By Matthew J Bartolini, CFA, Head of SPDR Americas Research

- Up and down the cap spectrum and beyond the shores of the US, value has had a strong start to 2021

- Will this rally continue?

The resurgence of value stocks has been a dominant theme over the past few months, culminating in the largest monthly excess return over growth stocks in February (9% and a two standard deviation event) since 2008[1]. And it hasn’t been just large-cap value that has produced strong above market returns. Up and down the cap spectrum and beyond the shores of the US, value has had a strong start to 2021, as well as over the past four months as the dual headwinds of election and vaccine timeline uncertainty were removed.

Today’s question to the value bulls that have played the part of Charlie Brown over the past decade only to have the market (Lucy) pull the ball away, is whether the rally will continue. Let’s review some data to gauge the strength and pervasiveness of this value rally.

Broad-based rally

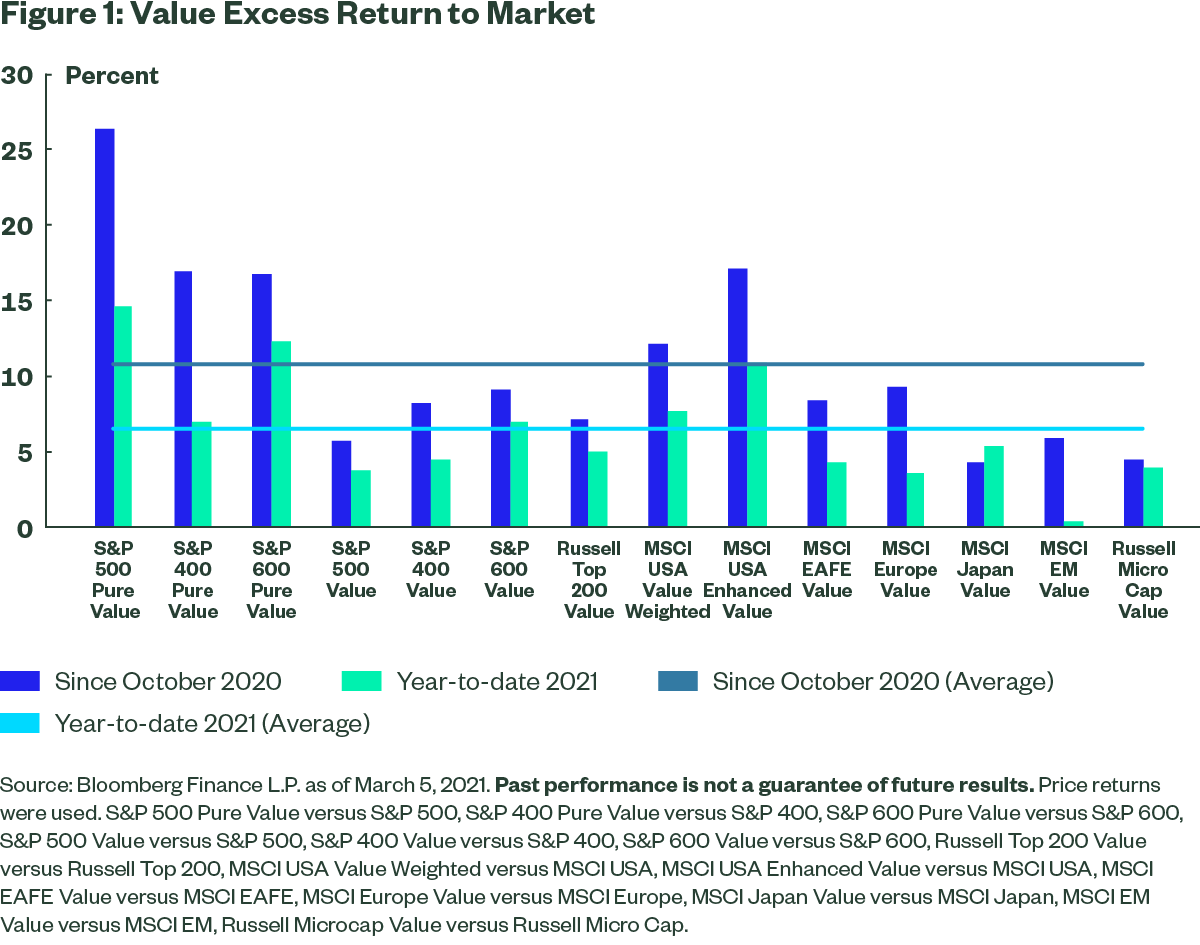

The run-up in value has not been confined to one specific market, or construction philosophy . As shown below, fourteen different value approaches (ranging from sector neutral to small cap to emerging market) have outperformed their respective broad market segments both in 2021 and since the end of October – with the average excess return of 6% and 10%, respectively.

[wce_code id=192]

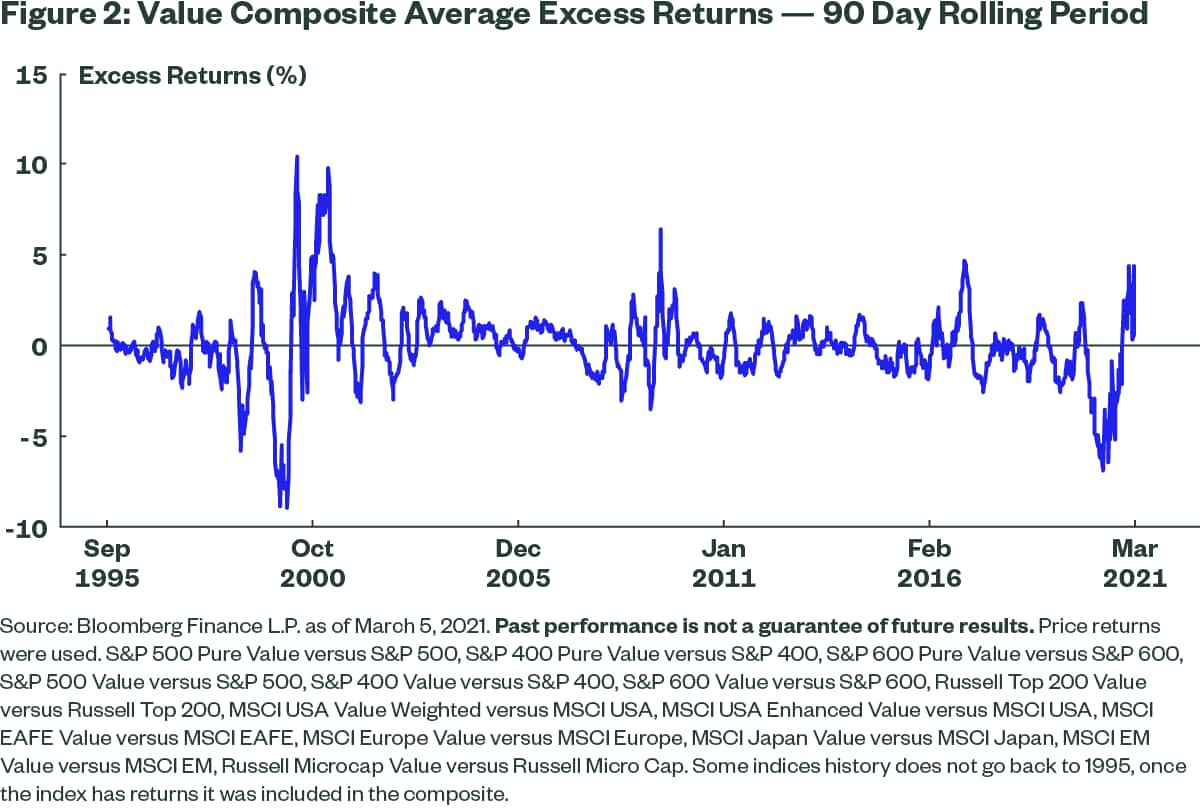

If we apply a composite approach to these fourteen value exposures (creating a portfolio that holds each value strategy at equal weights, rebalanced weekly) and calculate the rolling 90-day average excess market return, the current 4% excess return would be in the historical 97th percentile. And a positive excess return for 16 consecutive weeks underscores the breadth of this current value rally.

Sector effects on the value rally

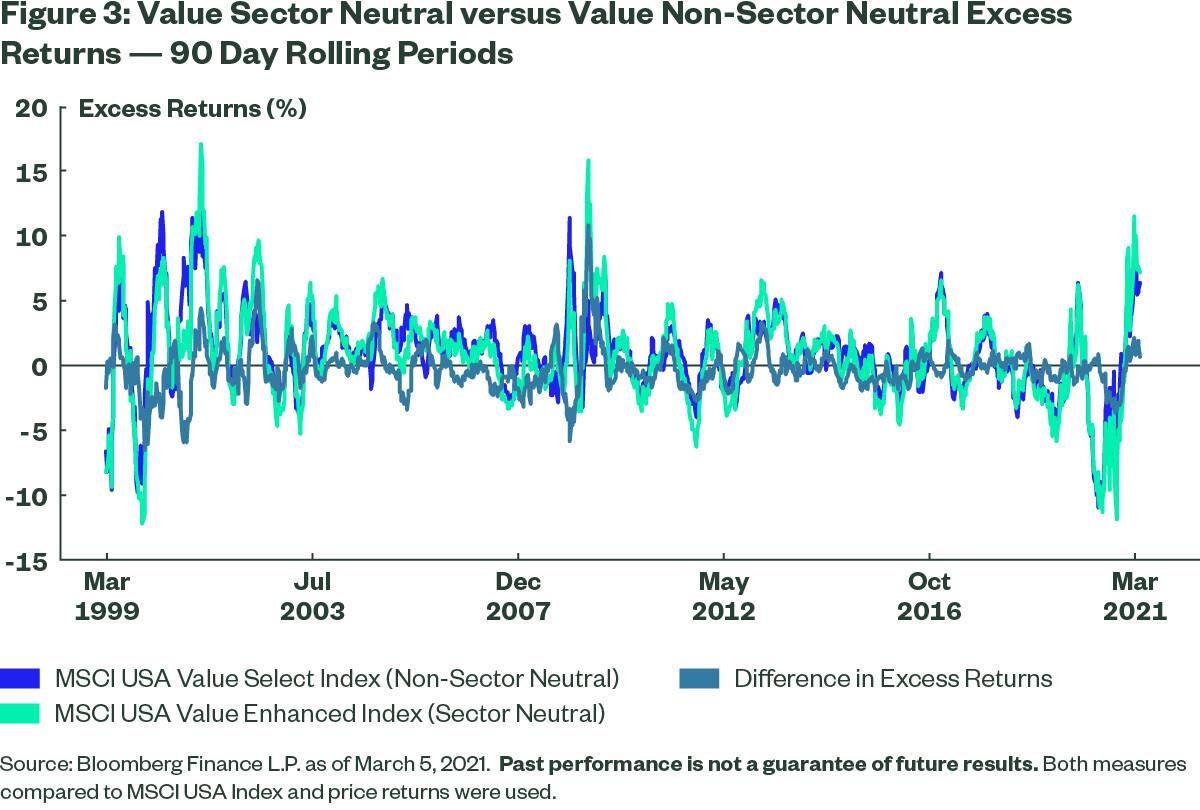

To determine if this value rally is predicated on sector allocations, we can showcase the return of a sector neutral value strategy versus a similarly constructed but non-sector neutral strategy[2]. Both have had strong positive excess returns so far this year, up versus the market by 11% and 7.7%, respectively[3]. Similar to the analysis on the composite approach, the rolling 90-day returns plotted below show both value construction types have had outsized outperformance as of late, with the sector neutral exposure leading. And the sector neutral exposure’s outperformance over the non-neutral benchmark indicates cheaper stocks are outperforming expensive stocks irrespective of the sector they reside in.

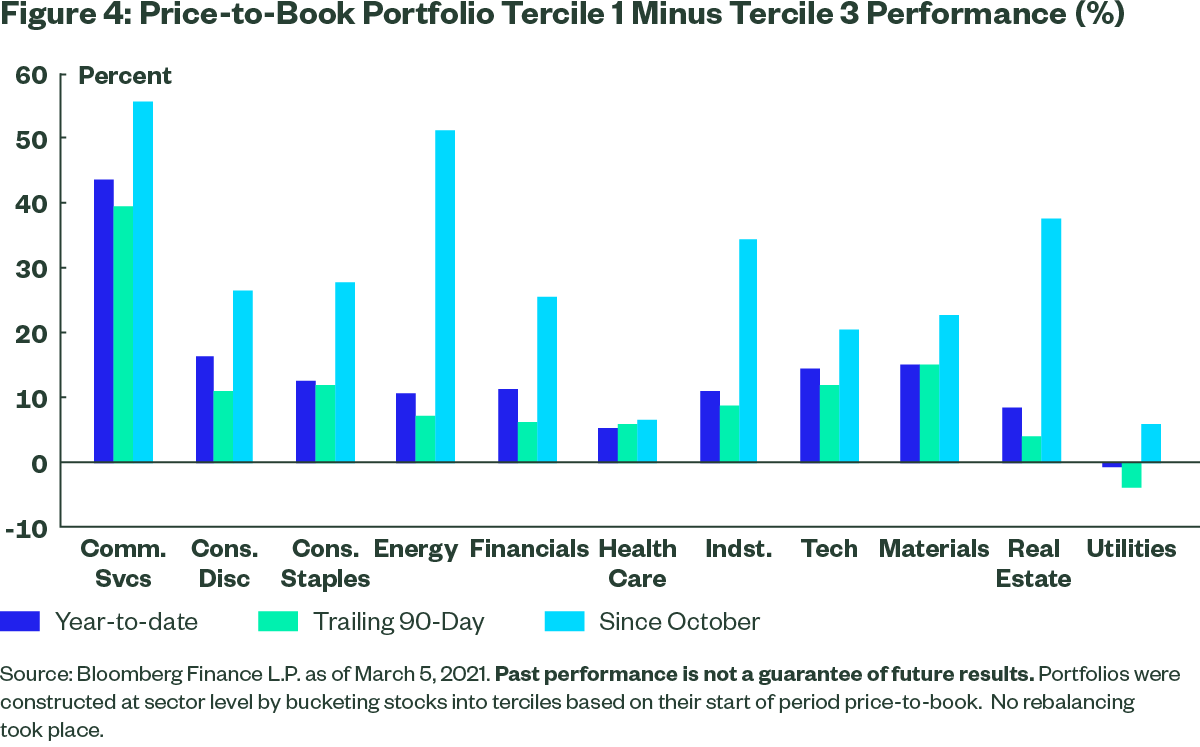

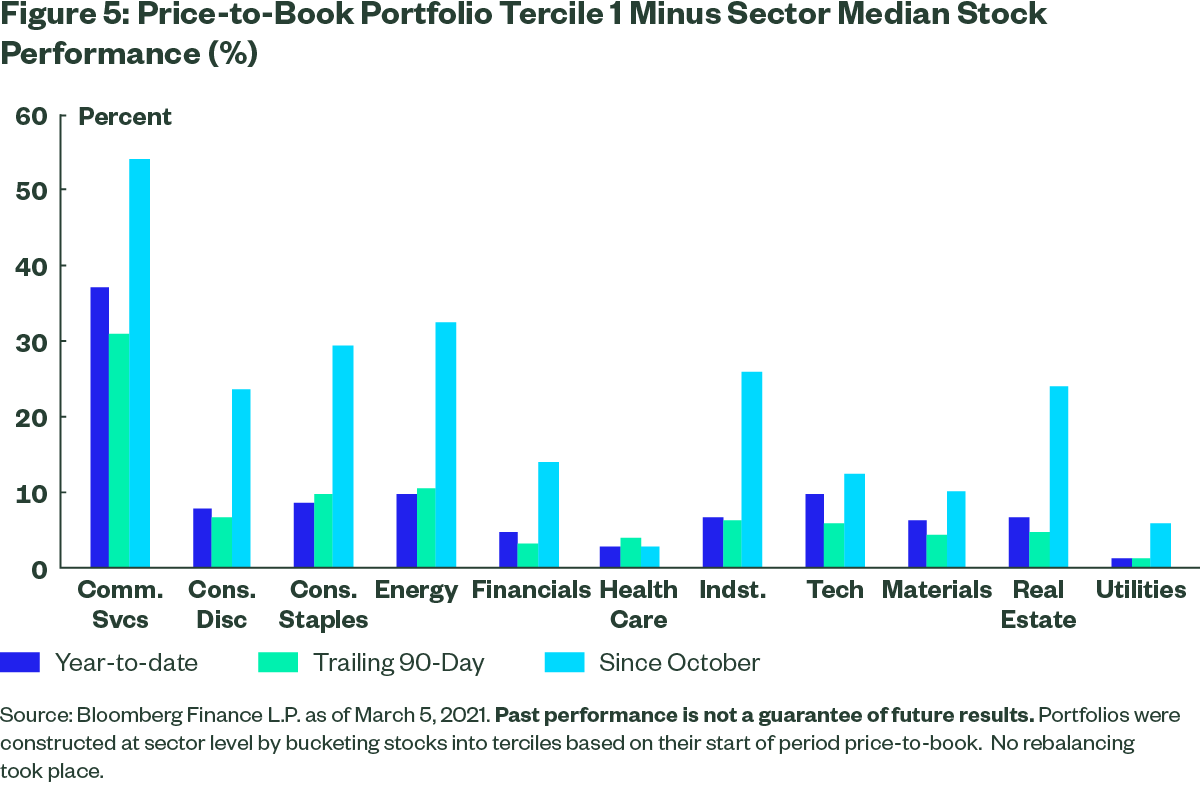

Another way to showcase this is to split each sector into terciles based on a valuation measure. For this example, I used price-to-book. Although this is not the perfect measure, it matches academic research and controls for firms with negative earnings – but is impacted by intangibles. With the Russell 1000 Index as the base universe, the top tercile includes the cheapest stocks with the lowest price-to-book (P/B) and the bottom tercile has the most expensive stocks. (Note that these aren’t growth stocks. Growth is not the absolute inverse of value. These are just high-priced stocks).

Within each tercile, the stocks were equally weighted. The performance of the sector tercile portfolios over the previously mentioned time periods (year-to-date, rolling 90 days, and since the end of October 2020) is shown below. Relative to the median stock return and the high-priced tercile, the “cheap” value stocks in every sector have outperformed since the end of October. Only low P/B stocks in the Utilities sector have recently underperformed the median and high-priced third tercile. Overall, however, the performance favors tercile one (low P/B or “cheap” stocks), further reinforcing how pervasive the value rally has been.

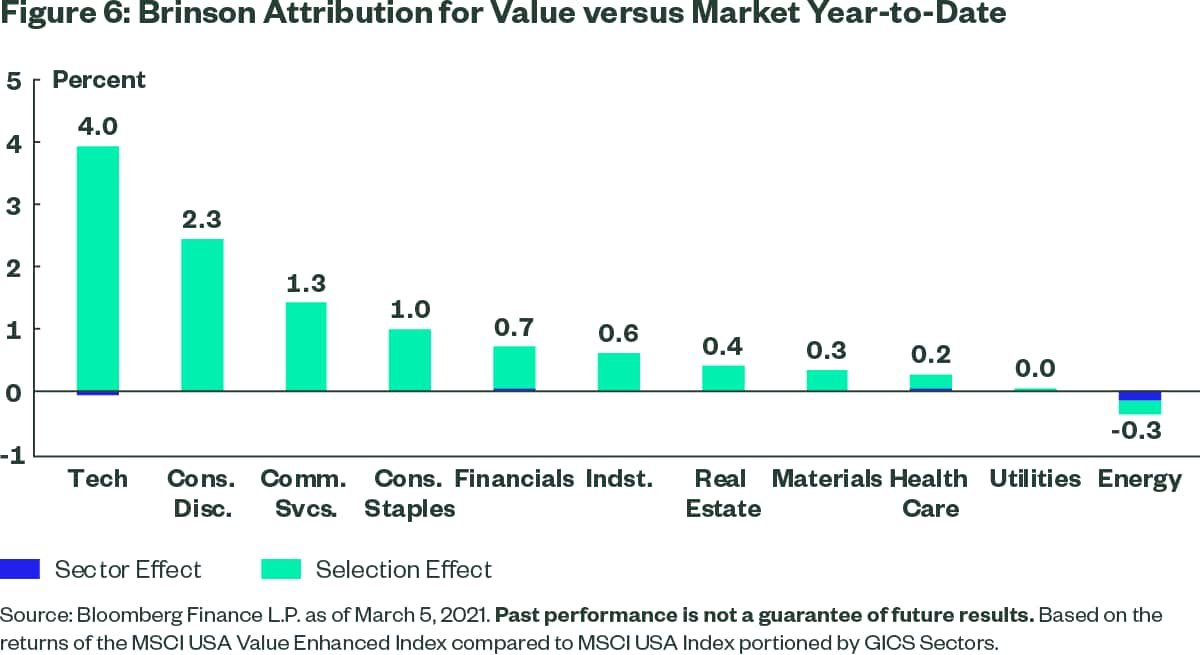

Performing Brinson attribution[4] of a value exposure to the broader market can also show whether sector effects or selection effects drove returns. The attribution for a sector neutral value versus the broader market is shown below, and more than 100% of the 11% outperformance by value so far this year is driven by selection effect – indicating the portfolio that targets cheap stocks and weights them accordingly drove the returns.

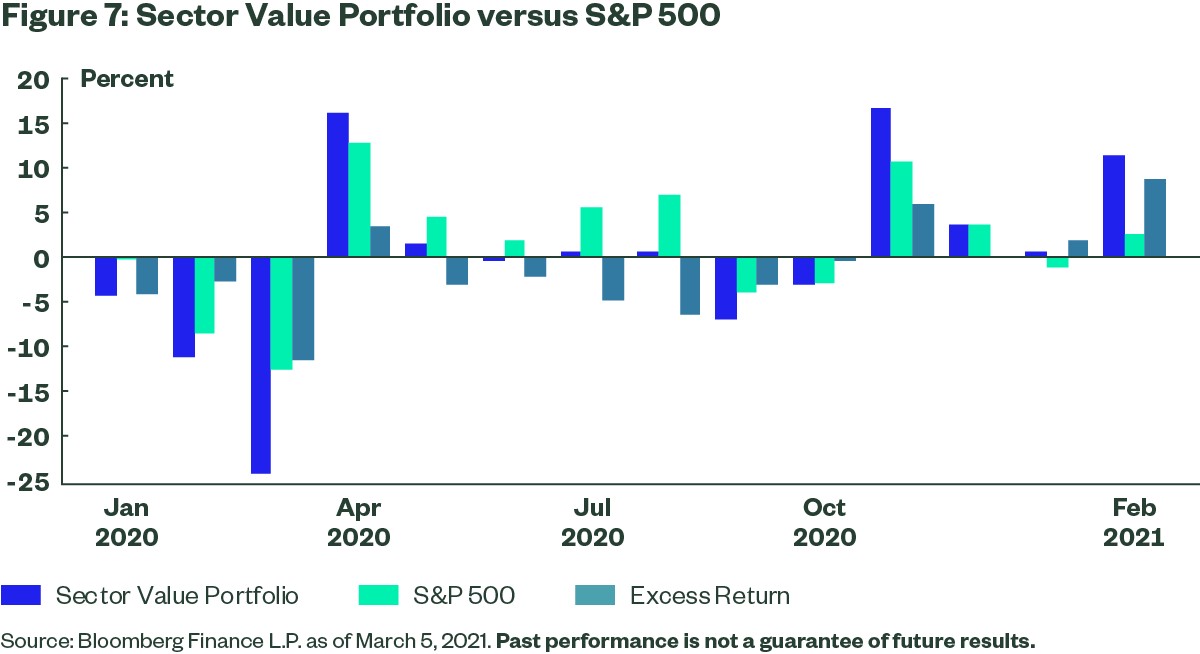

This is not to say, however, that sector effects are not playing a role. Rather, the returns illustrate a depth to the value rally that is not confined to the strong performance of sector XYZ. Yet, owning just cheap sectors has also produced strong returns. If we were to create a value sector portfolio by ranking each sector across four[5] valuation metrics[6] – as we highlight in our monthly chart pack – and equal weight the cheapest three sectors to create a single portfolio (rebalanced monthly)[7] , this portfolio would also show strong excess returns relative to the market. It would have outperformed the market in each of the past four months. This further strengthens the notion that cheap stuff has really rallied as of late, no matter the value construction approach.

Ok but why now?

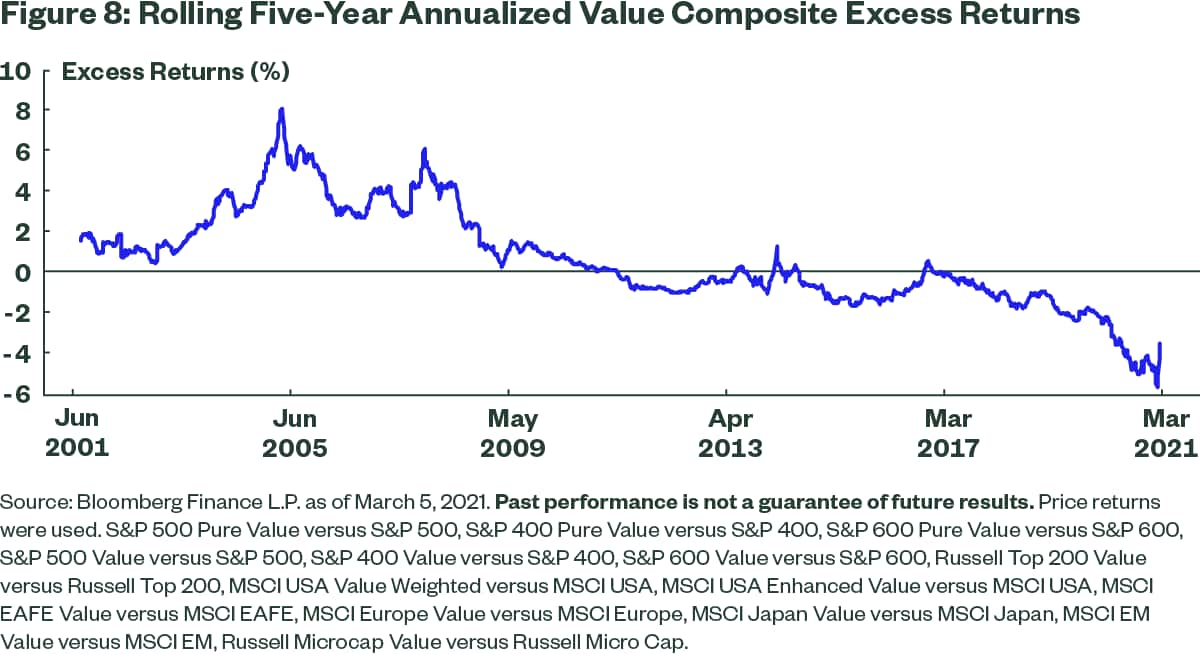

Value investors have played the roles of Vladimir and Estragon over the past decade, waiting for value (Godot) to return. In fact, on a rolling five-year basis for the composite of all fourteen value exposures discussed earlier, the composite had positive rolling return in only 9% of the time period observations over the past decade – and none since 2016, as shown below. It has been a tough ride to say the least.

Value’s continued resurgence is predicated upon two main variables:

- A reflating of the economy, benefiting rate sensitive equites – correlation and beta profile (55%/ 0.30) to rates is higher than both the market and growth disciplines (34%/0.12 and 27%/0.11, respectively)[8]

- Above market growth, plus attractive valuations at a time of stretched metrics elsewhere – Earnings-per-share growth (25%) is above that of growth styles (20%) and the market (24%). And relative valuations for S&P 500 value stocks are in the bottom decile across Price-to-Next-Twelve-Month-Earnings Ratio, Price-to-Book Ratio, and Price-to-Sales Ratio compared to top decile for S&P 500 growth stocks.[9]

With both macro variables likely to persist amid this renewed higher reflationary rate regime, the value rally may have more room to run. Not to mention, value stocks are starting to exhibit strong price return momentum. A simple sort of the top 100 S&P 500 stocks based on 12-1 momentum[10] screen now has 9% overlap at the end of February to the highly concentrated S&P 500 Pure Value Index,[11] up from 3% at the start of the year. A more intermediate momentum score of 6-1 leads to higher overlap, currently 40% versus 18% at the start of the year.

Overall the value rally has been strong and broad-based, no matter the definition. If this rally does continue, investor positioning toward these more rate sensitive equities may provide strong above market returns while at the same time mitigating the effects of the rate reflationary regime shift on broadly allocated portfolios.

Originally published by State Street, 3/10/21

1 Based on the returns of the S&P 500 Pure Value Index and the S&P 500 Index based on data from 1995 per Bloomberg Finance L.P. as of February 28, 2021

2 There are other differences in construction in terms of the descriptors used that can lead to deviations beyond sector effects, but sectors do have a meaningful impact on the differences in active risk

3 Based on the returns of the MSCI USA Value Select Index (non-sector neutral) and the MSCI USA Value Enhanced Index

4 Brinson attribution refers to performance attribution based on active weights. There are different variations, but the effects usually include allocation, security selection, currency, and potentially others.

5 Price-to-Book, Price-to-Sales, Price-to-Earnings, and Price-to-Next-Twelve-Month Earnings

6 In earlier analysis we used one metric as we are comparing intra-sector so we are comparing against like stocks that may be impacted by some of the valuation metrics shortcomings in a similar way (i.e. P/B to tech stocks would understate intangibles of tech firms, but it is done equally). For comparing across sectors where certain valuation metrics may provide corner results due to biases (e.g., intangibles) a composite approach is more robust.

7 For simplicity used end of month rebalancing even though that introduces timing luck.

8 Bloomberg Finance L.P. as of February 26, 2021 based on the monthly returns of the S&P 500 Pure Value Index, S&P 500 Pure Growth Index, and S&P 500 Index versus the US 10 Year Yield from 2/2016 to 2/2021

9 FactSet as of February 26, 2021 Price-to-Next-Twelve-Month-Earnings Ratio, Price-to-Book Ratio, and Price-to-Sales Ratio for S&P 500 Value Stocks are below the 10th percentile relative to the S&P 500 over the past 15 years

11 Most recent 12 months return minus the most recent month

12 Approximately 120 holdings

13 Most recent six month return minus the most recent month

The views expressed in this material are the views of SPDR Americas Research Team and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The information provided does not constituteinvestment adviceand it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All material has been obtained from sources believed to be reliable. There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information.

All the index performance results referred to are provided exclusively for comparison purposes only. It should not be assumed that they represent the performance of any particular investment.

Passively managed funds hold a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. Passively managed funds invest by sampling the index, holding a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. This may cause the fund to experience tracking errors relative to performance of the index.

Actively managed funds do not seek to replicate the performance of a specified index. The strategy is actively managed and may underperform its benchmarks. An investment in the strategy is not appropriate for all investors and is not intended to be a complete investment program. Investing in the strategy involves risks, including the risk that investors may receive little or no return on the investment or that investors may lose part or even all of the investment.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions.

Volatility management techniques may result in periods of loss and underperformance may limit the Fund's ability to participate in rising markets and may increase transaction costs.

A momentum style of investing emphasizes securities that have had higher recent price performance compared to other securities, which is subject to the risk that these securities may be more volatile and can turn quickly and cause significant variation from other types of investments.

Investments in small-sized companies may involve greater risks than in those of larger, better known companies.

Companies with large market capitalizations go in and out of favor based on market and economic conditions. Larger companies tend to be less volatile than companies with smaller market capitalizations. In exchange for this potentially lower risk, the value of the security may not rise as much as companies with smaller market capitalizations.

Value stocks can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time.

Because of their narrow focus, sector funds tend to be more volatile.

Read more on ETFtrends.com.The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.