Microsoft (NASDAQ: MSFT) recently kicked off a new fiscal year with a bang. The now 45-year-old software icon reported revenue and net income of $37.2 billion and $13.9 billion during the three months ended Sept. 30, 2020 (first-quarter fiscal 2021). Those figures represented respective increases of 12% and 30% from a year ago. Under the guiding hand of CEO Satya Nadella, Microsoft has been able to sustain its decades-long growth story via the cloud, and I wouldn't be quick to bet against the tech giant anytime soon.

But with the tech giant's stock trading for well over 30 times trailing 12-month earnings, is it still a buy?

Image source: Getty Images.

Enduring growth, enviable margins

In keeping with the last few years, it was cloud-based services that led the way again in Microsoft's latest report. Broadly speaking, product-based sales were flat from a year ago at $15.8 billion, but services increased 23% to $21.4 billion -- propped up by everything from booming business video conferencing tool Teams to AI systems powered by the Azure cloud juggernaut. Further breaking down Microsoft by its three reporting segments showed the following:

- Productivity and Business Processes increased 11% year over year to $12.3 billion, driven by Office 365 and related subscriptions and a 16% increase in LinkedIn revenue.

- Intelligent Cloud -- which houses the Azure public cloud computing business -- increased 20% year over year to $13.0 billion.

- More Personal Computing increased 6% year over year to $11.8 billion, with a 5% decline in Windows operating system revenue bailed out by 30% and 37% gains in Xbox and Surface sales.

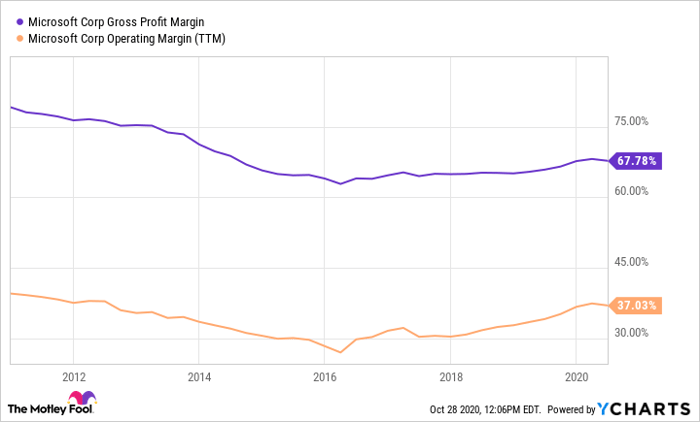

What is really impressive about Microsoft's results is the long-term trend it reinforces: The power of technology to maintain strong profit margins. Revenue growth is one thing, but profit margins that continue to expand at an even faster pace is another entirely. The company has innumerable competitors nipping at its heels, yet Microsoft has been able to maintain its pricing power with its cloud transformation and is slowly inching its way higher as each new dollar carries fewer associated costs. This is one old business, but operating margins nearing 40% is usually the realm of far younger and smaller companies.

Data by YCharts.

This old tech story illustrates why the myriad small cloud stocks out there carry such hefty valuations. Despite fierce competition, many years later a tech firm can remain in growth mode if it continues to allocate cash to the right projects at the right time. For Microsoft, the cloud was that catalyst that started to rekindle profitability five years ago, setting the stage for the next run higher in the coming years.

Not a bad bulwark to build a portfolio around

Paired with its enduring top- and bottom-line expansion, Microsoft also continues to return ample cash to shareholders via its dividend ($3.86 billion in the last quarter, good for a 1.1% annual yield as of this writing) and share repurchases ($6.74 billion in the last quarter). It also has some of the deepest pockets around with $138 billion in cash and short-term equivalents at the end of September 2020, offset by only $63.6 billion in debt.

Digital transformation is picking up in earnest during the pandemic, providing a strong tailwind for Microsoft in the decade ahead. This will not be the fastest-growing tech stock out there by any stretch, but shares are priced at a premium for good reason. Slow and steady sales growth will lead to even higher bottom-line growth over time as the cloud continues to pay rich rewards. This tech company has been through a lot over the decades, and I think it will be just fine whatever challenges might be lurking around the next corner. For investors looking for a stable tech name to build a portfolio around, Microsoft should be part of the equation.

10 stocks we like better than Microsoft

When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the ten best stocks for investors to buy right now... and Microsoft wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of October 20, 2020

Teresa Kersten, an employee of LinkedIn, a Microsoft subsidiary, is a member of The Motley Fool's board of directors. Nicholas Rossolillo owns shares of Microsoft. His clients may own shares of the companies mentioned. The Motley Fool owns shares of and recommends Microsoft and recommends the following options: long January 2021 $85 calls on Microsoft and short January 2021 $115 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.