Fact-Checking the Data Debate

We recently took a top-down view of investor costs. It showed that all-in exchange costs are just a small part of overall investor costs.

Today we take a bottoms-up view of exchange costs. The data presents a different view from what is normally discussed around the major exchanges’ market data businesses.

All exchange fees are regulated and transparent

The first important fact is that all exchange fees are regulated, which means all changes need to be filed with the SEC and rate sheets and customer tiers made public. That includes listing fees, colocation and prop data fees. Even the SIP rate sheets and revenue share back to exchanges are publicly available.

That’s important because it means there is data on exchange fees and each change over time. In fact, analysis of our filings over the past 10 years shows that most fees are unchanged on a year-to-year basis. For example, since around 2009, 85% of data fees and 95% of colocation fees are unchanged each year, and for more than a quarter of fees that did change, costs were reduced.

Interestingly, a “loophole” does exist for exchanges that don’t own their own data centers. In those instances, members who want to purchase colocation services will buy them directly from independent data center providers. Because these providers that are not exchanges are not regulated by the SEC and thus not required to disclose pricing or even ensure fair and equal access.

Growth in our accounting statements isn’t from U.S. equities

Another common error is to assume that all a modern exchange does is trade U.S. equities. In fact, data shows that relatively little revenue growth in our accounting statements relates to U.S. equities trading.

For example, almost all the growth in “data” over the past 10 years comes from acquisitions, diversification and new customers (Chart 1). It’s clear our competitors, like ICE and Cboe, also have globally diversified income streams.

According to recent findings from analyst firm Burton-Taylor, “M&A activity is driving revenue gains in these segments with some key acquisitions over recent years … Burton-Taylor maintains that inorganic revenue growth is driving the majority of segment gains. Exchanges are also benefiting from their index operations, which are experiencing double-digit percentage revenue increases.”

Chart 1: Nasdaq data revenues from our accounting statements show most of the growth comes from acquisitions and new products unrelated to U.S. equities

Source: Nasdaq Economic Research (*SIP revenue allocation in 2018 was $110 million, down $37 million from 2008, per UTP and CTA)

Although it is true that regulated U.S. equity market data for Nasdaq has increased, with a 6.6% CAGR (compound annual growth rate over 10 years), it’s important to also understand that didn’t all come from existing customers.

In fact, two-thirds of that came from new customers and sales. Existing customers who have not purchased additional products or expanded existing services have seen fee changes increase their costs by only 2.4% CAGR, not much more than the rate of inflation (Chart 2). That’s despite the fact that over the same time, the capacity and latency of our matching engine has more than doubled.

Chart 2: Where regulated data growth has come from

Source: Nasdaq Economic Research

Claims by industry groups that cherry-pick products or customers to say prices increase by over 1,000% aren’t representative of the overall average customer experience.

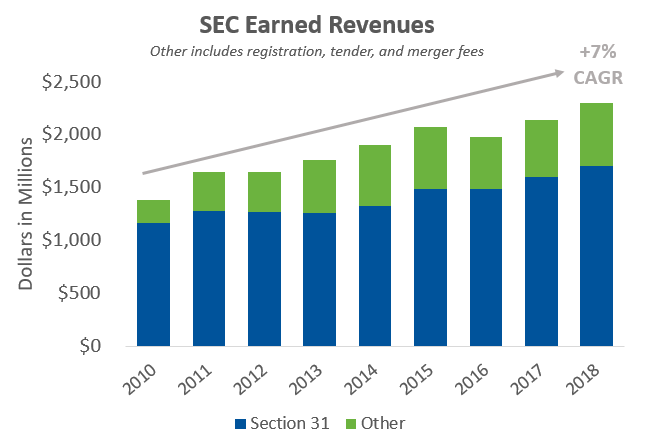

How does that compare to other regulated costs?

One publicly available cost is Section 31, or so called “SEC fees.” Section 31 of the Securities Exchange Act of 1934 allows the SEC to collect a fee from all exchanges based on the volume of securities sold. Interestingly these are:

- Charged in basis points, in contrast to most trading costs which are in cents-per-share.

- Passed through to customers on their contract notes, at cost, whereas rebates remain bundled into broker commissions.

Based on the SEC’s annual financial summary, the total annual cost of these fees has been growing at a 7% CAGR over the past 8 years. That’s more than double the rate of inflation.

Chart 3: SEC earned revenues have trended upwards

Source: SEC, Nasdaq Economic Research

Perhaps even more importantly, it now adds to over $2 billion, which we estimate is more than the industrywide all-in-costs of all U.S. exchanges combined.

Other industry costs are less transparent

It would be good to be able to compare these to other investor costs. We tried, but costs for EMS’s and terminal costs are notoriously opaque. Although a series of estimates show this likely costs over $10 billion per year, how it breaks down to U.S. equities is also difficult to discern.

Similarly, commissions remain bundled and opaque. In contrast to exchange pricing disclosures, there is little public information about the rates charged to different customers. In today’s competitive market, it’s hard to believe that commission rates don’t vary by customer based on their net rebate capture. Ironically, if they do, the Access Fee Pilot may have no broker conflict to fix at all.

Although there may be a lot of important data missing from the current debates, the facts show that data on exchanges is the most public and regulated of all.

Other Topics

Market Regulation

Phil Mackintosh

Nasdaq

Phil Mackintosh is Chief Economist and a Senior Vice President at Nasdaq. His team is responsible for a variety of projects and initiatives in the U.S. and Europe to improve market structure, encourage capital formation and enhance trading efficiency.

Read Phil's Bio