Hayden Capital commentary for the first quarter ended March 31, 2022.

Dear Partners and Friends,

The last six months have been extremely painful – by far, the worst period since we started Hayden. There’s a lot to worry about – the highest inflation rates in decades, an aggressive US central bank that’s rapidly increasing interest rates, and Russia’s invasion of Ukraine shaping geopolitical dynamics for the next decade.

Q1 2022 hedge fund letters, conferences and more

This macro uncertainty, combined with rapidly rising interest rate expectations have had a dramatic impact on the market valuations of our portfolio companies, along with the rest of the ecommerce, fintech, gaming, consumer internet and emerging markets sectors we operate in more broadly.

To illustrate the carnage out there, the Hang Seng Tech index (which tracks the largest technology companies listed in Hong Kong) is down -65% since its peak last year. Ecommerce stocks (as measured by the ProShares Online Retail ETF) are down -62%, and Fintech stocks (as measured by the Global X FinTech ETF) are down -56%. Looking at the NASDAQ, over 50% of the index companies are now down more than -50% from their highs. Even Amazon, a blue-chip of the tech universe is down over -40% from its highs last year.

This isn’t a normal draw-down in our sector. The markets are already trading similarly to what we saw in 2001 and 2008… the amount of fear that’s out there is chilling.

As another example of the craziness out there, you can even find growing, profitable companies, trading below net cash (see HUYA at a negative -$800M valuation, although there are plenty of other examples) in the Chinese Internet sector. You don’t see these types of extreme situations in healthy markets.

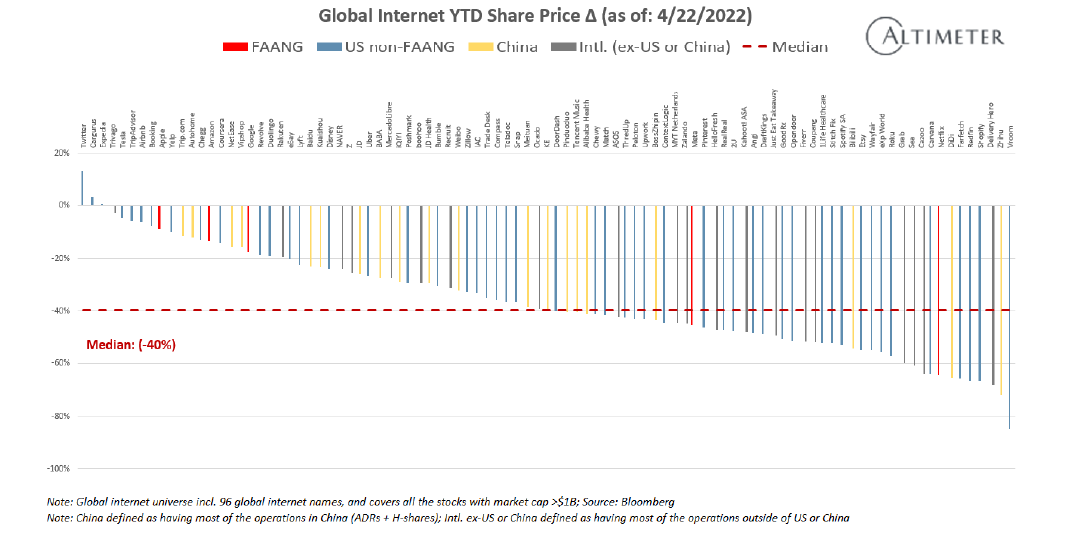

I thought the below graphic from my friend Freda at Altimeter illustrated the situation well. As of April 22, the median internet stock was down ~-40% YTD alone.

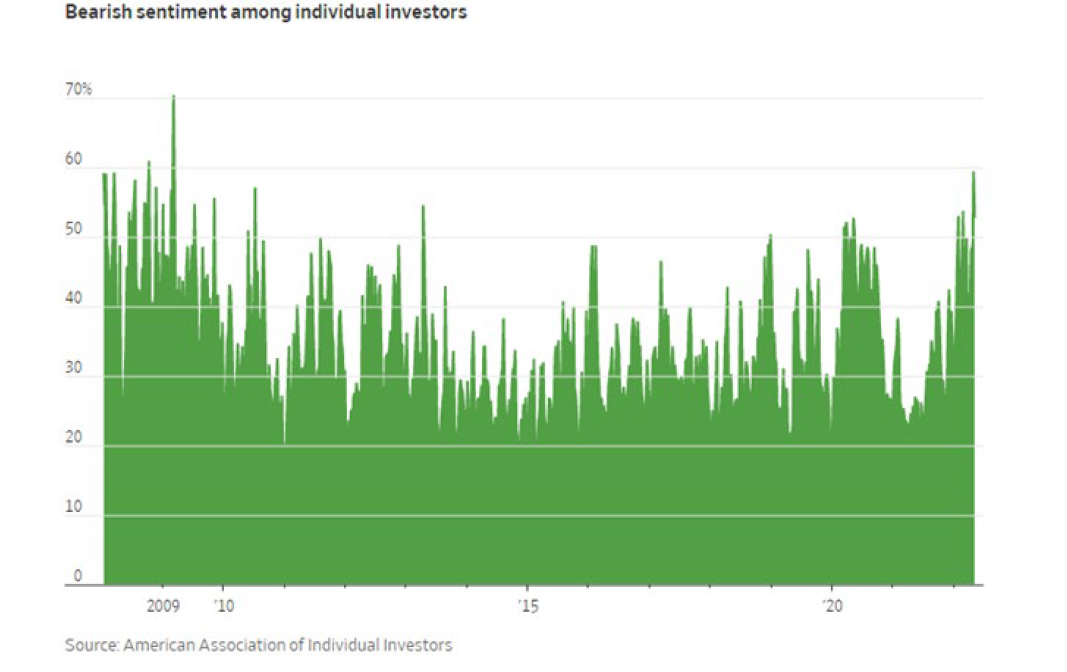

In addition, the American Association of Individual Investors (AAII) survey indicates ~60% of investors believe the stock market will fall in the next six months – levels not seen since March 2009 in the depths of the financial crisis.

Note, these statistics don’t mean that the markets will turn around quickly. But I mention it, as it does tell us where we are today, and state of the market’s mood.

When the markets are full of pessimism, usually that’s a buy signal for long term investors. But there’s certainly the possibility of even more pain in the short term, so the question becomes “when” to buy and how to tell the difference between stocks that will be permanently value impaired in this downturn, versus those whose fundamental trajectories are unaffected and their share prices should rebound quickly after sentiment improves.

Personally, I’ve been surprised by the speed and magnitude of the draw-down, especially considering many of the companies in our universe are even trading below their valuations prior to Covid.

This is in contrast to their fundamentals, which have only gotten stronger and have grown 2 - 3x from their levels two years ago. The pandemic helped provide “free” customer acquisition as customers were stuck at home and looked for new online alternatives (see our Q1 2020 letter, where I talked about this dynamic in the early days of Covid; LINK).

The recent share price round-trip would make sense if these customers were returning back to their old habits – but that isn’t happening. In fact, these customers have proven to be sticky, and the companies themselves are expecting to grow by 20 - 40% annually on top of their “Covid gains”, despite Covid restrictions ending.

It’s been a difficult period, and the markets are trading more on macro-factors than company fundamentals these days. It’s impossible to call a bottom in the short-term, especially as daily moves are seemingly dictated by narratives. And as long as there’s negative headlines and Fed officials keep increasing their hawkish tones, the markets and our portfolio will continue to be extremely volatile in the short-term. In the near-term, stock prices can trade anywhere – it simply depends on at what price the last marginal seller is willing to part ways with their shares.

But if we look out a few years from now, I believe we’ll look back to this time period and recognize just how cheap these companies were trading at, and how much certain companies’ valuations had over-shot to the downside. In markets like these where it seems most investors have a hard time looking out more than 3 weeks, those who have the ability to look out even 3 years will likely be rewarded.

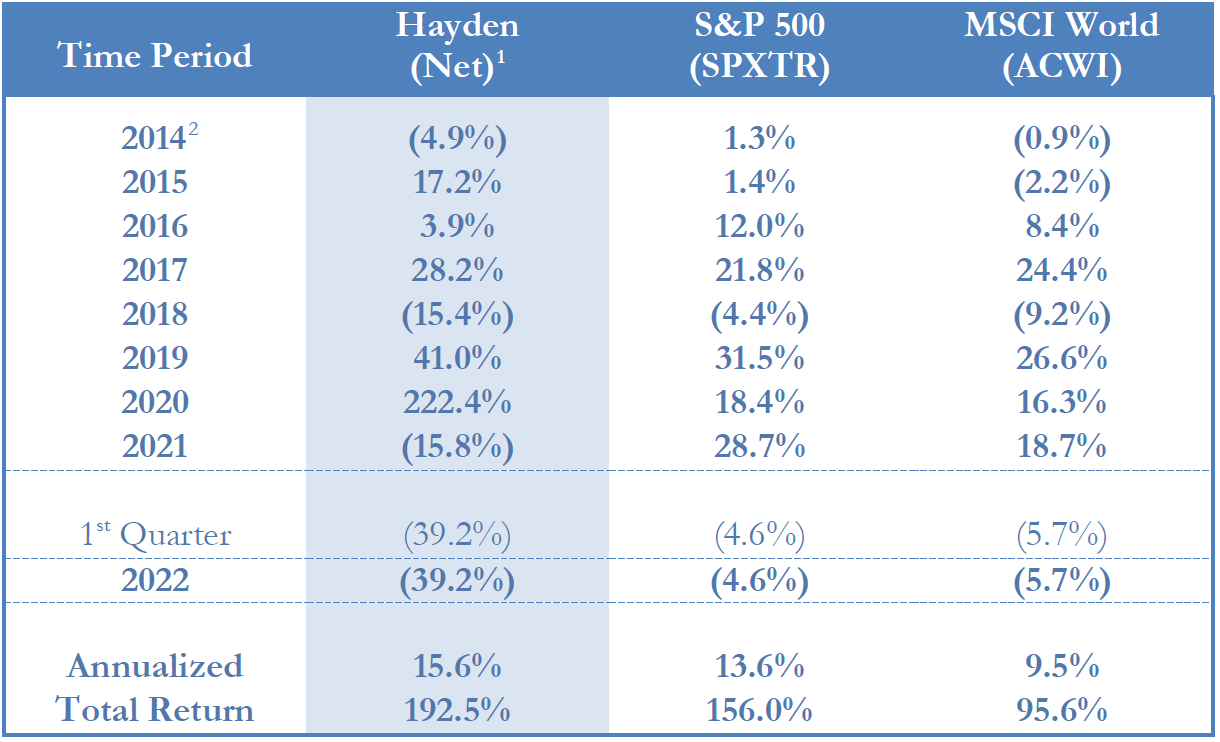

During the first quarter of 2021, our portfolio declined by -39.2%. This compares to the S&P 500’s -4.6% and the MSCI World’s -5.7% first quarter return. We have generated a +15.6% annualized return for our partners, since our portfolio’s inception.

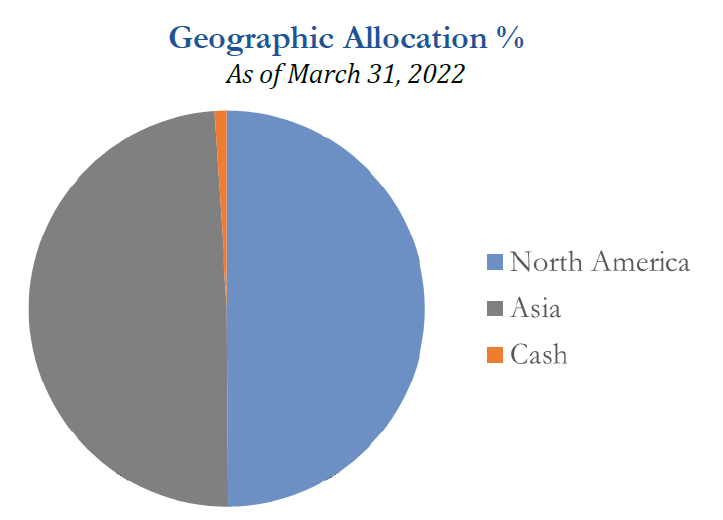

Meanwhile, our portfolio ended the year with ~49% of our assets invested in Asia and ~50% in North America, with the remainder in cash. Our Australian position was acquired in Q1 2022.

- Anatomy of a Bear Market

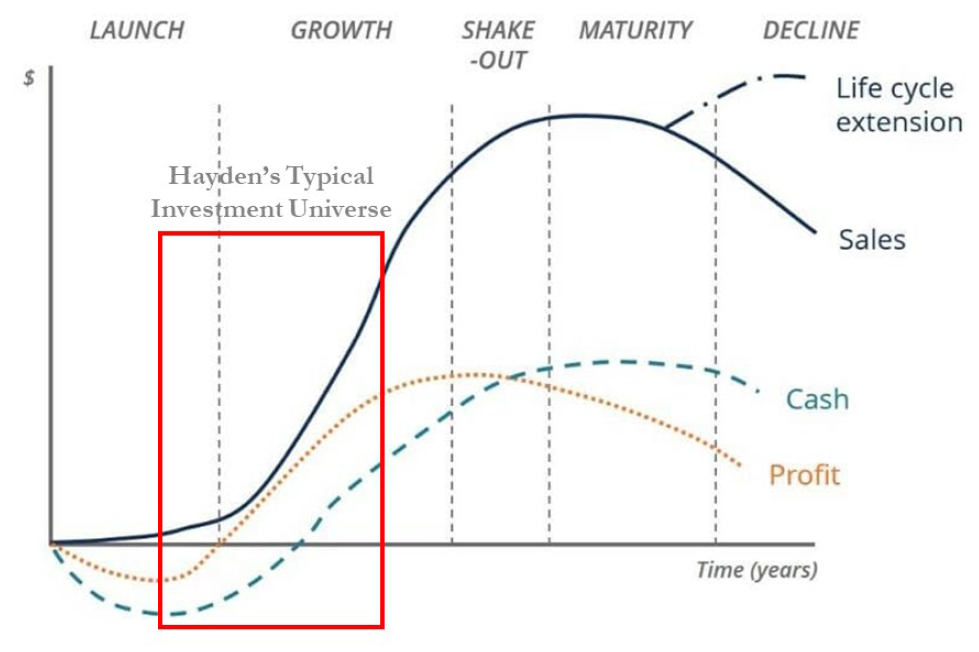

Over the past few years, I’ve described the areas we hunt for our investments and how that fits in our portfolio construction process (see our Q1 2019, Q2 2020, and Q3 2020 letters for reference).

Historically, we’ve focused on the early-stage of the S-curve. These companies are younger in their business model development, likely still a few years before they are able to generate profits and thus need external capital to reinvest into (by our calculations) high return on capital business opportunities, which given the high incremental margins will take them to profitability within a few years. Considering their nascent stage, the market tends to perceive these businesses as having a wide range of outcomes, and our alpha has historically come from being able to determine more accurately where the business trajectory might lie within this range.

Essentially, we get paid to take business model risk. As the business model proves itself to be capable of profitability, the market tends to ascribe a higher valuation to these business models than at our initial purchase due to this higher certainty / predictability. This allows us to realize valuation expansion, on top of an exponentially growing earnings stream. Once our companies are self-sustainable, our goal is to then allow our capital to compound alongside them, so long as the future reinvestment opportunities within the business remain attractive (i.e. high IRRs).

However in markets like today, this strategy is going to be extremely volatile. The reason for this, is that similar to fixed income markets where investors require higher returns in compensation for committing their capital for longer durations and higher volatility (30 year debt is more expensive than 1 year debt), I believe the equity markets exhibit a similar dynamic.

Our companies tend to be long duration (most of their profits, and thus basis for their valuations, lie further out in the future). Therefore any change in the interest rate or market environment tends to affect the market’s perceived valuation of these businesses to a greater degree, than more “stable” / more predictable companies.

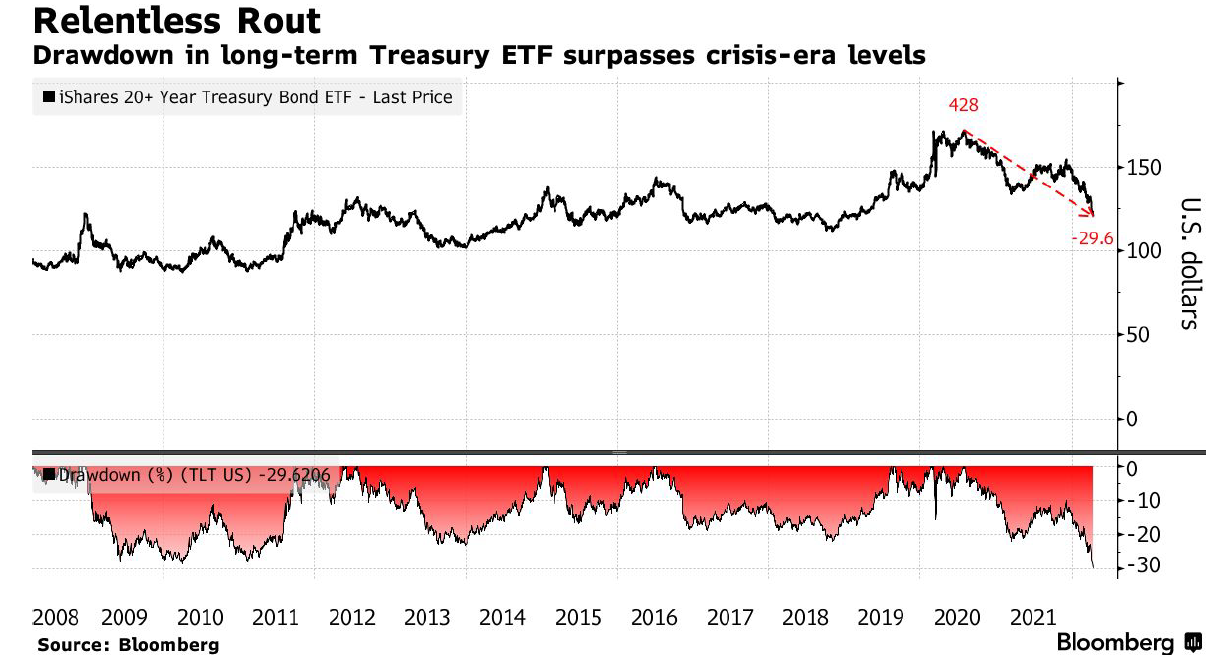

For example, US government long-term bonds have already declined by over -30% since their peak, which is even greater than in 2008 – 10. If essentially risk-free US government bonds are trading at these extremes, it’s only logical that the stock prices of our businesses, which are not only long-duration, but also have business risk as well, will decline even more.

In addition, real yields (as measured by TIPS) have increased by the quickest pace since the financial crisis of 2008. While the absolute level is still relatively low by historical standards, it’s the pace of change that matters most for financial markets. Markets tend to be able to digest yield increases if it’s done in a methodical and steady manner. However sudden changes in the yield cause turmoil and volatility, and panic to reposition investor portfolios, which is what we’re seeing today.

Long-Duration Bonds Drawdown

As of April 18, 2022 (LINK)

Most Rapid Increase in Real Yields Since 2008

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}