Guess?, Inc. GES is benefiting from growth efforts, which include focus on its strategic business plan. Strength in the company’s digital business has been aiding growth. That said, the designer, marketer and distributor of apparel and accessories has been grappling with rising costs.

Let’s discuss further.

Strategic Plan on Track

Guess? is focused on its strategic business plan unveiled in December 2019. To this end, the company is committed to its six key strategies and has made remarkable progress against them. The core strategies include organization and culture, functional capacities, brand relevance with three main consumer groups (heritage, Millennials and Generation Z customers), customer focus, product brilliance and international footprint.

Guess? is focused on implementing Customer 360, a solution developed by salesforce for personalized marketing, customer data optimization and customer journey engagement, among other objectives. As part of the Customer 360 project, management launched its CRM platform in 2021, which gives the company a 360 view of the customer and fuels improved personalization, marketing and promotional strategies. In its lastearnings call management highlighted that it has already implemented some of the solutions in Europe and is impressed with the results. The company plans to complete the rollout in North America by the middle of 2023.

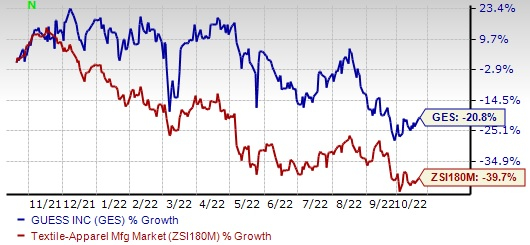

Image Source: Zacks Investment Research

The company focused on a brand-elevation strategy, which includes enhancing product quality, visual merchandising and boosting customers’ shopping experience across stores and online. In terms of brand elevation, the company is benefiting from the launch of its global line for all product categories over the last two years. The company is enhancing the customer experience while implementing various upgrades to its store and e-commerce infrastructure to improve the ease of shopping and increase customer conversion.

The company is on track with supply chain and inventory management to counter supply chain disruptions. The company has been rationalizing its store portfolio across retail and wholesale by shutting unproductive stores and accounts and lowering product offerings to develop a single business with more productive SKUs.

Digital Business: Key Driver

Guess? is benefitting from its solid digital business. The company is on track to progress with its customer-centric initiatives, including omnichannel capabilities and advanced data analytics and customer segmentation. Guess? has been on track with its digital-first initiative and is investing in brand-building through social media platforms. Management has also improved e-commerce operations through better data capturing, improved customer profiling, personalized marketing and relationship management.

Hurdles on Way

In the second quarter of fiscal 2023, the company’s gross margin contracted 470 basis points to 42.1%, mainly due to product margin compression. The downside was mainly caused by a different mix of full price versus markdown business across the Americas and Europe. Also, the adverse impact of unfavorable foreign currency rates was a concern. The adjusted operating margin came in at 8.7%, down from the 14.1% reported in the year-ago quarter, due to a margin decline across businesses, partly made up by efficient cost management.

Guess? is battling rising SG&A expenses for the past few quarters. During second-quarter fiscal 2023, its adjusted SG&A increased 5% to $215 million. The increase in such costs can be attributed to the company’s retail stores. It continues to witness labor cost pressures stemming from global inflation and solid employment in several markets.

That said, we believe that the aforementioned upsides are likely to help this Zacks Rank #3 (Hold) company stay afloat amid such hurdles.

GES’s stock has fallen 20.8% in the past one year compared with the industry’s decline of 39.7%.

Solid Consumer Discretionary Bets

Lululemon Athletica Inc. LULU, the designer and distributor of athletic apparel and accessories, sports a Zacks Rank of 1 (Strong Buy) at present. LULU has an expected EPS growth rate of 20% for three-five years. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for lululemon’s current financial-year sales and earnings per share (EPS) suggests growth of 26.6% and 26.8%, respectively, from the preceding fiscal year’s reported numbers. LULU has a trailing four-quarter earnings surprise of 10.4% on average.

Oxford Industries OXM is a renowned apparel company. It currently sports a Zacks Rank #1. OXM has a trailing four-quarter earnings surprise of 91.1% on average.

The Zacks Consensus Estimate for Oxford Industries’ current financial-year revenues and EPS suggests growth of almost 22% and 31.2%, respectively, from the earlier fiscal year’s reported figures.

Crocs, Inc. CROX, casual lifestyle footwear and accessories provider, sports a Zacks Rank #1 at present. The company has a trailing four-quarter earnings surprise of 21.9% on average.

The Zacks Consensus Estimate for Crocs’ current-year sales and EPS suggests growth of 49.7% and 20.7%, respectively, from the year-ago reported figures. CROX has an expected EPS growth rate of 15% for three-five years.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.8% per year. So be sure to give these hand-picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Guess, Inc. (GES): Free Stock Analysis Report

lululemon athletica inc. (LULU): Free Stock Analysis Report

Crocs, Inc. (CROX): Free Stock Analysis Report

Oxford Industries, Inc. (OXM): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.