The industrial conglomerate has long been a fascinating investment proposition. With a 64-year history of increasing dividends and a 5.6% yield, it's easy to see why 3M (NYSE: MMM) will attract income-seeking investors. In addition, restructuring actions promise to improve profit margins and drive earnings growth as its cyclical end markets improve over time. Does it all add up to make the stock a buy?

3M isn't perfect

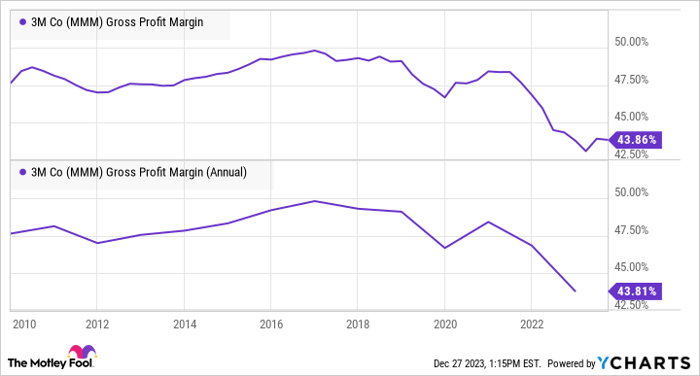

The industrial conglomerate is far from perfect. The company's high-profile legal settlements relating to its use of PFAS chemicals and allegedly faulty combat-arms earplugs have attracted all the attention. In addition, I would also point out the company's history of missing its growth guidance and its disappointing operational performance characterized by the long-term decline in its profit margin. This comes after a period of substantial acquisition and disposal activity, principally in its healthcare segment, none of which appears to have helped its margins.

MMM Gross Profit Margin data by YCharts.

Dividend problems?

In addition, there's the tricky question of the sustainability of 3M's dividend. Given the company's proud history of raising dividends, the last thing management probably wants to do is to cut them. However, several pressures are building up, which suggest that might be the best policy.

First, 3M is set to spin off its healthcare segment, Solventum, in the first half of 2024. While 3M will retain a 19.9% stake in Solventum, which could be sold to raise cash, losing the stable cash flows from the healthcare business will only increase the volatility of 3M's cash flows.

Second, 3M has cash calls coming from its legal settlements. In the words of CFO Monish Patolawala at an investor conference, the combat-arms settlement "is a combination of $5 billion in cash and $1 billion in stock," which "is going to get paid over the next 6 to 7 years." Meanwhile, the PFAS-related settlement is "$10.5 billion to $12.5 billion with a present value of $10.3 billion, again, for a payout that's going to be spread over 13 years."

These are significant cash calls, and Wall Street analysts expect 3M to generate $4.5 billion in free cash flow (FCF) in 2023 and then $4.3 billion in 2024. These figures easily cover its current $3.3 billion dividend payout. But note, these FCF estimates include the healthcare segment, which will be spun off, and 3M still has to fund the legal settlements described by Patolawala above.

If management and/or the board decide a dividend cut is in the best interest of shareholders (whom the board represents), you can bet it won't be a decision taken lightly. Nevertheless, it is a real possibility and hangs over the stock's prospects.

Image source: Getty Images.

Is improvement coming for 3M in 2024?

On a more positive note, evidence suggests that the significant restructuring actions taken earlier in 2023 are starting to take effect. For example, 3M's margin is improving despite a deteriorating sales outlook. Moreover, on the lastearnings call management reaffirmed it was on track to deliver benefits of $400 million to $450 million in 2023, totaling $700 million to $900 million from 2023 to 2025. These long-term annual benefits will come at a one-time cost of $400 million to $450 million in 2023 and $700 million to $900 million from 2023 to 2025.

Moreover, while 3M enters 2024 with deteriorating sales momentum (organic revenue declined 3.7% in the third quarter), lower interest rates will help its key cyclical end markets like electronics, automotive, and consumer spending. As such, don't be surprised if 3M starts 2024 in bad shape and then starts to recover in the back half of the year.

Image source: Getty Images.

Is 3M stock a buy?

The uncertainty over its dividend and the near-term deterioration in its end markets mean that 3M is entering 2024 with question marks hanging over it. On the other hand, there's some, albeit nascent, evidence of margin improvement, and the prospect of lower rates through 2024 is positive for an industrial company like 3M.

As such, 3M probably isn't a buy for most investors. That said, the stock's valuation is undeniably worth monitoring to try and initiate a long-term position, assuming a buying opportunity occurs in 2024.

Should you invest $1,000 in 3M right now?

Before you buy stock in 3M, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now... and 3M wasn't one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 18, 2023

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool recommends 3M. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.