Exxon Mobil Corporation XOM is set to report first-quarter 2026 results on May 1, before the opening bell.

The Zacks Consensus Estimate for first-quarter earnings is pegged at $1.07 per share, implying a decline of 39.2% from the year-ago reported number. It has witnessed no estimate revisions in the past seven days. The Zacks Consensus Estimate for first-quarter revenues is currently pegged at $81.5 billion, suggesting a roughly 2% fall from the year-ago actuals.

XOM beat the consensus estimate for earnings in each of the trailing four quarters, with the average surprise being 4.2%. This is depicted in the graph below:

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Q1 Earnings Whispers for XOM

Our proven model doesn’t predict an earnings beat for XOM this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the chances of an earnings beat. That isn’t the case here.

The leading integrated energy player has an Earnings ESP of -10.88%. XOM currently carries a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

XOM’s Factors to Note

In its latest 8-K SEC filings, XOM stated that it is likely to see a sequential improvement in the March quarter upstream earnings by $1.9 billion to $2.3 billion due to an increase in liquid prices.

To have an idea of how oil prices behaved in the March quarter, let's analyze the commodity prices from the data provided by the U.S. Energy Information Administration (“EIA”). The average Cushing, OK, WTI spot prices for January, February and March of this year were $60.04 per barrel, $64.51 per barrel and $91.38 per barrel, respectively, per EIA data. Commodity prices were $60.89 per barrel, $60.06 per barrel and $57.97 per barrel, respectively, in October, November and December, according to the EIA. Investors should note that a more favorable crude pricing environment is also likely to have aided the upstream businesses of other integrated giants like BP plc BP and Chevron Corporation CVX.

Coming to the natural gas story, XOM expects gas prices to sequentially increase its upstream earnings by $200 million to $600 million.

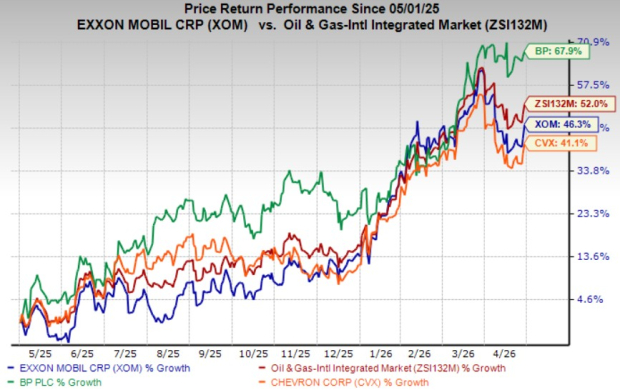

XOM’s Price Performance & Valuation

XOM's stock has jumped 46.3% over the past year, underperforming the industry’s 52% surge. BP has gained 67.9% over the same time frame, while Chevron, in the same space, has improved 41.1%.

One-Year Price Chart

Although XOM’s stock price has underperformed the industry, the company appears relatively overvalued. The company's current trailing 12-month enterprise value/earnings before interest, tax, depreciation and amortization (EV/EBITDA) is 9.85x, reflecting that it is trading at a premium compared with the industry average of 6.83x. While BP is valued lower at 3.78x, CVX is valued higher at 9.92x.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Investment Thesis of XOM

The price of West Texas Intermediate (“WTI”) crude is trading at more than the $105 per barrel mark. Ongoing tensions in the Middle East are driving the high price. The highly favorable pricing environment for the commodity is likely to continue to support ExxonMobil's exploration and production activities, given its strong portfolio of upstream assets.

To provide a glimpse of the upstream assets, the company has a massive footprint in the Permian, the most prolific oil and gas play in the United States, and offshore Guyana. In the Permian, the integrated giant has been employing lightweight proppant technology and hence has been capable of boosting its well recoveries by up to as much as 20%.

In Guyana, XOM has made several oil and gas discoveries, further highlighting its solid production outlook. Record production from both resources has been aiding its top and bottom lines. In both resources, the breakeven costs are low.

Last Word

Considering the backdrop, it might be wise for investors to bet on the integrated energy giant ahead of earnings.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>BP p.l.c. (BP) : Free Stock Analysis Report

Chevron Corporation (CVX) : Free Stock Analysis Report

Exxon Mobil Corporation (XOM) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.