Credit: Shutterstock photo

Credit: Shutterstock photoBy Charlie Bilello :

Donald Trump made headlines this week in accusing Janet Yellen and the Fed of keeping interest rates low to help President Obama. Trump said :

A fair amount of showmanship and hyperbole here on the part of Trump, but it raises an interesting question.

If the economy is the number one issue in almost every election and the Federal Reserve has the power to influence the economy through monetary policy, does the Fed hold the fate of the next election in its hands?

First, we need to establish that it is indeed the economy that is the best predictor of the presidency.

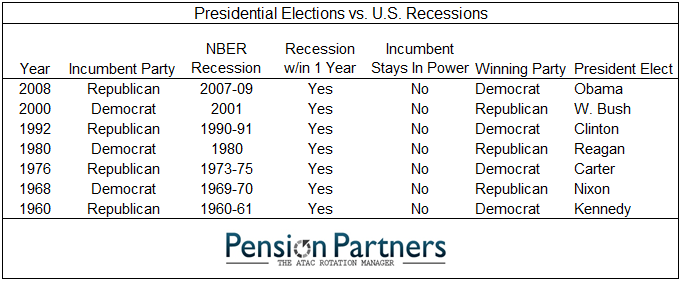

Recession = Change of Party

Since 1960, in every presidential election in which the U.S. economy was in or near a recession, the incumbent party has lost. Barack Obama was the last beneficiary of this correlation back in 2008 when the U.S. economy was in the midst of the worst recession since the Great Depression. Before Obama, presidents who defeated the incumbent party during U.S. recessions included: George W. Bush, Clinton ( It's the economy, stupid ), Reagan, Carter, Nixon and Kennedy.

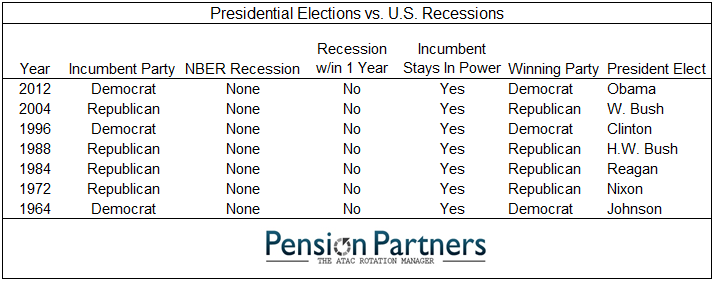

Expansion = Remain in Power

Contrast this outcome with elections during which the U.S. economy was in an expansion. Here we see that the incumbent party has remained in power each and every time. The deciding factor for a "two-term" presidency has been the economy, with Obama, George W. Bush, Clinton, Reagan and Nixon winning a second term as economic conditions were favorable during their reelection year.

If we accept that the economy greatly influences presidential elections, to prove the Fed can influence the result of an election, we still need to show the linkage between monetary policy and the economy.

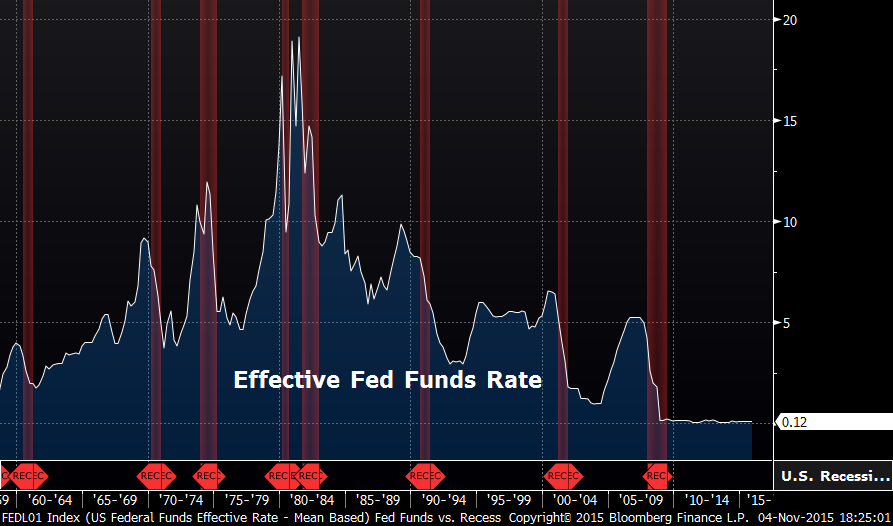

Recessions and Rate Hikes

Since 1960, every U.S. recession has been preceded by a rate hiking cycle. That is not to say that hiking rates immediately leads to or is even the proximate cause of a recession, just that no recession has occurred without a tightening of monetary policy.

Regardless, it is widely accepted that raising short-term interest rates is a tool that can be used to not only tame inflation, but also to cool an "overheated" economy. While it may not be the "cause" of a recession, then it certainly can be an important underlying factor. The opposite is also true, whereby cutting interest rates or leaving them at extraordinarily low levels is viewed as a tool to spur asset price inflation and growth.

As we know, the Federal Reserve has kept the Federal Funds Rate at close to 0% for the past seven years, by far the longest period of easy monetary policy in history. During this time, it has also expanded its balance sheet (Quantitative Easing 1, 2 and 3) from $900 billion to over $4.5 trillion. These policies were said to be integral in preventing the U.S. economy from slipping into a second Great Depression. Whether that is true or not we'll never know as the counterfactual (not moving all the way to 0% and not engaging in QE) is unknowable.

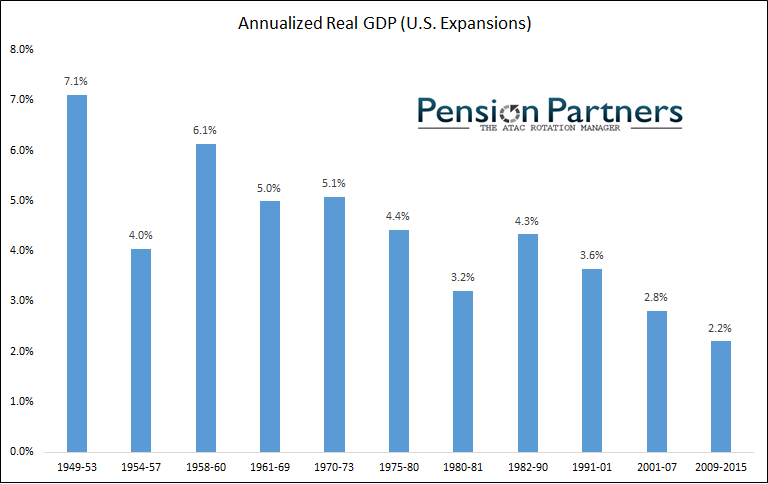

What we do know is that the economic expansion is now in its sixth year, and at 2.2% real growth, it has been the slowest on record. With nominal growth at only 2.9% over the past year, many are concerned that it would not take much to push the U.S. into another recession.

Election in the Hands of the Fed?

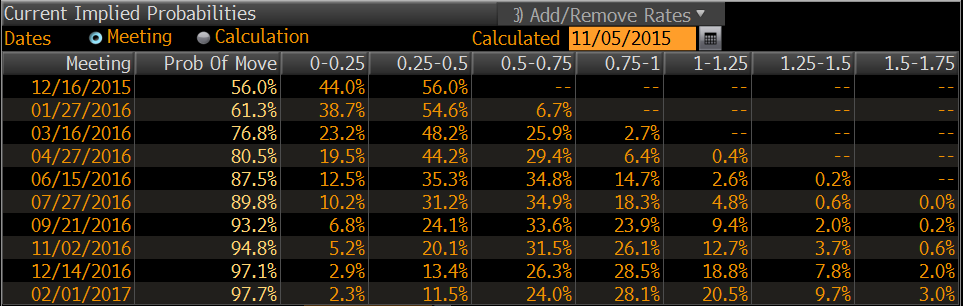

Which brings us back to the Fed and the idea that should it start hiking "too early," it would jeopardize the expansion. Financial markets are now expecting (56% probability) the Fed to move in December, bringing this issue to the forefront.

If it goes ahead with this hike, and more importantly, follows it up in 2016 with more hikes, would it be enough to push the U.S. economy into a recession? That remains to be seen, but if recessionary conditions do emerge in 2016, it would most certainly have an impact on who the next president is. As we know, the electorate has not treated the incumbent party kindly during periods of economic weakness.

Which means that, ironically, this time next year we could be talking about how President Trump owes his victory to the "highly political" Janet Yellen.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Pension Partners, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial orinvestment adviceon any subject matter. Pension Partners, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Charlie Bilello, CMT

Charlie Bilello is the Director of Research atPension Partners, LLC, an investment advisor that managesmutual funds and separate accounts. He is the co-author of threeaward-winning research paperson market anomalies and investing. Mr. Bilello is responsible for strategy development, investment research and communicating the firm's investment themes and portfolio positioning to clients. Prior to joining Pension Partners, he was the Managing Member of Momentum Global Advisors previously held positions as an Equity and Hedge Fund Analyst at billion dollar alternative investment firms.

Mr. Bilello holds a J.D. and M.B.A. in Finance and Accounting from Fordham University and a B.A. in Economics from Binghamton University. He is a Chartered Market Technician and a Member of the Market Technicians Association. Mr. Bilello also holds the Certified Public Accountant certificate.

See also Could The Fed Hike The Discount Rate On Monday? on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}