As PayPal Holdings PYPL prepares to announce its Q3 2025 earnings, all eyes will be on the company’s transaction revenues, which form the backbone of PayPal’s business model. Transaction revenues come primarily from fees charged to merchants and consumers on payments processed through PayPal's platforms. These fees are based on the Total Payment Volume processed by the company.

Transaction revenues accounted for approximately 90% of its total revenues in the second quarter of 2025. In this quarter, PayPal reported transaction revenues of $7.44 billion, up 4% year over year.

Looking ahead to the third quarter of 2025, expectations are optimistic for another quarter of solid transaction revenue growth. This optimism is driven by a few key factors. Firstly, management expects an increase in transaction margin dollars between 3% and 5% in the third quarter of 2025. Secondly, PayPal is actively working to enhance its payment ecosystem and introduce new features. Lastly, the growing popularity of Venmo as a peer-to-peer platform, along with its increasing merchant transactions, continues to contribute meaningfully to transaction revenues.

The Zacks Consensus Estimate for its third quarter transaction revenues is pinned at $7.45 billion, indicating a rise from $7.07 billion in the prior-year quarter. Investors will be keen to know how much transaction revenues are reported in the third quarter, when the company announces results on Oct. 28.

PayPal’s business closely follows overall digital commerce trends. The continued rise in online shopping and mobile payments will help boost transaction volume, leading to better third-quarter results.

How Are Block & Payoneer Earning Their Transaction Revenues.

Block’s XYZ transaction revenues in Q2 2025 were $1.82 billion, up 6.1% YoY and representing 30% of its net revenues. XYZ earns most of its transaction revenue from Square by charging merchant fees for payment processing. Cash App also plays big role, earning from peer-to-peer payments, Bitcoin trading and other financial services.

Payoneer Global’s PAYO Q2 2025 total revenue was $261 million, up 9% YoY, with revenue excluding interest income growing 16% YoY. The increase in transaction volume and improved customer take rates were important for this growth. PAYO generates transaction revenue by charging fees on cross-border payments, currency conversions and fund withdrawals.

PYPL’s Price Performance, Valuation & Estimates

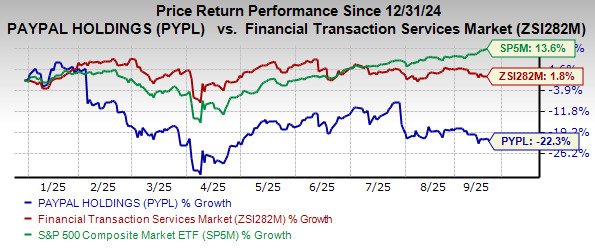

Shares of PayPal have declined 22.3% year to date, underperforming both the broader industry and the S&P 500 Index.

Image Source: Zacks Investment Research

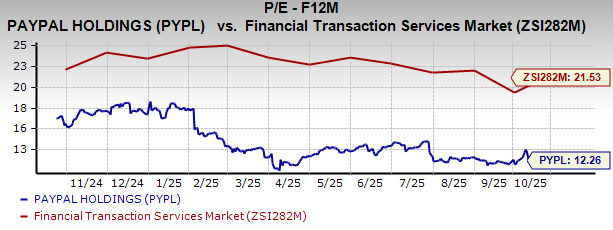

From a valuation standpoint, PayPal shares are trading cheaply, as suggested by the Value Score of A. In terms of forward 12-month P/E, PYPL stock is trading at 12.26X, which is at a significant discount to the Zacks Financial Transaction Services industry’s 21.53X.

Image Source: Zacks Investment Research

PayPal’s estimate revisions reflect a positive trend. The Zacks Consensus Estimate for full-year 2025 EPS has been revised upward over the past week. The Zacks Consensus Estimate for 2025 EPS suggests 12.5% growth year over year.

Image Source: Zacks Investment Research

PayPal currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>PayPal Holdings, Inc. (PYPL) : Free Stock Analysis Report

Payoneer Global Inc. (PAYO) : Free Stock Analysis Report

Block, Inc. (XYZ) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.