By Emiliano Rabinovich, Senior Portfolio Manager, CFA, State Street Global Advisors

Around the world, Environmental, Social and Governance (ESG) investing has seen rapid growth over recent years. In the US, however, demand from institutional investors for ESG or climate-integrated investment strategies has lagged that of its European and Asian counterparts – but it is growing quickly. US ESG fund flows reached $10.4 billion for in the second quarter of 2020, which on a year-to-date basis nearly matched the full-year 2019 sustainable fund net flows of $21.4 billion.1

The US Department of Labor’s recently proposed rule, entitled Financial Factors in Selecting Plan Investments, sought to clarify obligations related to the consideration of ESG factors by fiduciaries responsible for retirement plans. As investors continue to evaluate these obligations, this article provides a framework for assessing ESG performance as it tracks the returns of four prominent US ESG index strategies versus the benchmark – using the extreme market volatility caused by the COVID-19 pandemic as a unique test of the strategies’ performance.

Performance of Four Equity ESG Indices

ESG can play a key role in identifying potential business and financial risks, which in turn, can impact a company’s share price. There is also strong empirical evidence that ESG considerations have contributed to long-term sustainable returns.2

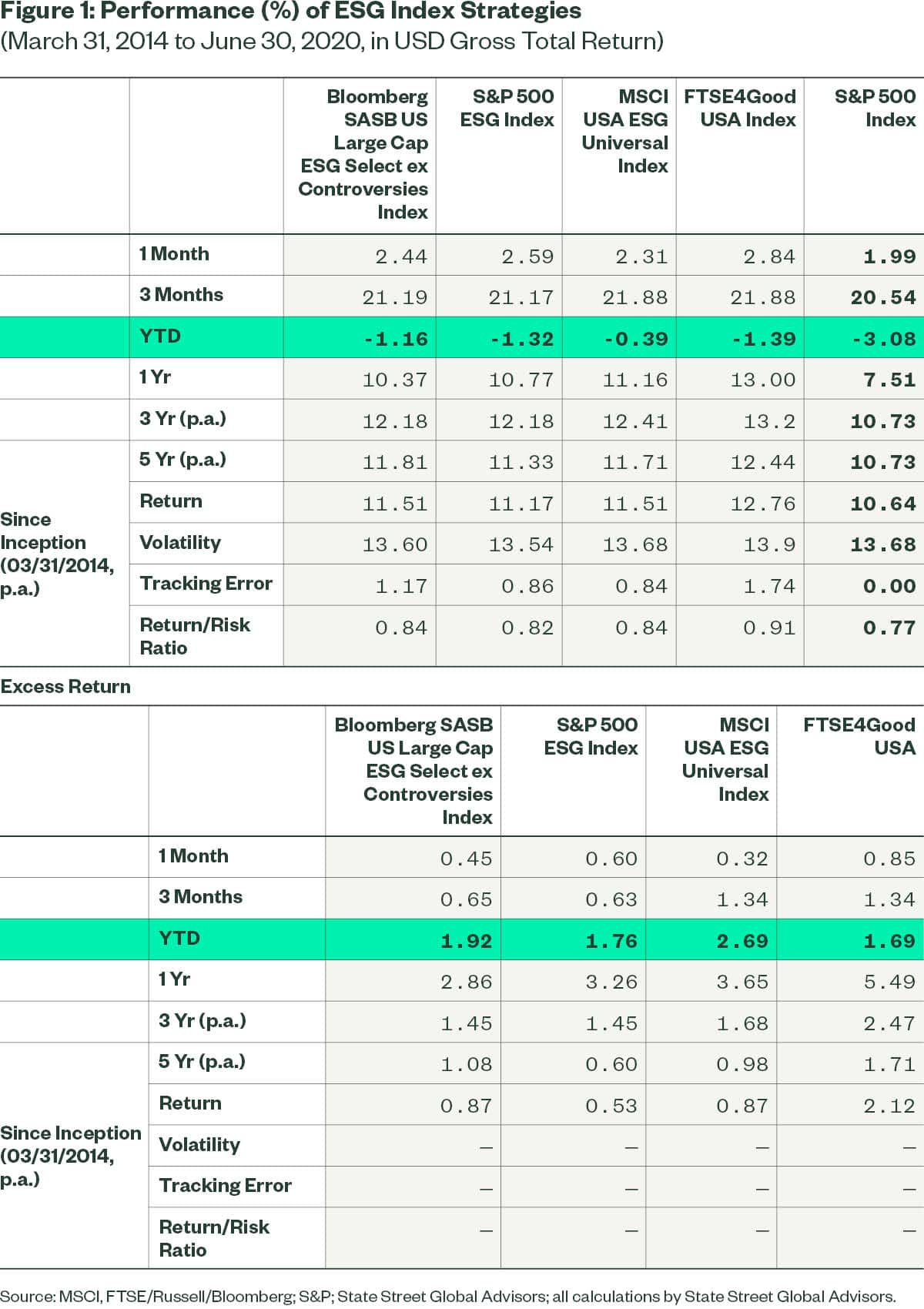

Over the first half of 2020, ESG integrated index strategies have been a source of added value vis-à-vis the broad market, as measured by the S&P 500 Index. We determined this by analyzing the performance of four US equity ESG indices, created by four different index providers (in order to remove any construction bias). As summarized in Figure 1, the four ESG index strategies provided consistent outperformance relative to the market cap index, year-to-date, for 1 year, 3 years, 5 years and since inception of the Bloomberg SASB US Large Cap Select index (in March 2014).3

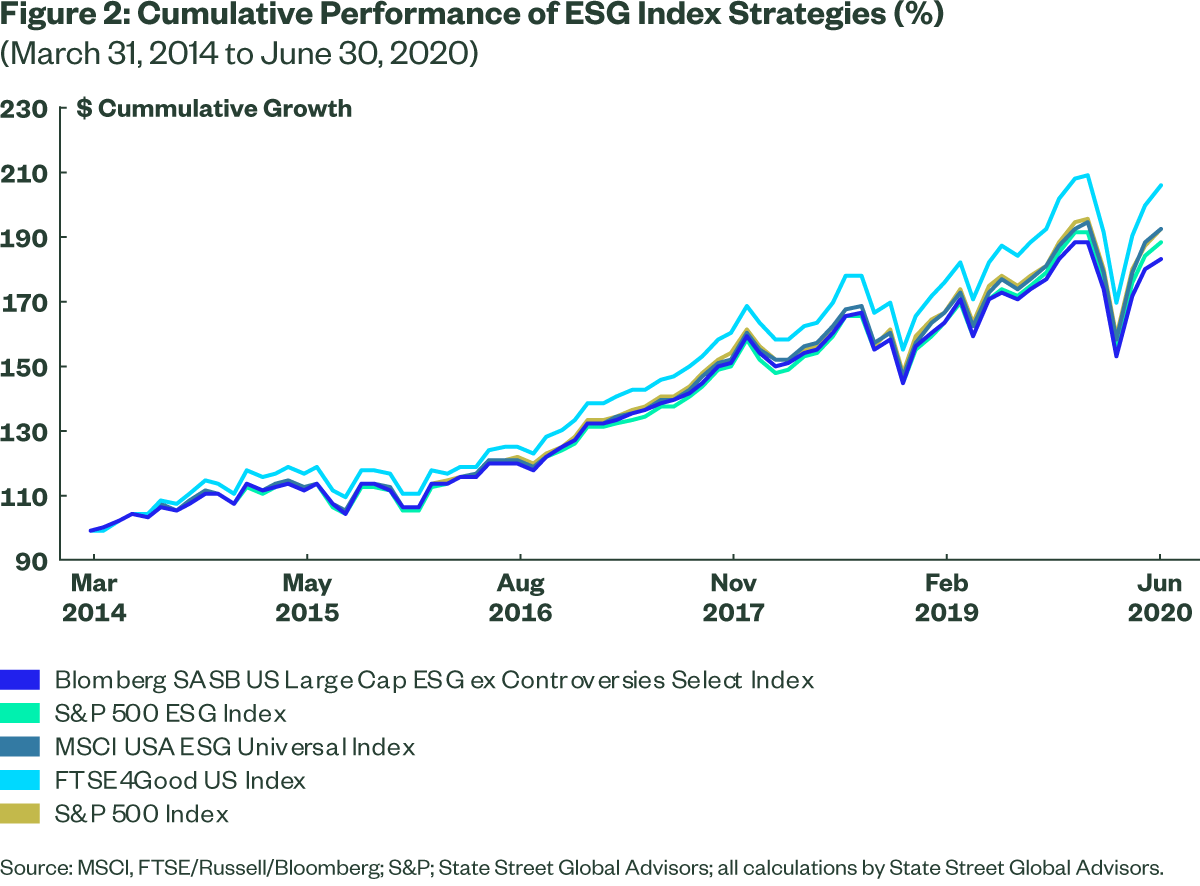

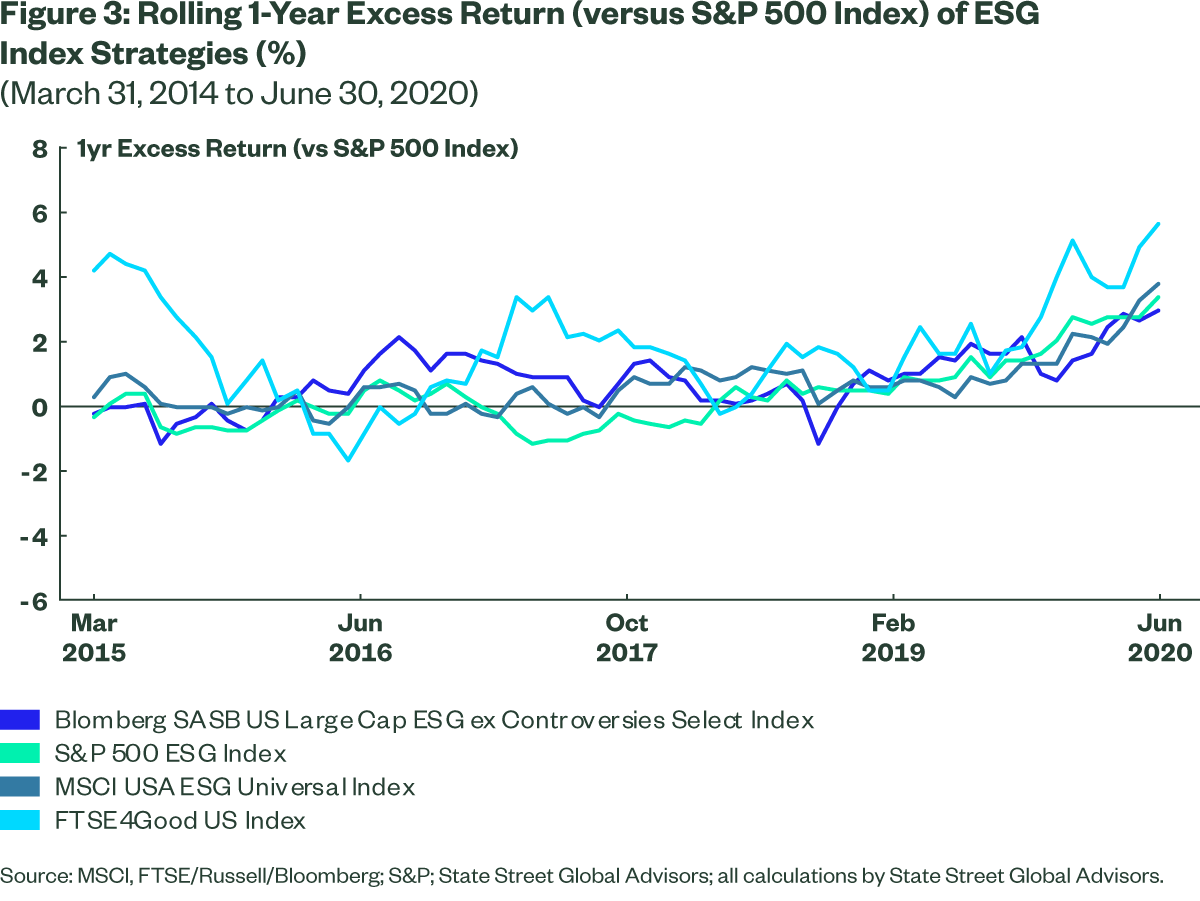

While many ESG indices represent a departure from the traditional market-capitalization weighting scheme, they are generally designed to reflect broad risk and return characteristics while targeting an improved ESG profile. This “index-awareness” is demonstrated in the performance journeys displayed in Figure 2, and Figure 3 provides the rolling 1-year excess return of these strategies versus the S&P 500. Despite some divergent return patterns near the beginning of 2020, all four ESG indices demonstrated incremental increases in excess return over the first half of 2020.

Portfolio construction explains some of the performance differences among ESG index strategies shown in Figure 3. For example, the FTSE4Good index takes on more active risk relative to the other index strategies, suggesting that it should outperform other ESG strategies during time periods when, collectively, ESG does well. Note that this level of active risk may not be appropriate for all investors. The Appendix summarizes the portfolio construction approaches taken by the four ESG index strategies.

Although the magnitude of the outperformance varies among the different ESG index providers, it’s important to note that each has beaten the benchmark over time and has done so consistently, regardless of ESG methodology or ESG data provider. And while past performance is not an indicator of future results, we believe that the performance demonstrated by US ESG Indices since their inception is worthy of consideration.

Drivers of ESG Outperformance

So what are the drivers of the year-to-date outperformance of the four US ESG indices, and are they the same across the different permutations of ESG index strategies? To understand performance drivers over the first half of 2020, we decomposed active returns and identified three common themes.

Sectors

We performed a sector attribution for the ESG indices relative to the S&P 500 Index, for one year as of June 30, 2020. For all four of the indices, Information Technology was the sector that contributed most to outperformance. Depending on the specific index construction approach, Industrials, Financials and Consumer Discretionary all contributed to outperformance. Interestingly, the Energy sector underweight that is a common theme in ESG index strategies was not found to be a large driver of added value.

Factors

All four indices also show modest active style factor exposure relative to the S&P 500. We see positive exposure to momentum (given the strong performance these indices exhibited) and profitability (usually associated with high-quality stocks). At the same time, we see negative exposure to value and leverage (again associated with high-quality stocks). Given the limited history of robust ESG data (versus traditional style factor premia), we didn’t expect to see a consistent relationship between the ESG profile and any one particular style factor. Rather, sources of active risk and return may be attributable to idiosyncratic features of a provider’s ESG signal.

ESG Signal

We examined the ESG index exposure and attribution through the lens of State Street’s R-Factor™ an innovative, transparent ESG scoring mechanism that measures the performance of a company’s business operations and governance as it relates to financially material ESG issues facing that company’s industries. R-Factor™ facilitates an objective analysis of the ESG tilts embedded in each of these indices. Note, however, that while we believe that companies with higher R-Factor scores are generally managing their ESG risks better, and that the proactive management of ESG risks is a marker of company performance, this of course does not always result in better stock performance.

All indices demonstrate an improved ESG profile vis-à-vis the S&P 500 index, as measured by R-Factor™. In addition to incorporating an ESG tilt, index construction plays an important role in holdings and therefore performance. For example, the MSCI USA ESG Universal Index presents a very low R-Factor™ improvement over the S&P 500 Index, but this is likely due to the index methodology that prioritizes diversification through a large number of securities with only a minimal ESG tilt. Investors looking for indices that provide higher exposure to ESG should note these key construction differences.

And, while all indices reported a positive overweight to R-Factor™, the highest scoring ESG stocks (i.e., first quintile) made by far the largest contributions to active returns, resulting in a positive allocation effect all ESG indices. See Figure 4. This reinforces our perspective that an improved ESG profile was a likely source of value add over the past year.

Summary

ESG index performance in the US has experienced strong, consistent performance in recent years, including during the COVID-19-related market volatility. While the US regulatory environment remains uncertain for now, ESG investing is achieving grassroots support from a number of public and private investors across the country. As stewards of capital, State Street believes investors should consider a range of risk and opportunities that could impact investment returns, and these include material ESG factors alongside the traditional financial factors. And while there is still more work to do in standardizing ESG metrics, methodologies, and reporting, we hope these arguments elevate the investment community’s conviction that financially material ESG considerations are key drivers of long-term sustainable performance.

APPENDIX

ESG Index Portfolio Construction Comparison

| Bloomberg SASB US Large Cap ESG ex Controversies Select Index | S&P 500 ESG Index | MSCI ESG Universal Index | FTSE4Good Global Index | |

| Index Provider | Bloomberg | S&P Dow Jones Indices | MSCI | FTSE Russell |

| ESG Score Provider | SSGA (R-Factor™ ESG Score) | S&P DJI ESG Score | MSCI ESG Research | FTSE ESG Ratings |

| ESG Exclusion Categories | Controversial Weapons, Severe ESG Controversies, Tobacco, Civilian Firearms, UNGC Violators, Thermal Coal | Controversial Weapons, Thermal Coal, Tobacco, UNGC Violators, Weakest ESG scores,

Reputational Risk |

Controversial Weapons, Severe ESG Controversies, Weakest ESG scores

|

Controversial Weapons, Controversies, Tobacco, Coal, Investment Trusts

|

| Index Construction Approach

(Selection/Weighting) |

Optimization | Up to 65% (of the float adjusted market-cap universe), ranked best to worst on ESG score and market cap weighted. | All stocks in eligible universe, weighted by the product of the market cap weight * combined ESG score. | Minimum ESG rating required (above 3.3) and market cap weighted

|

| Sector/Stock Constraints | Sector/Stock Active: +/-1.0% | n/a | Max 5% stock weight | n/a |

| Number of Names* | 180 | 310 | 598 | 270 |

| Predicted Tracking Error* | 1.42% | 1.91% | 1.35% | 2.77% |

*Source: Factset, as at June 30 2020. See individual index provider methodology documents for more detailed information.

1 Morningstar, as of 30 June 2020.

2 Serafeim, Khan et al. “Corporate Performance: First Evidence of Materiality.” HBR 2017

3 The earliest common inception date across all four indices

4 State Street’s Responsibility Factor, or R-Factor™, relies on three key principles: 1) Multiple ESG data sources; 2) Transparent materiality framework defined by the Sustainable Accounting Standards Board (SASB); 3) Governance scoring influenced by State Street’s asset stewardship team.

5 It is important to highlight that the Bloomberg SASB Large Cap Select ex Controversies Index utilizes R-Factor™ in its construction process, and therefore tends to show higher exposure to this metric, relative to the other indices.

Originally published by State Street Global Advisors, 10/8/20

Disclosures

Marketing Communication

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent. The returns on a portfolio of securities which exclude companies that do not meet the portfolio’s specified ESG criteria may trail the returns on a portfolio of securities which include such companies. A portfolio’s ESG criteria may result in the portfolio investing in industry sectors or securities which underperform the market as a whole. Responsible-Factor (R Factor) scoring is designed by State Street to reflect certain ESG characteristics and does not represent investment performance. Results generated out of the scoring model is based on sustainability and corporate governance dimensions of a scored entity. The information provided does not constituteinvestment adviceand it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor. All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The views expressed in this material are the views of the ESG Research team through the period ended August 31, 2020, and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal. The information contained in this communication is not a research recommendation or investment research and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence ofinvestment research(b) is not subject to any prohibition on dealing ahead of the dissemination ofinvestment research

© 2020 State Street Corporation.

All Rights Reserved

3275487.1.1.GBL.RTL

Exp. Date: 10/31/2021

Read more on ETFtrends.com.The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.