Unless you've been living under a rock, it's hard not to have noticed the growth of the Chinese e-commerce platform Temu over the last year. After flooding the internet with advertisements and spending a boatload of money on two Super Bowl commercials, the PinDuoDuo-owned (NASDAQ: PDD) app has skyrocketed to the top of the downloads list for mobile app stores in the United States.

Offering free shipping and huge discounts for first-time customers, Temu has drawn interest from tens of millions of shoppers in the United States, replicating a model that worked in the Chinese market. Have we finally found the killer competitor to Amazon (NASDAQ: AMZN)? Or is Temu just a flash in the pan? Let's investigate.

What the heck is Temu?

Temu was born out of PinDuoDuo, a Chinese e-commerce company that has gained rapid success in the East Asian nation since launching in 2015. The U.S. version of the app launched around a year ago in the country and has grown at an extremely quick pace. Spending a boatload of money on advertising, Temu has vaulted itself to be the most downloaded mobile application in 2023, with tens of millions of downloads just in the United States.

The platform offers cheap and unbranded products, typically at a large discount. For example, right now I can buy a 26-piece nail clipping and grooming set for under $5. Temu sources its products directly from Chinese manufacturers in Guangzhou and is currently offering free shipping as a promotion to lure consumers to try the platform. Plenty of customers have complained about poor customer service and low-quality products, but with items going for $5 or less, people don't seem to mind at the moment.

But is this business model sustainable?

The key differentiator: Infrastructure

If you just looked at the headline numbers, you'd think Temu had finally cracked the code to compete against Amazon. It is likely doing billions of dollars in sales across its platform in the United States compared to zero a little over a year ago. An impressive feat, no doubt.

But if you look under the hood, this growth looks unsustainable. According to an investigation by WIRED magazine, Temu loses about $30 for every order made on its platform as it subsidizes free shipping while also spending a boatload on marketing expenses. And it looks like this spending isn't slowing down soon, with Temu planning to up its advertising spend from $1.4 billion in 2023 to $4.3 billion in 2024.

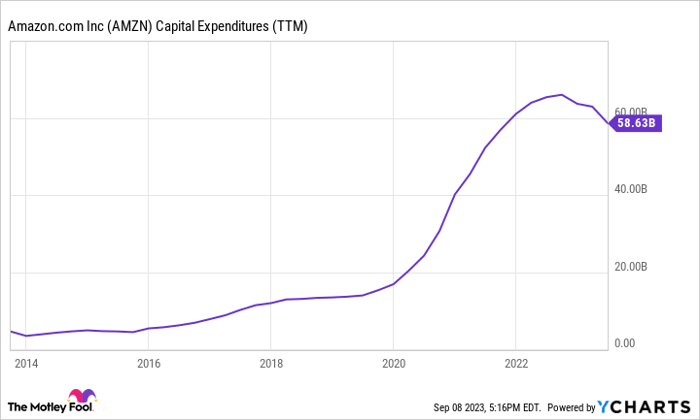

AMZN Capital Expenditures (TTM) data by YCharts

In the short run, Temu could keep growing at an impressive pace by losing money on every order. But eventually, it will have to generate positive unit economics, which will be tough to do when competing with Amazon's vertically integrated e-commerce infrastructure. Amazon has spent hundreds of billions on capital expenditures over the last decade, a lot of which has gone to delivery vehicles, warehouses, and airplanes to help quickly deliver products to customers. Temu has none of this infrastructure. Unless it can somehow get hundreds of billions of dollars to build out these capabilities (which is essentially impossible), it never will.

Vertical integration will give Amazon a durable advantage over Temu. The Chinese app will either have to charge for shipping or increase its selling prices compared to Amazon's, both of which will decrease its customer value proposition vs. the incumbent. Or it can lose money on every order until it runs out of money entirely. Whatever happens, Amazon should come out relatively unscathed.

Amazon shareholders have nothing to worry about

The headlines may get scary for Amazon investors in the next few quarters if Temu continues its advertising blitzkrieg. However, shareholders need to remember that this spending cannot continue forever if Temu loses money on every order.

Through years and years of infrastructure spending, Amazon has built up a competitive moat that will be difficult for any e-commerce platform to match. Competitor Shopify recently threw in the towel with its e-commerce delivery business and was forced to come to the table to bring Buy With Prime as a service for its merchant partners.

It is becoming increasingly difficult to compete with Amazon's platform in the United States. This should have long-term investors in Amazon stock resting easy.

10 stocks we like better than Amazon.com

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Amazon.com wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of September 5, 2023

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Brett Schafer has positions in Amazon.com. The Motley Fool has positions in and recommends Amazon.com and Shopify. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.