e.l.f. Beauty, Inc. ELF delivered another quarter of solid top-line momentum in the second quarter of fiscal 2026, though profitability remained under pressure as tariffs continued to weigh on costs. Gross margin contracted about 165 basis points to 69%, mainly due to higher tariff expenses, somewhat compensated by pricing and mix.

The margin strain extended beyond gross profit. Operating income fell to about $7.7 million from $27.9 million a year earlier, with the operating margin contracting significantly. Adjusted EBITDA totaled roughly $66 million, representing 19% of sales, down from the prior year’s level. All of this underscores the drag tariffs and higher expenses are having on profitability.

Nonetheless, demand trends remained encouraging. ELF’s net sales advanced 14% in the quarter due to continued market share gains for the core brand and another quarter of outperformance compared with the broader mass cosmetics and skin care categories. The company highlighted that despite the global $1 price hike implemented on Aug. 1, 75% of its portfolio still sits at $10 or less, helping preserve its value positioning.

Easing tariff comparisons later in the fiscal year is expected to provide margin relief. Per the second-quarterearnings call e.l.f. Beauty is cycling a 45% tariff rate and anticipates a lower average rate as it moves into the next year, which should help stabilize and potentially rebuild margins.

That said, tariffs remain the main obstacle to profitability for now, though strong demand and pricing execution place ELF well for future margin recovery.

How the Margin Story Looks for COTY & EL

Coty Inc. COTY is also feeling the sting of cost pressures. In its latest quarter, COTY reported a 100-basis-point decrease in the adjusted gross margin to 64.5%, including a 40-basis-point tariff headwind that directly weighed on profitability. Coty emphasized that tariffs remain a meaningful drag for the business even after mitigation efforts, signaling that the company is navigating a tough cost environment.

Meanwhile, The Estee Lauder Companies Inc.’s EL gross margin expanded 60 basis points to 73.3% in the first quarter of fiscal 2026, supported by operational efficiencies and lower promotional intensity under its PRGP program. However, Estee Lauder expects to witness tariff-related hurdles to the tune of roughly $100 million for the fiscal year, underscoring that EL is not immune to trade pressures.

ELF’s Stock Price Performance, Valuation & Estimates

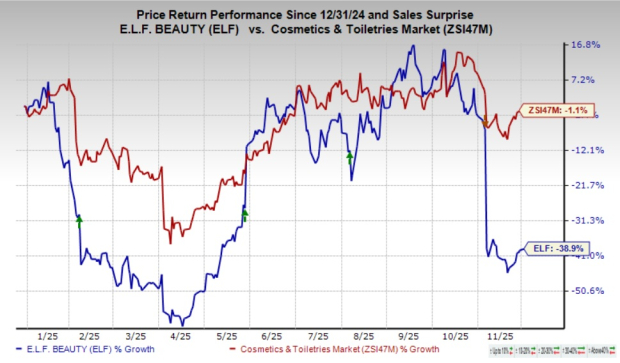

Shares of e.l.f. Beauty have plunged 38.9% year to date compared with the industry’s decline of 1.1%.

ELF Price Performance Versus Industry

Image Source: Zacks Investment Research

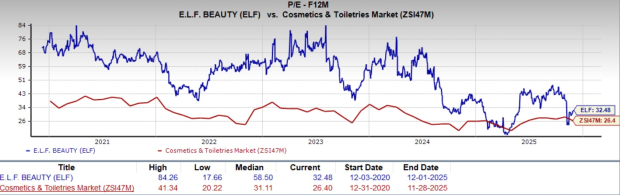

From a valuation standpoint, e.l.f. Beauty trades at a forward price-to-earnings ratio of 32.48, higher than the industry’s average of 26.4.

ELF’s Valuation Compared to Industry

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for ELF’s fiscal 2026 earnings implies a year-over-year decline of 13.6%, while the consensus mark for fiscal 2027 calls for 27.3% growth.

e.l.f. Beauty currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThe Estee Lauder Companies Inc. (EL) : Free Stock Analysis Report

Coty (COTY) : Free Stock Analysis Report

e.l.f. Beauty (ELF) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.