Leading in business requires constant awareness to navigate through trends and rough patches. The dramatic rise in interest rates over the last two years has deeply shifted business priorities.

In March of 2022 the effective funds rate was 0.08%.

Then the Federal Reserve started raising rates to counteract inflation, peaking at 5.33% as of July 22, 2024.

Rising interest rates change business incentives

Why do rising interest rates matter for you, people leader?

The key thing is that rising interest rates prioritize cash and profitability over growth and spend.

Why?

As a business, when you’re in a low interest rate environment, this means that the payments on loans are so low that it’s worth getting a loan to grow the business.

As an investor, when you’re in a low interest rate environment, investing in fixed income doesn't yield much. So, to hit their return baselines, investors turn to equity investments–often both public and private markets.

As a startup founder, when you’re in a low interest rate environment, investor’s demand for equity can make it easier to fundraise more to fuel growth.

And as a nonprofit ED, when you’re in a low interest rate environment, it’s easier for non-profits to fundraise, money is cheap and investors who have taken profits look to donate to offset the tax hit.

The inverse is true when interest rates are high. The system now rewards savers and punishes borrowers. Money is no longer “cheap” as investors aren’t incentivized to take on risk when they are getting high yield in savings or fixed income products.

Which means your CEOs and CFOs have a much harder time raising or getting money to expand the business or your non-profit. So for you, as a people leader, a high-interest rate environment means improving what you have. Not expanding it.

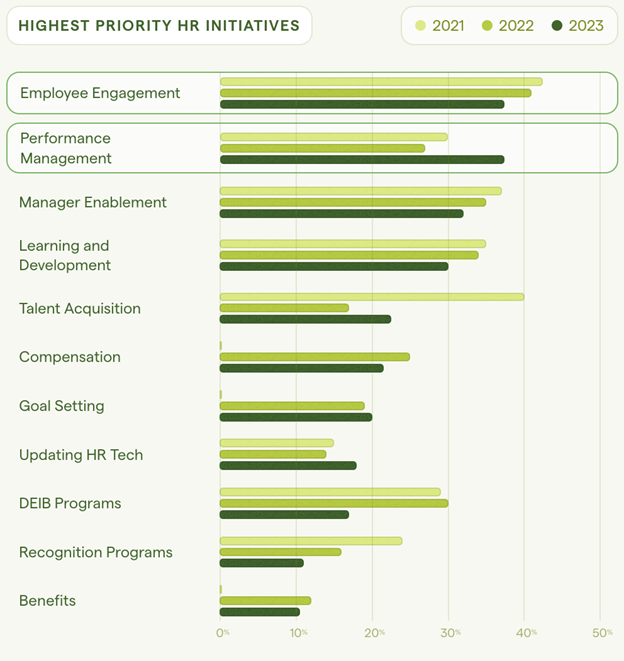

People leaders are shifting to performance and engagement–not recruiting

In Lattice’s State of People Report 2024, there are a ton of insights. Two that stick out are the disconnection between executives and HR leaders, as well as the dramatic shift in priorities.

The big loser in HR priority was recruiting, and the big winner is performance management.

Money is more expensive. Hiring people may be too costly. Layoffs arise. Hard goods are still inflating in price (if less quickly). You have to do more with less. Get creative and unlock your most talented people.

Rising interest rates affect employees too, especially performance and engagement

The pickle here is that employees feel the effects of the changing economy too. It’s suddenly more expensive for them to borrow. And in the past two years, they’ve seen everything from groceries to haircuts get a lot more expensive from inflation. Their purchasing power has declined, and they can afford less.

While purchasing power has a normal decline with moderate inflation, the declined accelerated.

From January 2013 to January of 2021, the purchasing power dropped more than 5 points from 43.4 to 38.2. But as COVID supply chain inflation combined with oil inflation, the purchasing power dropped to 31.8 in June of 2024, that’s a 6.4 point drop and almost tripling the rate of change.

These may seem like abstract numbers, but they have real consequences. Financial worries have big effects on people’s mental health.

A group of researchers studied the relationship between financial stress and mental health and came to the conclusion you would expect: “The hierarchical regression analysis revealed that higher financial worries were significantly associated with higher psychological distress.” - The Relationship between Financial Distress and Psychological Health by Soomin Ryu and Lu Fan.

And this puts people leaders in a pickle. You are currently being charged with getting more out of your same team. You don’t have the budget to give financial rewards and raises. And at the same time, all of your team is feeling greater financial stress.

It’s a double-whammy.

What are you to do?

Ideally, you can just give regular COL salary increases. But unless your company has the term AI in the title, that’s probably not happening.

However, constraints can unlock creativity. And there’s plenty you can do. Here’s one of them:

Retirement plans provide a hidden lever for people leaders

Your retirement plan is hidden in plain sight.

It’s an expense the company has already baked in and is not going to cut. So how can you optimize it for your employees? How can you use it to better understand the financial needs of your team?

Help your executive team “read the tea leaves” on the economy. Your Investment Committee meets regularly to discuss high level macro-economic trends. They produce valuable research and opinions that can give your leadership team additional context for when these cycles might stabilize or change.

For you as the HR leader, a retirement plan has data that can correlate with how stressed your employees are truly feeling. So look at their contribution rates, is it enough for them to retire on (typically 10-15% is the rule of thumb)? Is the contribution rate going down? Are there more loans being taken out? These are signals that your employees are struggling.

This can be helpful both for seeing macro level trends as significant drops in deferral and contribution rates can be an early indicator that you might see key folks getting ready to leave for economic reasons. And on the micro level, changes in individual behavior can be a good cue to have a check in and with those key, “can’t lose” employees to get ahead of any major financial issues.

Help your employees build better financial frameworks and habits to manage financial stress. And providing investments summaries may provide helpful context for the overall company decisions as well as how they may want to save and invest.

You have to be delicate with this, as it’s not a fool proof replacement for the gap in pay they may need, but having a plan and a system can build back a sense of control. The silver lining for times of belt tightening is that it can put us back in touch with what we actually want and care about for our money. Even with plenty of income, having that sense of what “enough” is materially can be a great psychological booster.

If your retirement plan has an investment advisor, and they are not already doing this, then ask them to. It’s a great perk that should be part of the services an investment advisor provides. If not, look for a new advisor - and because an advisor is generally paid out of employee fees, this would not impact your company budget.

If you do have a little budget there are some ways that compensation dollars can be stretched a little further if given through a profit share into a 401(k) plan, but that’s another article.

Overall, this is a challenging time for people leaders. But challenge breeds creativity. And one creative place you may not be looking at optimizing is your retirement plan. You likely can squeeze even more value from it for your team.

Latest articles

This data feed is not available at this time.

Data is currently not available