Innodata Inc.’s INOD first-quarter 2026 results suggest that operating leverage is becoming a more visible part of the story. Adjusted EBITDA rose to $25 million, up from $12.7 million in the prior-year period, marking roughly 96% growth. That significantly outpaced revenue growth of 54%, with sales reaching $90.1 million. Management highlighted this gap directly, noting that EBITDA grew about 1.8 times faster than revenues, which it described as evidence that operating leverage is now embedded in the model.

The quarter also showed how Innodata’s mix is shifting toward higher-value AI services. The company is expanding beyond traditional post-training work into pre-training, evaluation, trust and safety, agent optimization and physical AI data solutions for major hyperscalers and frontier AI labs. Management noted that proprietary platforms, reusable off-the-shelf datasets and synthetic data technologies are beginning to improve margins because they reduce dependence on linear headcount growth.

Margin expansion further reinforced the trend. Adjusted EBITDA margin reached 28%, while adjusted gross margin improved to 47%, exceeding the company’s long-term 40% target. At the same time, Innodata continues to deepen relationships with major hyperscaler and enterprise AI customers. Management disclosed new engagements with a large technology customer that could contribute roughly $51 million in 2026 revenues, while additional opportunities are emerging across enterprise and federal AI markets.

The key question is sustainability. Management said it does not expect a near-term “step change” in investment expenses, even as it continues adding sales, R&D and product talent. If revenues keep scaling through larger AI programs and higher-leverage platform offerings, INOD’s EBITDA growth may continue to outpace sales growth. But investors will likely watch whether this margin strength holds as new programs ramp and the company reinvests for growth.

Margin Expansion Faces Competitive Pressures

Innodata faces rising competition from AI software and infrastructure players like Palantir Technologies Inc. PLTR and C3.ai, Inc. AI, which continue expanding their enterprise AI capabilities and could pressure margins and customer growth over time.

Palantir is rapidly scaling profitability alongside explosive AI demand, with first-quarter 2026 revenues surging 85% year over year and adjusted operating margin reaching 60%, reflecting significant leverage from its expanding AIP platform adoption across commercial and government markets. Palantir also relies on its core platform architecture, specifically its central "Ontology," which functions as a "no slop zone" to coordinate purpose-built AI agents with exact precision, cost attribution and governance.

C3.ai, on the other hand, is emphasizing enterprise AI transformation across industries such as manufacturing, energy, healthcare and defense. The company is concentrating on areas like supply-chain optimization, asset performance and generative AI applications while pursuing large-scale enterprise-wide AI deployments. C3.ai is pursuing its own margin-improvement strategy through aggressive restructuring, workforce reductions and AI-led productivity gains. These moves show that operating leverage is becoming a key battleground across the enterprise AI industry, increasing pressure on Innodata to sustain both growth and margin expansion.

INOD’s Price Performance, Valuation & Estimates

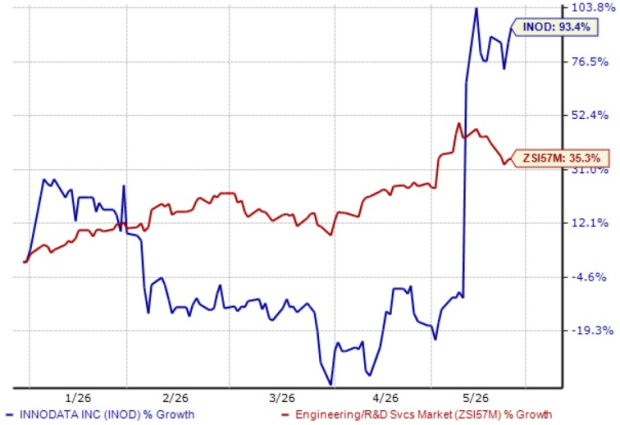

Year to date, INOD stock has surged 93.4%, outperforming the industry’s 35.3% growth.

Image Source: Zacks Investment Research

From a valuation standpoint, INOD trades at a forward price-to-earnings ratio of 75.93, much higher than the industry’s average of 31.35.

P/E (F12M)

Image Source: Zacks Investment Research

INOD’s earnings estimates for 2026 and 2027 have moved upward in the past 30 days to 99 cents and $1.78 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 7.6% and 72.2%, respectively.

Image Source: Zacks Investment Research

INOD currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpC3.ai, Inc. (AI) : Free Stock Analysis Report

Innodata Inc (INOD) : Free Stock Analysis Report

Palantir Technologies Inc. (PLTR) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.