A mostly graphical daily curated roundup of the markets and the economy from Nasdaq's IR team.

#marketseverywhere | several weeks of losses now w/ equities: ACHTUNG! rising yields making investors nervous | Q2 + early Q3 rally was due to multiple expansion while earnings recession | valuations getting rich / short-term oversold territory | weakness out of China | Jackson Hole central banker symposium in focus this week

* source: Piper Sandler

* source: Grindstone Intelligence

* source: CNBC

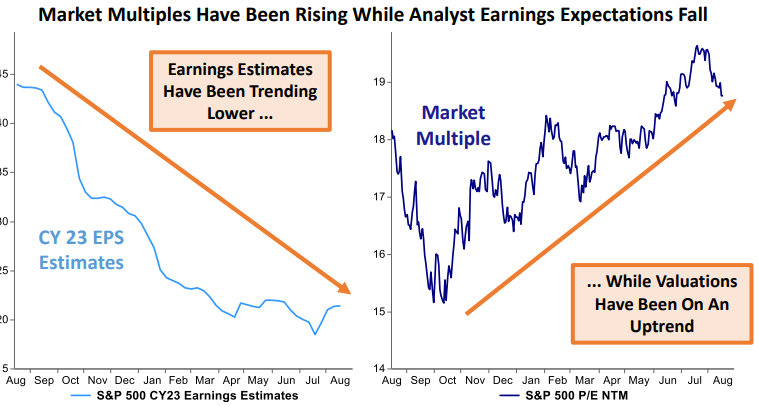

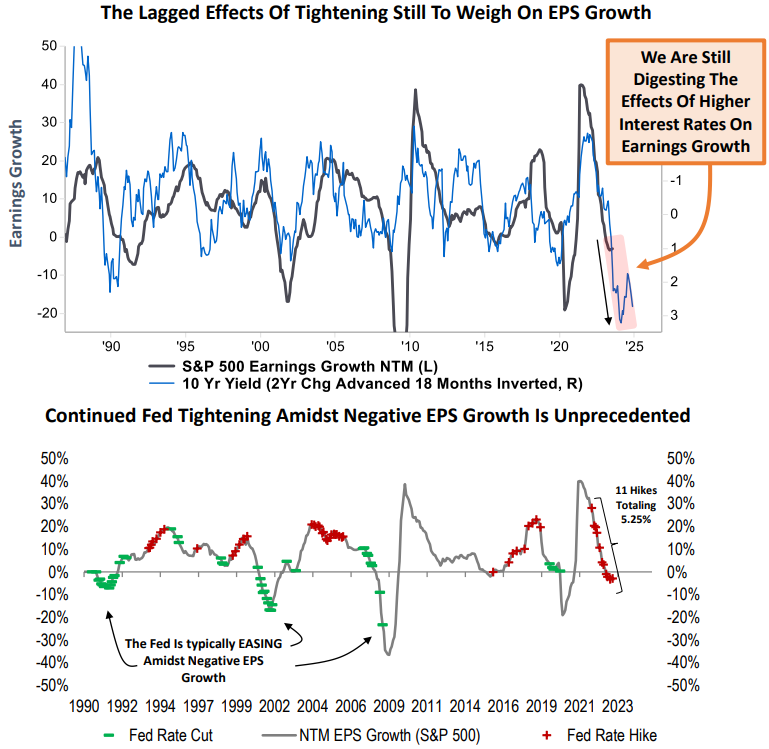

|"it is extremely unusual to see the Fed hiking while earnings growth is slowing sharply into negative territory. In our opinion, earnings will continue to face significant headwinds well into 2024."

-Piper Sandler, Michael Kantrowitz

* source: Piper Sandler

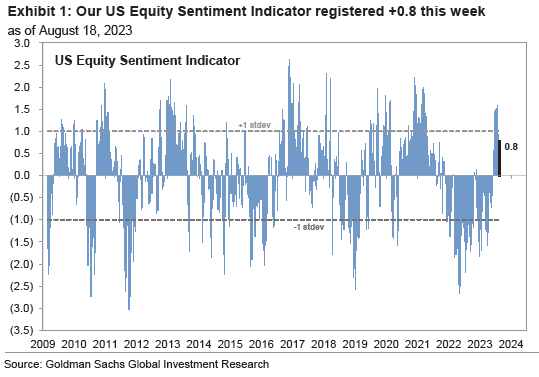

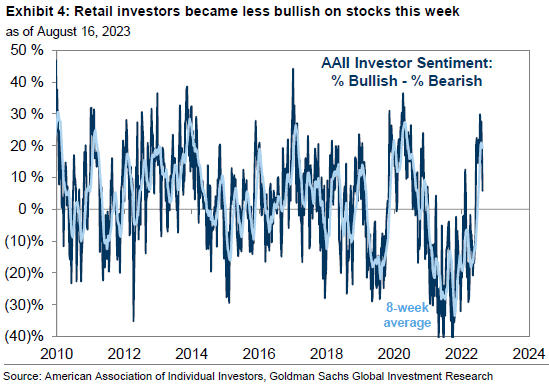

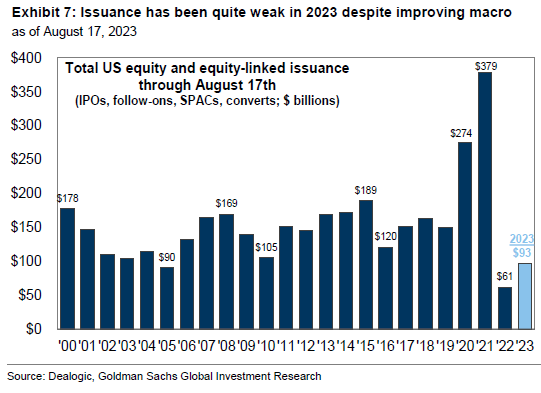

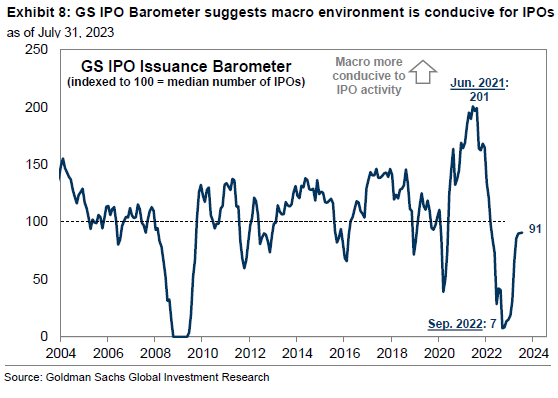

|"The re-opening of the buyback blackout window will provide a boost to equity demand in coming weeks although a flurry of expected equity issuance this fall may provide a partial offset." -Goldman Sachs Global Investment Research

Equity Sentiment Indicator falling... + equity issuance + IPO market

* source: Goldman Sachs Global Investment Research

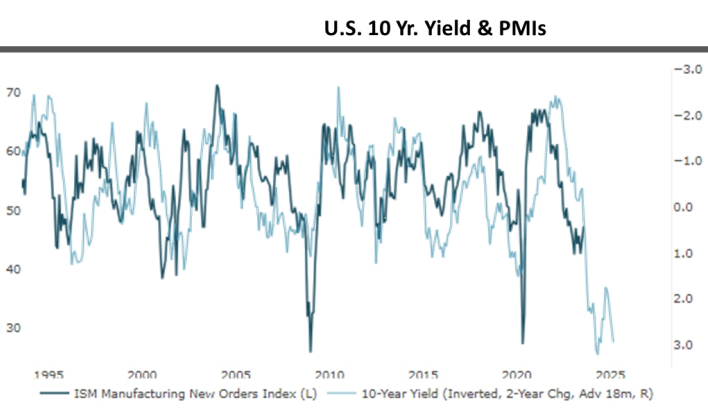

|"we would expect the historically tight relationship between risk factors and PMIs to hold and either PMIs rise or risk factors take a sharp move lower" -Piper Sandler

* source: Piper Sandler

1) KEY TAKEAWAYS

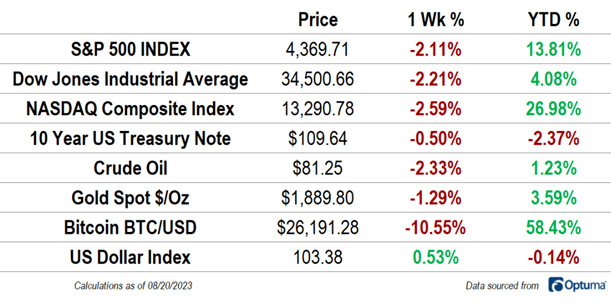

1) Equities mostly HIGHER + TYields HIGHER

| "For the most part, another earnings season is in the books. Until 3Q earnings starts, economic data is likely to be in the spotlight again. This week we will get flash readings on key global PMIs." -Piper Sandler

DJ +0.0% S&P500 +0.5% Nasdaq +1.0% R2K -0.1% Cdn TSX +0.3%

Stoxx Europe 600 +0.3% APAC stocks MIXED, 10YR TYield = 4.320%

Dollar LOWER, Gold $1,891, WTI +1%, $82; Brent +1%, $85, Bitcoin $26,048

NOTABLE HEADLINES

- Surge in zero-day options sparks fears over market volatility – FT

- Big treasury rout lures fresh buyers – WSJ

- Strong US economy forces investor rethink on interest rates – FT

- Bond investors brace for supply freight train before fed confab – BBG

- Why the era of historically low interest rates could be over – WSJ

- US consumers near day of reckoning as pandemic cash stash shrinks – BBG

- China surprises with modest rate cut amid growing yuan risks – RTRS

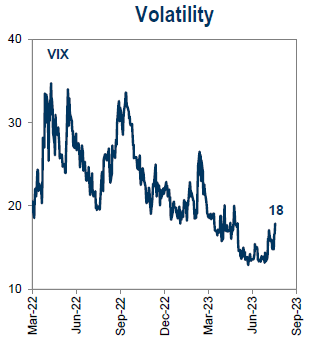

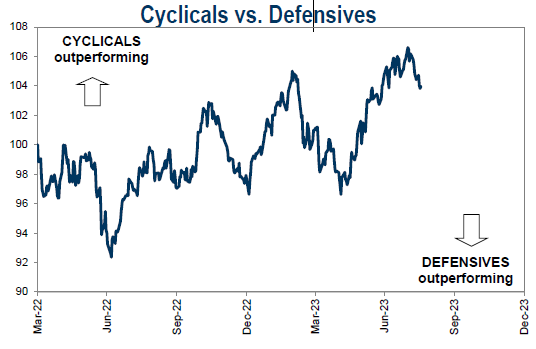

2) Volatility has returned slightly

Defensives performing slightly better as markets drop

* source: Goldman Sachs Global Investment Research

3) Fed's Jackson Hole symposium = highlight for investors NEXT WEEK. +investors focus on global flash PMI prints + durable goods orders in the US + sentiment indicators across Europe.

* source: Grindstone Intelligence

4) Food for thought: no pun intended

"Of the 25 largest fast-food chains globally, 22 come from the United States, with every single one of the top 17 being American-owned" -Chartr

"But, adjusting for its relative size, no chain has grown faster than Crumbl Cookies, which opened an astonishing 363 new units, adding a whopping 53% to its store count in a single year: not bad for a company founded in 2017 that relies on the humble cookie to pay its bills. Chicken lovers are also increasingly spoilt for choice, as chains like Wingstop, Popeyes and Chick-fil-A continue to expand — adding more than 500 units between the 3 of them in the last year. And if that still doesn’t whet your appetite, there’s also been room for both Taco Bell and Chipotle to keep expanding as well."

"Chick-fil-A continues to post some of the most mind-boggling numbers in the industry, with the average store selling $6.7m worth of food and drink every year."

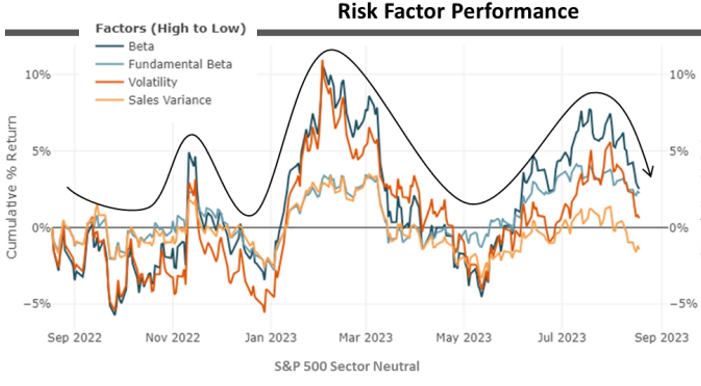

5) "Optimism that CPI will continue to fall and we will have a soft landing has helped support risk positioning despite the weakness in PMIs.

Over the last year, risk factors have moved a ton but gone nowhere. While positioning and PMIs trend together over the long-term, they do not move tick for tick and can diverge for periods." -Piper Sandler

* source: Piper Sandler

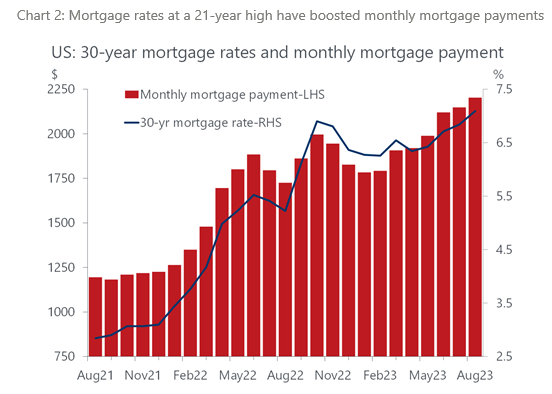

6) Mortgage rates + payments rising...

* source: Oxford Economics

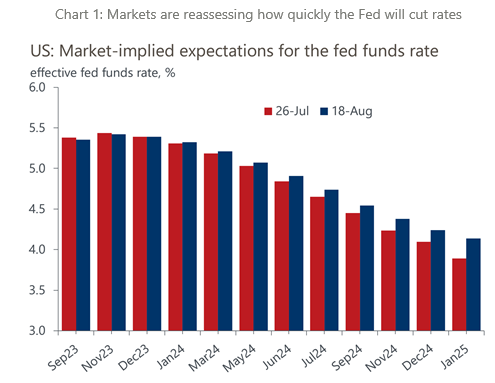

7) the outlook for rates: to decline but more slowly = higher for longer

* source: Oxford Economics

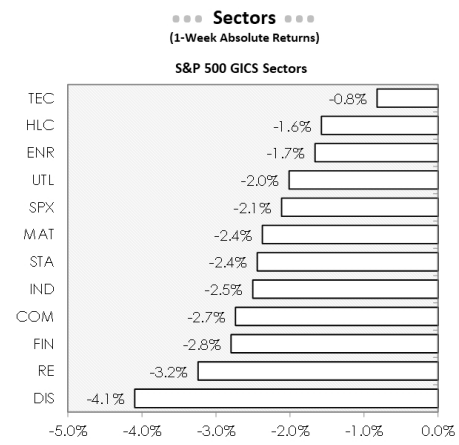

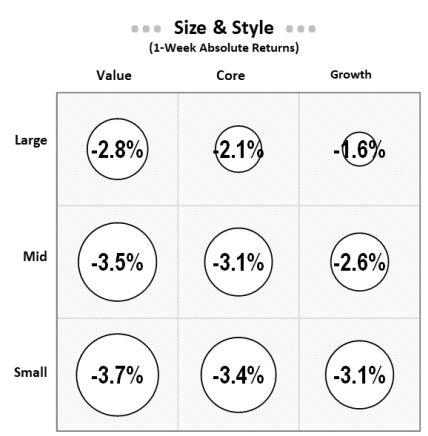

8) Performance

* source: Piper Sandler

2) ESG, COMPILED BY NATHAN GREENE

OFF TODAY

3) MARKETS, MACRO, CORPORATE NEWS

- Is the U.S. economy really growing by 5.8%? not so fast – Barron’s

- China urges more loans, debt risk reduction as woes compound – BBG

- US grows doubtful Ukraine counteroffensive can quickly succeed – FT

- Ukraine running out of options to retake significant territory – WaPo

- China launches military drills around Taiwan after VP’s US stopover - FT

- Silicon Valley start-ups revive listing plans as Arm reignites IPO market – FT

- David Solomon retains board and investor backing amid internal backlash – FT

- Old Dominion Freight Line bids $1.5 billion for Yellow Terminals – BBG

- US insurance giant Marsh set for $448 million Honan deal – BBG

- Sunak to spend £100m of taxpayer cash on AI chips – Telegraph

- DuPont is in talks to sell Delrin unit to private equity firm for $1.8 billion – BBG

- Pacific Current’s talks to buy Fortlake AM – TA

- The Premier split could unlock more than $1b in value – AFR

- Entain in audacious play for Racing.com – TA

- Citi considers overhaul that would hand more power to chief Jane Fraser - FT

- The AI trade faces its first major test with NVIDIA earnings – WSJ

- Cruise reduce robotaxi fleet in SF while CA DMV investigates ‘incidents’ – CNBC

- Hedge fund Sculptor rejects unsolicited offer from Weinstein - BBG

- Oil/Energy Headlines: 1) China's Saudi crude imports to remain depressed through third quarter-RTRS 2) Iranian oil cargo seized by US begins unloading after long delay-RTRS 3) Lawmakers urge Biden to resolve offloading delay of seized Iran oil tanker-RTRS 4) US and Iran rely on shadow diplomacy where open deals would fail-BBG

About the author

Massud Ghaussy, CFA, is part of Nasdaq's IR Insights team and delivers daily insights that empowers readers to get a sense of the important issues impacting the day's trading.