DraftKings Inc. DKNG delivered a standout profitability inflection in fourth-quarter 2025, with adjusted EBITDA margin expanding to 17%, up more than 1,000 basis points year over year. This improvement reflects a combination of stronger structural margins, disciplined promotional spending and favorable sports outcomes. However, the key question for investors is whether this level is sustainable or nearing a peak.

A major driver behind the margin expansion is the company’s improving revenue mix. Higher parlay penetration, which carries structurally better margins, continues to lift sportsbook profitability. Additionally, advancements in pricing models and AI-driven marketing are helping DraftKings optimize customer acquisition and retention, leading to better lifetime value and lower promotional inefficiencies. These structural levers suggest that a portion of the margin gains is durable rather than cyclical.

That said, not all tailwinds are permanent. Management acknowledged that short-term factors like favorable sports outcomes and elevated hold rates can boost margins but introduce volatility over time. As outcomes normalize, some pressure on margins is expected. Moreover, the company is entering an investment phase, particularly in its emerging “Predictions” vertical, where upfront marketing and product investments could weigh on near-term profitability.

Importantly, DraftKings’ 2026 guidance implies continued EBITDA growth but with a wider range, reflecting both reinvestment and inherent variability in the business. While the 17% margin may not represent a steady baseline, the company’s structural improvements indicate it can sustain margins at a meaningfully higher level than in prior years.

In essence, DKNG’s margin story is evolving from cyclical gains to a more durable framework, but investors should expect some moderation as growth investments ramp up.

Competitive Landscape: FanDuel and BetMGM Intensify Margin Race

DraftKings’ margin expansion comes amid strong competition from Flutter Entertainment plc FLUT, the parent of FanDuel, and BetMGM, backed by MGM Resorts International MGM and Entain plc.

FanDuel remains the industry benchmark, leveraging scale, advanced pricing models and a rich parlay mix to deliver consistent profitability. Its disciplined promotional approach aligns with DraftKings’ strategy, reinforcing a broader industry shift toward margin optimization.

BetMGM, while still scaling profitability, is narrowing losses through reduced promotions and improved player monetization. However, it continues to lag in proprietary technology and product integration compared with DraftKings and FanDuel.

Overall, while DraftKings’ 17% EBITDA margin is impressive, sustaining it will depend on execution, as competitors with strong backing and improving efficiency continue to close the gap.

DKNG’s Price Performance, Valuation & Estimates

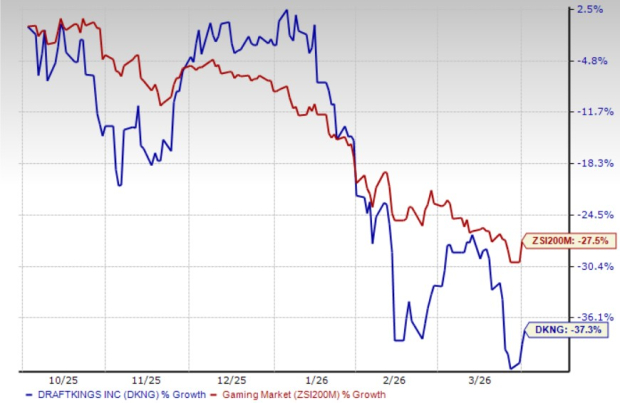

Shares of DKNG have lost 37.3% in the past six months compared with the industry’s decrease of 27.5%.

Price Performance

Image Source: Zacks Investment Research

DraftKings is currently trading at a discount compared with the industry, with a forward 12-month price-to-sales ratio of 1.56.

P/S (F12M)

Image Source: Zacks Investment Research

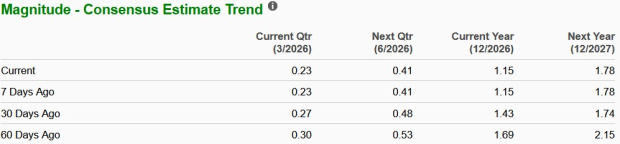

The Zacks Consensus Estimate for DKNG’s 2026 and 2027 earnings estimates has declined sharply in the past 60 days.

Image Source: Zacks Investment Research

DKNG currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeMGM Resorts International (MGM) : Free Stock Analysis Report

DraftKings Inc. (DKNG) : Free Stock Analysis Report

Flutter Entertainment PLC (FLUT) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.