Credit: Shutterstock photo

Credit: Shutterstock photoChristopher Holt submits:

Here's a stocking stuffer for you. Just in time for Christmas, the ECB has released its semi-annual Financial Stability Review . According to the Bank, the world may not actually be coming to an end. In fact, Santa seems to be about to reward mega-financial institutions.

Writes the ECB:

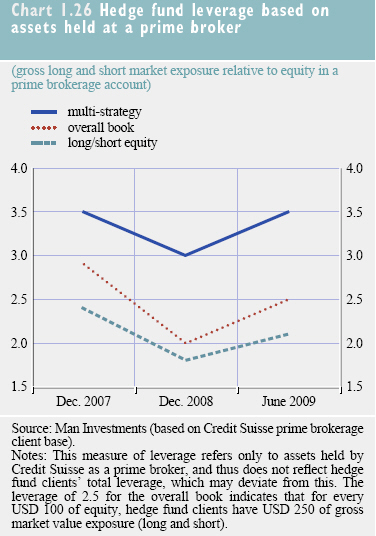

Cynics might suspect that Santa maybe got his "naughty" and "nice" lists mixed up - or that some kind of evil "Anti-Santa" sneaked into Santa's workshop and added a few names to the "good" rolls. But one of the reasons these behemoths are getting a break this season is surely the good fortunes of their clients - hedge funds (see chart right - click to enlarge).

As you can see, the leverage levels in this chart are noticeably higher than those reported in the Bank's other main source, Merrill's Global Fund Manager Survey, in which the vast majority of fund report leverage levels under 2x. Could it be that managers forget some of their leverage when surveyed?…

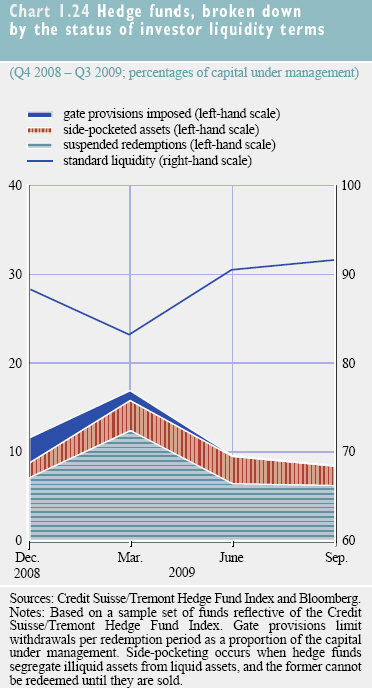

The ECB also finds that redemption gates imposed by managers to prevent a run on their funds may have completed their useful life. Gates, defined by the ECB as metered (not suspended) redemptions seem to have been wound down as all the investors who wanted to exit through these turnstiles have now done so. Side pockets remain in smaller amounts and the AUM caught in suspended animation has remained stable over the past quarter (see chart right- click to enlarge).

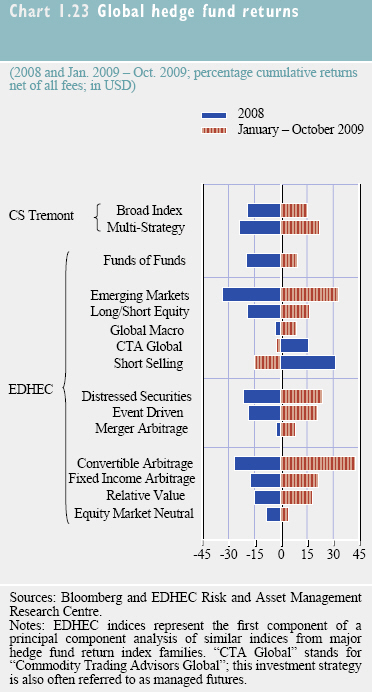

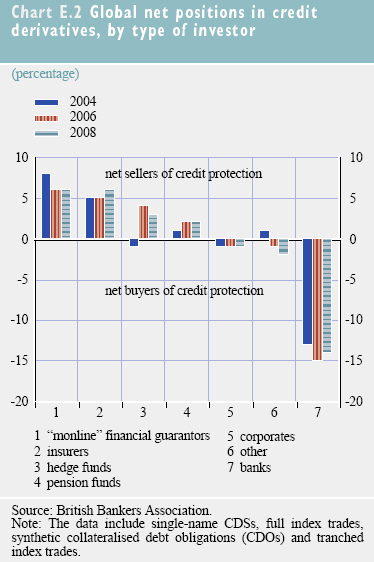

Hedge Funds: Minor credit derivatives players

Convert Arb Beta

For some hedge funds, alternative beta can be the crack cocaine of return generation. Sometime disguised as alpha, alternative beta can be levered to produce a high in the good times - and

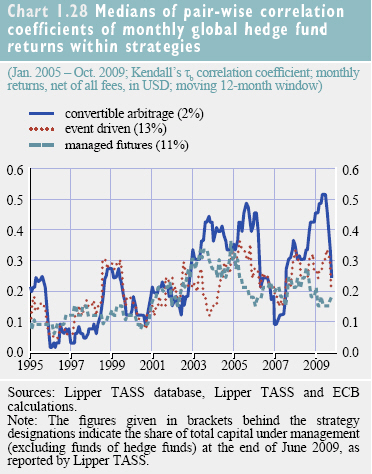

With that in mind, convert arb has its share of "users". The chart at right shows that convert arb pair-wise correlation has shown some dramatic upticks in recent years - upticks that are ticking up higher and higher with each beta binge.

See also San Francisco, Minneapolis Housing Up 15% From Lows on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}