As was widely anticipated, Apple (NASDAQ: AAPL) reported lower year-over-year revenue for its quarter ending in early July. The decline wasn't as dramatic as feared, however. Its top line fell from $83 billion a year earlier to $81.8 billion this time around versus estimates of $81.7 billion. Earnings grew from $1.20 per share then to $1.26 now, topping estimates of $1.19 per share.

Once again, declining iPhone revenue is a key culprit in this third consecutive quarterly revenue dip. Apple only sold $39.7 billion worth of the popular smartphone during its third fiscal quarter of the year, down from the year-ago comparison of just under $40.7 billion.

Let there be no mistake -- the revenue dip isn't solely the result of lower selling prices. Apple is selling fewer iPhones.

The thing is, it doesn't really matter.

Yes, iPhone sales are slowing down

Longtime followers of Apple stock already know the company stopped sharing unit sales data back in 2018. Other in-the-know observers have continued to track unit sales anyway, confirming what many investors quietly suspect: Apple isn't selling as many iPhones as it used to.

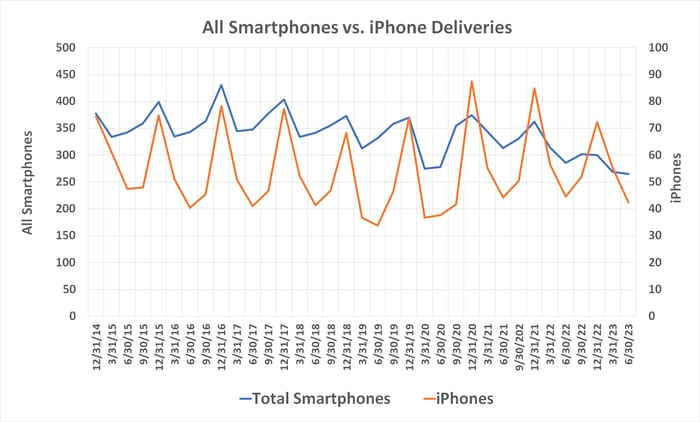

Technology market research outfit IDC is one of these other observers. It estimates unit sales of the iPhone slipped to 42.5 million in the second quarter of this year, extending weakness that first took shape following the late-2020 peak. In fact, last quarter's iPhone shipment count was the lowest quarterly figure since the third quarter of 2020, when the number was on the way up.

Data source: IDC. Chart by author. Figures are in millions.

It's not entirely Apple's fault. As the graphic above also shows, the whole smartphone market has been shrinking since 2017. Consumers are keeping their increasingly expensive devices for longer, and there are fewer cellphone owners left to convert to smartphone users.

Numbers from Pew Research say that 97% of adults living in the U.S. now own a mobile phone, and 85% of these people own a smartphone. They don't need another one, at least not yet. It's not a stretch to presume we're seeing similar cellphone and smartphone ownership rates overseas.

Apple shareholders need not worry just yet, though. The company's more than ready for this slowdown.

Services are the future, devices are a means to the end

Apple's Q3 press release alluded to the growth engine that's picking up the slack being left behind by iPhone sales. CEO Tim Cook explained, "We are happy to report that we had an all-time revenue record in Services during the June quarter, driven by over 1 billion paid subscriptions." Services revenue grew from $19.6 billion in the third fiscal quarter of 2022 to $21.2 billion a quarter ago.

The comment, however, doesn't do this particular profit center justice.

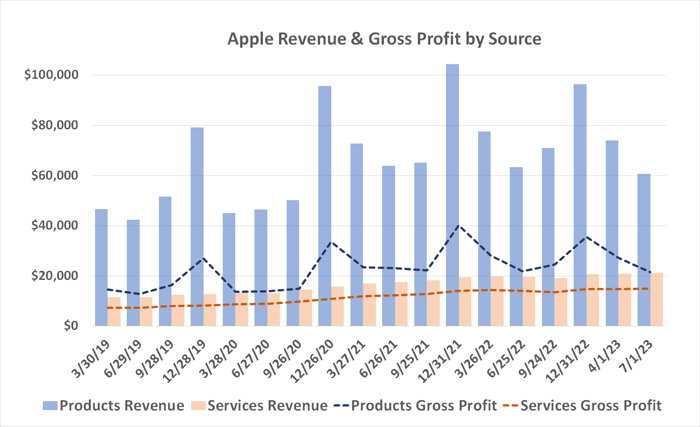

Apple's quarterly reporting doesn't make this terribly clear to the casual observer. But profit margin rates on services are much higher than the company's profit margins on physical products. For perspective, last quarter's product sales of $60.6 billion cost Apple $39.1 billion, leaving behind a profit of $21.5 billion, or 35.5% of revenue. Services revenue of $21.2 billion, on the other hand, only cost the company $6.2 billion. That's a difference of $15 billion, translating into a profit margin rate of 70.7%.

The majority of Apple's revenue obviously still comes from sales of physical products. So, most of its gross profits also still come from sales of goods like iPhones, iPads, and Mac computers (although iPhones make up the majority of these sales).

Data source: Apple. Chart by author. Figures are in millions.

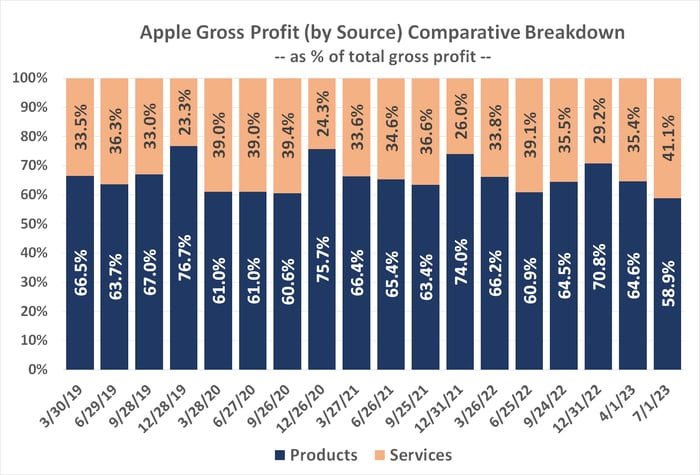

Something of a milestone was met in this regard last quarter. For the first time ever, products accounted for less than 60% of the company's gross profit, while services accounted for more than 40% of its gross income.

Data source: Apple. Chart by author.

Given the bigger-picture slowdown in all smartphone sales, don't look for this shift in the company's profit mix to reverse course anytime soon.

But that may ultimately be the more profitable path to take.

Buy Apple stock because it's handling the shift like a champ

Don't misread the message. Apple would love to have more of both types of revenue, as the ongoing proliferation of iPhones is the key driver of its Services arm's sales and profit growth. As Cook explained in the press release, the company watched its "installed base of active devices reach an all-time high" in the same quarter Services revenue reached a record as well. Connect the dots.

Given the smartphone market's prolonged and strengthening headwind, however, meaningful Product sales growth probably isn't in the cards anytime soon.

Fortunately, the company's got a great plan B that's not only already in place but is already working even as the company is still learning how to extract more revenue from iPhone owners (and iOS users in general). As it gets better at doing this, don't be surprised to see Services eclipse Products as Apple's top profit center. That would be a much more consistent business to prioritize anyway.

Bottom line? Shares of Apple fell following Thursday's post-close release of last quarter's numbers, with investors largely concerned about the third-straight sales slump. Don't sweat it. The dip just makes for an even better buying opportunity.

10 stocks we like better than Apple

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Apple wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of August 1, 2023

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.