Things can change relatively fast in the stock market, as telemedicine specialist Teladoc Health (NYSE: TDOC) can attest. Not too long ago, the company's shares were soaring because the need for its services exploded amid the pandemic. But the stock has lost about 55% of its value over the past year alone. One key factor behind this poor performance has been Teladoc's disappointing financial results. The good news for the company is that the telehealth market is here to stay, and according to estimates, it will grow rapidly in the coming years.

Is that a good enough reason to buy the stock now? Let's dig in.

Will Teladoc's financial results improve?

Teladoc's results -- specifically, its net losses -- were abysmal last year. That's because the company had to incur hefty impairment charges related to its 2020 acquisition of Livongo Health. Teladoc overpaid for this acquisition, hence the charges. In 2022, the company's net loss came in at a massive $13.7 billion -- or $84.60 on a per-share basis -- significantly worse than the net loss of $428.8 million reported in the previous fiscal year.

But it seems as though Teladoc will improve on this front this year. The company expects a net loss per share between $1.75 and $1.25 for 2023. Not only is that orders of magnitude better than what it recorded in 2022, it even shows progress compared to 2021, when it had a net loss per share of $2.73.

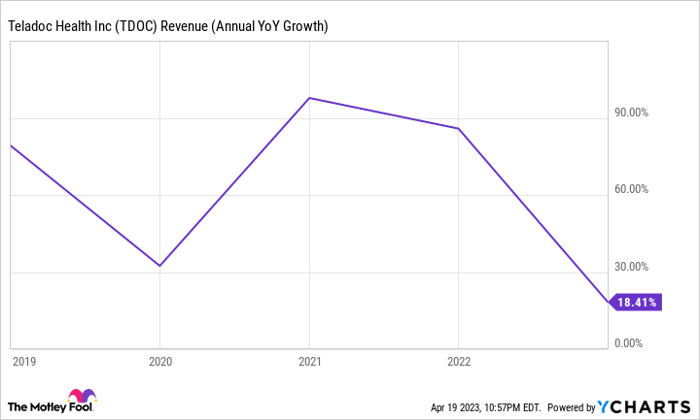

This suggests that Teladoc is getting closer to breaking even and -- eventually -- achieving profitability. Management has highlighted the importance of becoming profitable on a generally accepted accounting principles (GAAP) basis, and in my view, that should come within the next few years. On the other hand, Teladoc's top-line growth rates have slowed, a trend that should continue in 2023.

The company expects revenue between $2.6 billion and $2.7 billion, which would represent a year-over-year increase of about 9% at the midpoint. That's much lower than what it has gotten investors used to in recent years.

TDOC Revenue (Annual YoY Growth) data by YCharts

Teladoc's revenue growth could accelerate if it takes advantage of the opportunities in the expanding telehealth market.

The path forward for Teladoc

Telehealth offers several advantages for both patients and physicians. For the former, virtual consultations save them the trouble of making a trip -- that's time and money, two valuable resources, especially when we add up these savings over hundreds of consultations. Meanwhile, for physicians in many specialties, telehealth leads to cost savings. Consider one specific example: mental health.

Teladoc offers mental health services through its BetterHelp platform. The company does not give the option of in-person sessions, but this allows it to offer lower prices than traditional therapy. That's probably because not having to worry about in-office visits allows mental health specialists to save on various overhead costs. These doctors can then pass these cost savings onto patients, and everyone wins.

BetterHelp has been one of Teladoc's key growth drivers over the past two years, but it is also looking to make headway in the management of chronic illnesses. After all, that is why it acquired Livongo Health, a company that specializes in this area. Teladoc recently announced that it would extend its existing provider-based care services, which already catered to hypertension and diabetes, to pre-diabetes and weight management.

It estimates that 42% of people in the U.S. are obese, while 33% have pre-diabetes. Teladoc ended 2022 with 83.3 million U.S. paying members for its integrated care services, an increase of 7% year over year. However, its BetterHelp platform ended the year with just 419,000 members, growing 37%. Its chronic care program had about 1 million clients as of the end of 2022, rising by 16% compared to 2021.

If Teladoc can increase the penetration rate of its mental health and chronic care services among its existing paying members, it will allow the company to grow its revenue and earnings for a long time, even without adding brand-new paying users.

A good entry point for patient investors

Given Teladoc's leadership in the telehealth industry -- which will continue growing -- and its ability to expand its suite of services, the recent sell-off may be overdone. Plus, the biggest reason investors avoided the stock last year (Teladoc's deep net losses) seems to be in the rearview mirror.

As of this writing, the stock's forward price-to-sales ratio is just 1.7. All these factors combine to make Teladoc shares a good buy, especially while they remain significantly down.

10 stocks we like better than Teladoc Health

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Teladoc Health wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of April 10, 2023

Prosper Junior Bakiny has positions in Teladoc Health. The Motley Fool has positions in and recommends Teladoc Health. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.