Taiwan Semiconductor Manufacturing (NYSE: TSM) has had a great 2024, as it's up more than 80%. With that kind of performance in the rear-view mirror, many investors may wonder if they've missed the boat.

Possibly not: Several positive trends are on the horizon, and this could be the start of something even bigger.

Taiwan Semiconductor is a key part of AI proliferation

Taiwan Semiconductor is the world's largest contract chip manufacturer. Essentially, it specializes in producing the chips designed by better-known tech names such as Apple, Nvidia, and AMD. This allows its customers to stay relatively asset light and avoid investing in the highly specialized infrastructure required to manufacture the chips.

This also provides a benefit for Taiwan Semiconductor. It doesn't matter to TSMC which companies win the races to become the leading provider of artificial intelligence (AI) chips, electric vehicles, or smartphones. It does chip manufacturing for almost every one of the leading tech brands, so it will benefit regardless of which of them is leading at any given time.

So far in 2024, the AI trend has been a large component of TSMC's growth story, as management alluded to during its Q1 conference call. They predict that the company's AI-related revenue will grow at a 50% compound annual rate through 2028, and will account for more than 20% of overall revenue by the end of that five-year period. Considering that TSMC has produced over $70 billion in revenue over the past 12 months, that's a lot of new sales coming.

Another short-term catalyst will be Apple Intelligence. Apple's AI services will only be available on its latest generations of iPhones and other products. Given that Apple already provides around a quarter of Taiwan Semi's annual revenues, a surge in upgrade activity among its loyal user base could also give the foundry a noteworthy boost.

So the potential growth catalysts are visible for Taiwan Semi, but has their impact already been baked into the stock price?

High expectations are already priced into the stock

The guiding light for Taiwan Semi investors has been management's forecast for 15% to 20% compound annual revenue growth for the next several years. Unfortunately, the company did not give a specific year range, so for the purposes of attempting to weigh the stock's current valuation, let's postulate a 15% growth rate over the next five years.

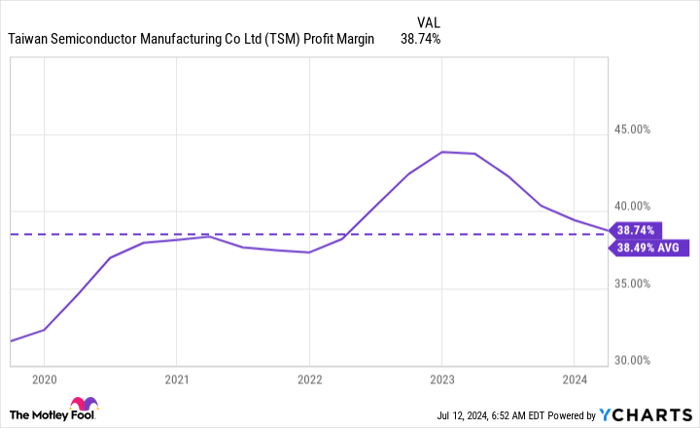

If TSMC does grow at that rate, its annual revenues would basically double to $144 billion. If it can maintain the near-40% profit margin that it has averaged over the past five years, that revenue would result in about $56 billion in profits.

TSM Profit Margin data by YCharts.

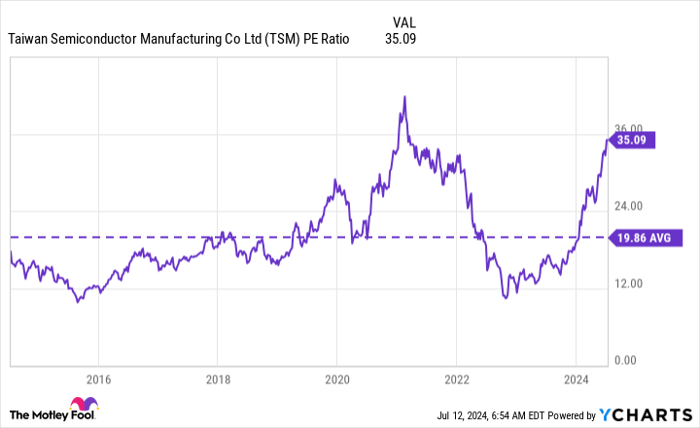

Over the past decade, Taiwan Semiconductor has, on average, traded for about 20 times earnings. That's a fair valuation for a company with above-average execution.

TSM PE Ratio data by YCharts.

So if Taiwan Semiconductor can grow at a 15% compound annual rate over the next five years, maintain its profit margins, and trade at its decade-long average valuation, the company would at the end of the time be valued at $1.12 trillion. Considering that it's worth around $950 billion right now, that would be a compound annual growth rate of just 3.2% for the stock.

That's not a great outlook for the next five years, and it shows how expensive the stock has gotten. But if we shift our assumptions toward the top of management's forecast range, figuring that the company will grow at 20%, and further assume that it will trade at an above-average valuation of 25 times earnings, its annualized growth rate would be 12.7% -- a potentially market-beating return.

So is it too late to buy TSMC stock? One analysis says "yes" while the other says "no."

I'd say look at the facts. First, Taiwan Semiconductor is a vital supplier to a host of tech firms across an array of specialties, and will benefit from their growth for years to come. Second, there are high growth expectations already baked into the stock price.

As a result, I'd say be cautious with TSMC stock. If you want to open a position, there's no reason to go all in immediately. Instead, I'd suggest buying a fraction of what you'd want your final position to be; that way, you can follow the company and take advantage if better opportunities present themselves.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $774,281!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 15, 2024

Keithen Drury has positions in Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.