineup. To iShares' credit, more of the ETFs that they have launched recently come with attractive price tags, even in areas with little direct competition. For example, iShares MSCI EAFE Minimum Volatility(EFAV) charges just 0.20%, while iShares Baa - Ba Rated Corporate Bond(QLTB) charges 0.30%.

It is important to note that cheaper and equally high-quality core funds exist from providers such as Vanguard and Schwab--the same funds whose success, in part, prompted iShares to launch its core series in the first place. Still, the differences in these funds' expense ratios are becoming increasingly small. For example, Schwab U.S. Broad Market ETF(SCHB) has an annual expense ratio of just 0.04% and Vanguard Total Stock Market ETF(VTI) levies an annual fee of 0.06%. Both of these stock portfolios hold more individual stocks than the S&P 1500 Index. For investors, the process of choosing the best core funds will likely come down to individual factors such as which broker you use, especially since some brokerage firms offer commission-free trades for certain ETFs. Transaction costs can quickly add up if you plan to make regular contributions to your investment account or rebalance your portfolio frequently. What is abundantly clear is that fierce competition for the core of the ETF market has left investors with a plethora of very low-cost portfolio building blocks at their disposal.

Disclosure : Morningstar, Inc. licenses its indexes to institutions for a variety of reasons, including the creation of investment products and the benchmarking of existing products. When licensing indexes for the creation or benchmarking of investment products, Morningstar receives fees that are mainly based on fund assets under management. As of Sept. 30, 2012, AlphaPro Management, BlackRock Asset Management, First Asset, First Trust, Invesco, Merrill Lynch, Northern Trust, Nuveen, and Van Eck license one or more Morningstar indexes for this purpose. These investment products are not sponsored, issued, marketed, or sold by Morningstar. Morningstar does not make any representation regarding the advisability of investing in any investment product based on or benchmarked against a Morningstar index.

See also Turquoise Hill Will Rise Again on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}