Credit: Shutterstock photo

Credit: Shutterstock photoBy Niall Gannon :

By Niall J. Gannon and Scott B. Seibert, CFA

Forecasting long-term asset class returns with reliability is an important component for matching a portfolio's performance with its future liabilities. Whether one is an individual investor or a public pension fund, a reliable estimate of an asset's minimum expected return is critical for financial planning purposes. Using the United States public pension system as an example, the use of inflated return expectations has perpetuated a growing deficit. According to Moody's, in 2017, US public pension plans had unfunded liabilities of over $4 trillion. A deficit this massive can only be rectified by either cutting previously promised benefits for current participants or having future generations pick up the difference through higher contributions, sacrificing their standard of living. Most investors have an understanding that inception yield is predictive of the future returns of a fixed-income (bond) portfolio. We aim to illustrate that starting earnings yields are similarly predictive of the future returns in an equity portfolio, over 20-year investment periods.

Much of the previous financial research suggests either that forecasting future returns a futile exercise because returns are random, or that asset class performance tends to display a reversion to the mean of its historical observations. Eugene Fama, known for developing the Efficient Market Hypothesis, famously stated:

Among those who adhere to the theory of mean reversion, Jeremy Siegel wrote in Stocks for the Long Run (2007) that stock returns "cling" to a statistical trend line. In reality, for the first 18 years of the 21st century, the total return on the S&P 500 index (with dividends reinvested) was only 5.34%, approximately 50% lower than its often-quoted long-term average of 10%. Was this dramatic underperformance of stocks for such an extended period truly a function of randomness? Does the degree of this underperformance weaken the theory of reversion to the mean? Our analysis seeks to narrow the gap between an investor's equity return expectations and the actual future returns received. We aim to illustrate, utilizing 20-year rolling periods, that equity returns and portfolio performance over the long run do not perform randomly, but rather, are remarkably predictable.

Hypothesis

The study seeks to demonstrate that much of the long-term (20-year rolling periods) variability in stocks can be explained by the beginning-of-period earnings yield (the inverse of the starting price-to-earnings ratio). If our hypothesis is correct, investors can plan for the future using a forecasted minimum expected return to be realized over a 20-year investment horizon.

Method Description

A typical 20-year investment horizon includes multiple business cycles, possibly comprised of unexpected economic events, which have the potential to add or subtract from investment returns over the analysis period. According to the National Bureau of Economic Research (NBER), the United States has experienced 11 business cycles during the modern era, 1945-2009. The average cycle length, whether measured from trough from previous trough or peak from previous peak, is roughly 69 months, or 5.75 years. We seek to neutralize the impact of outsized returns derived from a single business cycle by focusing on 20-year rolling periods. In choosing the beginning-of-period price-to-earnings ratio as the starting point for our analysis, we have selected a measure of valuation that is widely available and well understood by investors.

Time Period

A total of 42 rolling full calendar year 20-year periods exist in the analysis period, which begins at the inception date of the S&P 500 on January 1, 1957 and ends December 31, 2017 (1957-2017). Each rolling 20-year period has its own annualized return.

Annualized Returns

The 20-year annualized rolling returns from the S&P 500 are presented. The returns are displayed as a pre-tax and pre-liquidation return of the S&P 500 over each 20-year period.

P/E

The price-to-earnings ratio is presented as of January 1 of the beginning year of each 20-year period.

Earnings Yield

The earnings yield of the index is derived from taking the inverse of the price-to-earnings ratio at the beginning of each period (January 1).

Return - EY

The beginning of period earnings yield is compared to the actual 20-year annualized return produced during the 20-year period. The difference between the actual annualized return and the earnings yield is displayed.

Exhibit 1

Results

Using the earnings yield as a minimum expected return, the hypothesis was successful at a rate of 95%. Over the 42 periods, only two scenarios had a realized annualized return less than the beginning-of-year earnings yield "forecast". The two periods that didn't meet the minimum expected return were 1958-1977 and 1989-2008. For 1958-1977, an annualized return of 7.79% was realized versus an earnings yield forecast of 8.40%, which resulted in a missed forecast of -.62%. In 1989-2008, an annualized return of 8.34% was realized versus an earnings yield forecast of 8.70%, which resulted in a missed forecast of -.35%. A couple of similarities exist with the two periods that didn't meet the forecasted earnings yield. First, both of the earnings yields fell in the 75th percentile of all starting earnings yields. Also, in both scenarios, the last year of the analysis period was a negative total return year for the S&P 500. The total return was -6.76% in 1977 and -36.12% in 2008. The combination of a high earnings yield forecast plus a negative return in the final year of the analysis partially contributed to the missed forecasts.

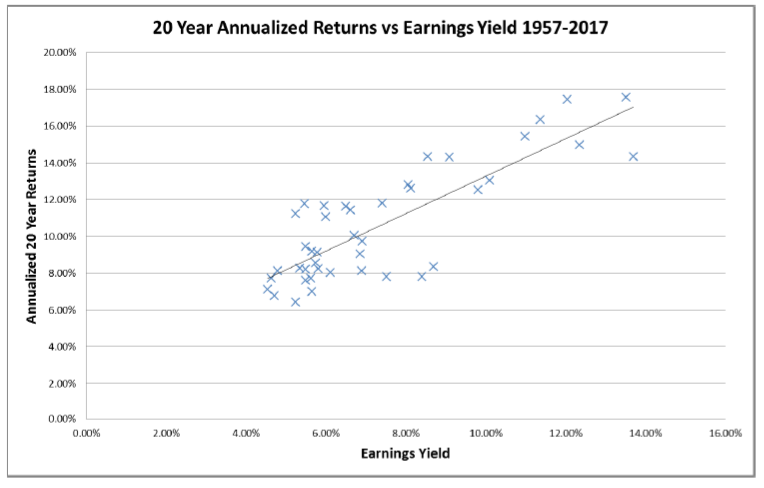

Exhibit 2

In Exhibit 2, we have plotted the annualized 20-year returns versus earnings yield from the 42 periods that were observed in the analysis. The correlation of the data sets as shown in Exhibit 1 is .83, representing a strong linear correlation. In analyzing the data further, through a regression analysis, we calculate that the R2, the coefficient of determination, was 68%. Therefore, 68% of the variation in 20-year annualized returns is explained by beginning year earnings yield. The equation of the line of best fit is: 20-year annualized return = 1.02*(Earnings Yield) + .0307.

Observations of extreme high/low points of historical returns and earnings yields:

- The highest observed earnings yield of 13.7%, in 1975, produced a 14.33% annualized return.

- The lowest observed earnings yield of 4.54%, in 1998, produced a 7.11% annualized return.

- The highest observed 20-year portfolio return of 17.56% (1980-1999) began with an earnings yield of 13.51%.

- The lowest observed 20-year portfolio return of 6.42% (1959-1978) began with an earnings yield of 5.24%.

- Analyzing 2000-2017 (18 years): The beginning earnings yield in 2000 was 3.52%, and the annualized return, over 18 years, is currently tracking at 5.34%. The 2000 vintage portfolio is on pace to produce a lower annualized return than any other vintage since 1957. Also, the 2000 vintage portfolio has the lowest starting earnings yield of any observed year since 1957.

Conclusions

Our conclusions from the analysis:

- A strong correlation exists between 20-year annualized returns of the S&P 500 and the beginning-of-period earnings yield.

- Much of the variation in 20-year annualized returns can be explained by beginning-of-period earnings yield.

- Beginning-of-period earnings yield provides a useful estimate of minimum expected return that investors can expect over a long-term horizon, specifically a 20-year investment period.

- Excess return above starting earnings yield is unexplained in this study when only using historical data available to an investor at the beginning of each period. We strongly suspect that forward earnings growth and/or inflation is the driver of the unexplained portion of the forward expected return.

- Long-term portfolio forecasting includes the mandate for investors to consider real (net of inflation) returns. The nominal returns observed in this study provide a baseline from which investors can model for various forward-looking inflation scenarios.

Investors should use the earnings yield to approximate a minimum expected return for future financial planning. This conservative estimate of future returns could help reduce the unfunded liabilities that have accumulated in public pension plans due to poor forecasting. For individual investors, it should provide confidence that a minimum expected return can be achieved, even with unforeseen events, when investing over long time horizons. In the practice of setting asset allocation policy, the use of earnings yield as a minimum expected return produces a more informed comparison of the future return potential of equities versus fixed income than the application of the theory of mean reversion or the Efficient Market Hypothesis.

References:

Fama, E.F. "Random Walks in Stock-Market Prices." Financial Analysts Journal , Vol. 21, No.5 (1965), pp. 55-59.

Moody's Investors Service. "State and local government - US: Pension burdens to rise through 2020, even in positive investment scenario." June 2017 ( Source )

The National Bureau of Economic Research. " US Business Cycle Expansions and Contractions ." 2017

Siegel, Jeremy. Stocks for the Long Run: The Definitive Guide to Financial Market Returns and Long-Term Investment Strategies (4th Edition). New York: McGraw-Hill, 2007. Print.

Silverblatt, H. " S&P 500, Ticker: SPX ." S&P Dow Jones Indices. 2017

See also Ship Finance International: Q4 Results Show Strength on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}