The U.S. tariff announcement after market-close on April 2nd resulted in deep equity declines over the ensuing two trading days. The Nasdaq-100 Index® (NDX®) experienced losses of -11.5% (worst 2-day decline since 2007) and the S&P 500 Index dropped -10.8% (worst 2-day decline since 1960). Volatility was on full display as equity volatility, as measured by the VIX, more than doubled and closed at 52.3 on April 8th, its highest level since March 31, 2020. Then, on April 9th, after the U.S. announced a 90-day pause on higher reciprocal tariffs for everyone except China, the NDX jumped 12% (second best day since 2007) and the S&P 500 Index gained 9.5% (third largest gain since 1933).

These extreme market swings and volatility in global asset owner and consultant reactions were captured via Nasdaq eVestment™ Analytics profile reviews of asset managers’ products, which showed peaking interest in several strategies as they hit, or held, 52-week highs in research activity.

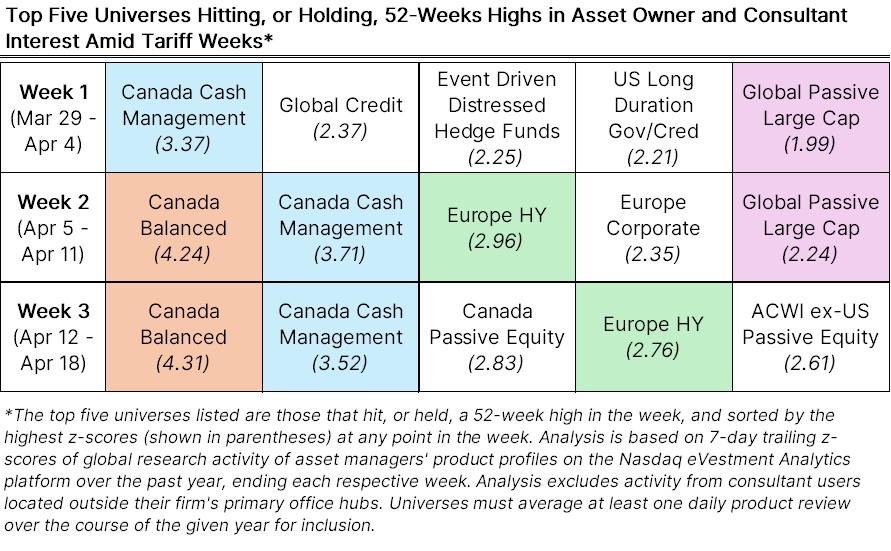

At the end of tariff Week 1, several strategies experienced unusual surges in profile reviews from global asset owners and consultants using the Nasdaq eVestment platform. Profile reviews, or views, of asset managers’ products indicate that allocators and intermediaries are actively investigating these strategies and are direct evidence of interest.

Canada Cash Management strategies (total AUM of US$ 17bn as of Q4’24) saw their viewership activity rise 3.4 standard deviations above their typical mean activity over the past year and Global Credit strategies (US$ 359.7bn) recorded a z-score spike of 2.4 – both figures calculated using 7-day trailing data. This was the first time Canada Cash Management surpassed two standard deviations since February 6th, shortly after the U.S. announced 25% tariffs on non-energy imports from Canada. Outside of the preceding week, it was also the first time Global Credit exceeded two standard deviations since September 1, 2024. And contrary to equity market declines, the Bloomberg Global Aggregate Corporate Index was slightly positive for the week ended April 4th—though it proceeded to decline notably the following week.

After the end of tariff Week 1, U.S. reciprocal tariffs paused for all countries but China, U.S. Treasury 10-year yields spiked to mid-February levels, and gyrations in FX markets led to a notable USD depreciation, and plenty more. Elevated levels of volatility and uncertainty continued heading into the second week.

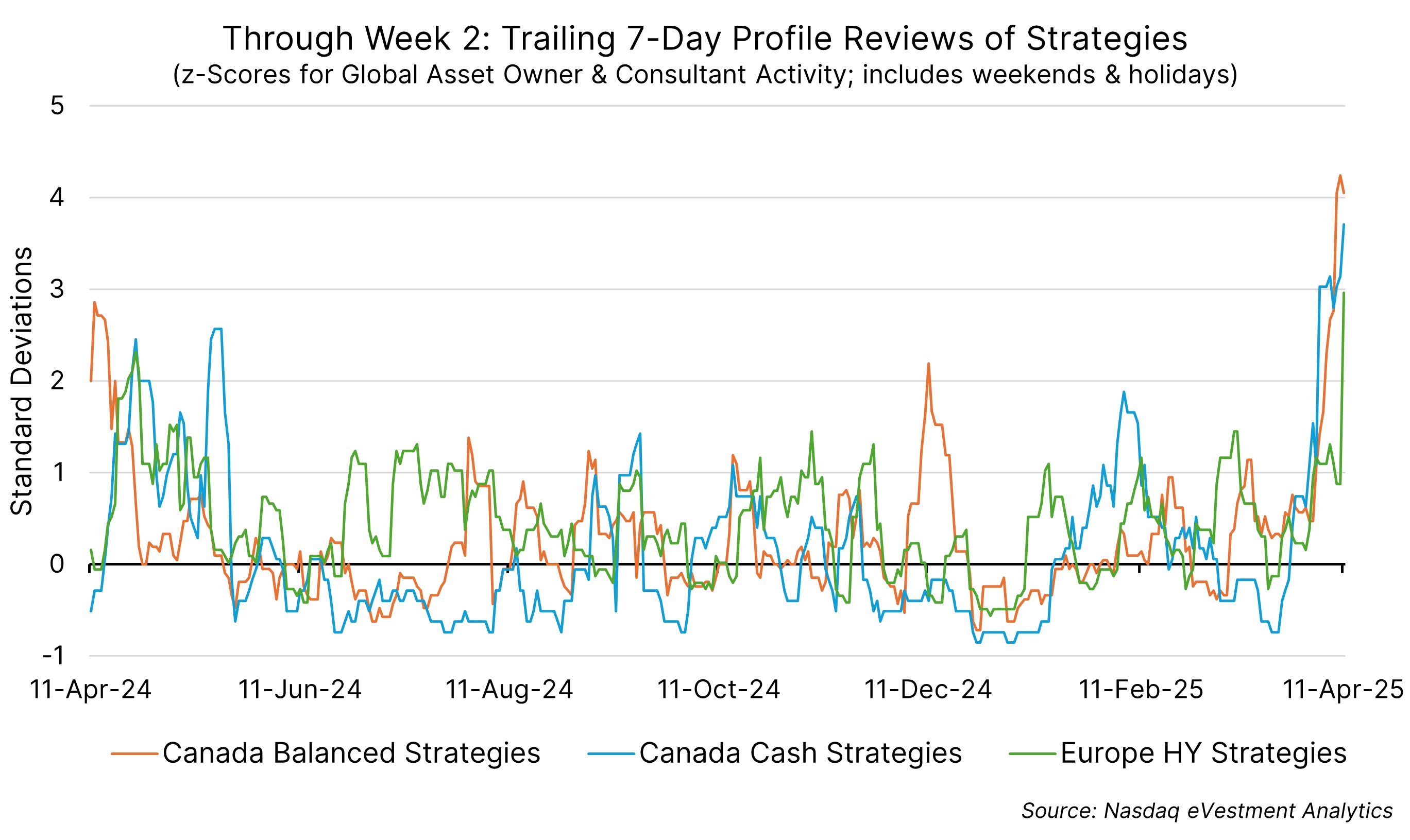

In Week 2 ending on April 11th, the CAD appreciated 2.15% against the USD and allocator and consultant viewership of Canada Cash Management strategies continued reaching new highs. Institutional interest in Europe High Yield (US$ 87.6bn) products reached its highest level over the past year, coinciding at a time when the effective yield of the ICE BofA Euro HY Index reached its highest level (6.31%) in nearly a year as well (6.32% on April 25, 2024). But a significant spike exceeding four standard deviations for Canada Balanced (US$ 58.5bn) strategies emerged – driven primarily by U.S.-based consultant activity. This may suggest increased appeal for multi-asset exposure to the Canadian market via new manager searches, or may reflect typical consultant activities such as manager due diligence.

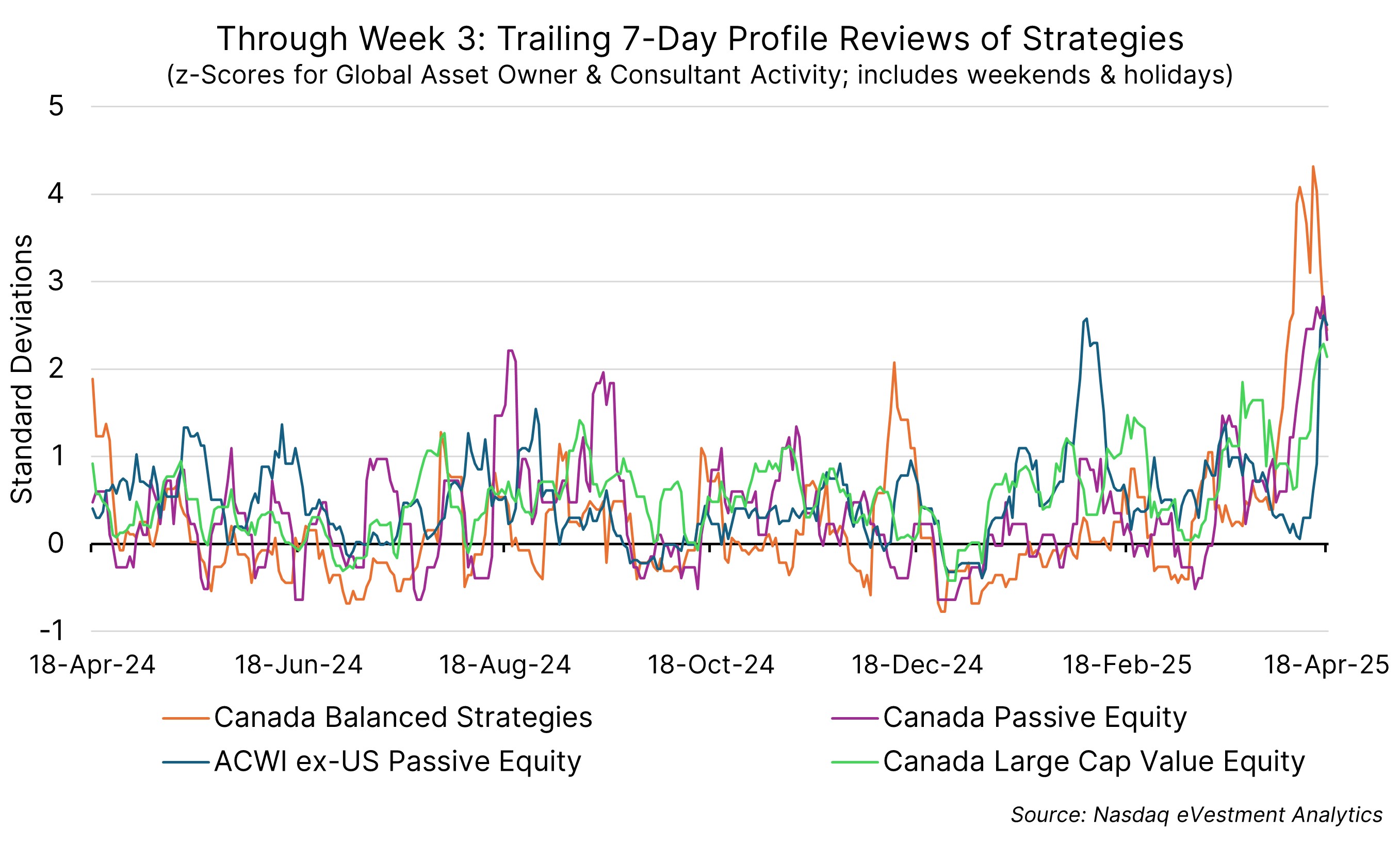

Starting in Week 2 and continuing into Week 3, Canadian equities (S&P/TSX) outperformed U.S. equities (S&P 500) by 7.1% over the five trading days ending on April 16th in USD terms. This was the largest five-day relative outperformance since March 25, 2020, as U.S. equities sold off on April 16th following comments from Federal Reserve Chair Jay Powell, when he emphasized the need to prevent tariffs from causing rising inflation and that the Fed is not in a hurry to lower rates. Additionally, the USD continued to sell-off vs. the CAD amidst a broader USD weakening given trade tariff and policy concerns, along with potential asset reallocations regionally.

Both active and passive Canada-focused strategies experienced increased research activity from asset owners and consultants in Week 3. Canada Passive Equity (US$ 36.2bn) interest was driven by domestic consulting firms, while interest in Canada Large Cap Value (US$ 44.2bn) strategies came from mostly domestic public pensions, corporate pensions, insurance, consulting, and manager of manager firms. ACWI ex-US Passive Equity (US$ 967.4 bn) also saw a notable increase at a time when the “sell America” trade was gaining momentum and gold was hitting new highs, with all of Week 3’s research activity to these strategies coming from U.S-based consultants and public pensions. YTD through April 22nd, the MSCI ACWI ex-US Index is up 4.4% while MSCI US Index is down -10.3%.

We expect continued market volatility and macro uncertainties across global markets in the coming weeks and months. Nasdaq eVestment is uniquely positioned to provide insights on how thousands of asset owners and consultants are reacting to tariff and policy dynamics based on their research activity of institutional asset managers’ product profiles on the Nasdaq eVestment Analytics platform.

Nasdaq®, Nasdaq eVestment™ are trademarks of Nasdaq, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED.

© 2025. Nasdaq, Inc. All Rights Reserved.

Leveraging Nasdaq eVestment for Real-Time Insights

Policy implications on financial markets allow for investors to reevaluate their investments and exposures, both tactically and strategically. Real-time awareness of investor and consultant activity can keep you prepared for fundraising opportunities. Nasdaq eVestment for Asset Managers provides real-time analytics to identify which strategies are garnering interest from allocators and consultants, and from where this activity is coming from. And the Nasdaq eVestment API solution provides users with even more data granularity and flexibility.

Latest articles

This data feed is not available at this time.

Data is currently not available