Despite positive share price growth of 18% for WVS Financial Corp. (NASDAQ:WVFC) over the last few years, earnings growth has been disappointing, which suggests something is amiss. Some of these issues will occupy shareholders' minds as the AGM rolls around on 26 October 2021. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. In our analysis below, we show why shareholders may consider holding off a raise for the CEO's compensation until company performance improves.

Comparing WVS Financial Corp.'s CEO Compensation With the industry

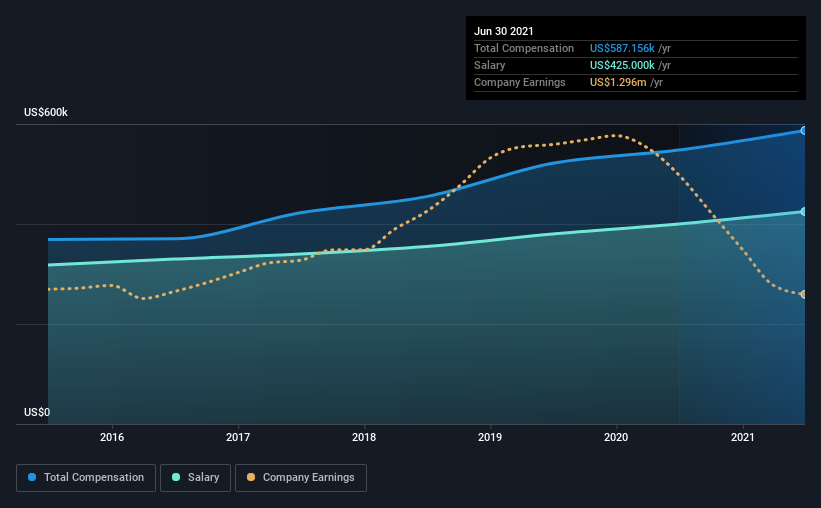

According to our data, WVS Financial Corp. has a market capitalization of US$27m, and paid its CEO total annual compensation worth US$587k over the year to June 2021. That's just a smallish increase of 7.2% on last year. We note that the salary portion, which stands at US$425.0k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the industry with market capitalizations below US$200m, we found that the median total CEO compensation was US$534k. From this we gather that Dave Bursic is paid around the median for CEOs in the industry. Furthermore, Dave Bursic directly owns US$3.3m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | US$425k | US$400k | 72% |

| Other | US$162k | US$148k | 28% |

| Total Compensation | US$587k | US$548k | 100% |

Talking in terms of the industry, salary represented approximately 51% of total compensation out of all the companies we analyzed, while other remuneration made up 49% of the pie. WVS Financial is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

WVS Financial Corp.'s Growth

WVS Financial Corp. has reduced its earnings per share by 14% a year over the last three years. Its revenue is down 22% over the previous year.

The decline in EPS is a bit concerning. This is compounded by the fact revenue is actually down on last year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has WVS Financial Corp. Been A Good Investment?

With a total shareholder return of 18% over three years, WVS Financial Corp. shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

Despite the positive returns on shareholders' investments, the fact that earnings have failed to grow makes us skeptical about whether these returns will continue. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 3 warning signs for WVS Financial that investors should think about before committing capital to this stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.