Dover Corporation DOV has reported third-quarter 2025 adjusted earnings per share (EPS) from continuing operations of $2.62, beating the Zacks Consensus Estimate of $2.50. In the year-ago quarter, the company reported an adjusted EPS of $2.27. On a reported basis, Dover has delivered an EPS (from continuing operations) of $2.20 in the quarter, down 3% year over year.

Total revenues in the third quarter were $2.08 billion, up 4.8% from the year-ago quarter. The top line missed the Zacks Consensus Estimate of $2.09 billion. Organic growth was 0.5% in the quarter.

Dover Corporation Price, Consensus and EPS Surprise

Dover Corporation price-consensus-eps-surprise-chart | Dover Corporation Quote

DOV’s Margins Rose Y/Y in Q3

The cost of sales rose 2% year over year to $1.24 billion in the reported quarter. Gross profit was up 9.2% year over year to $834 million. The gross margin was 40.1% compared with the year-ago quarter’s 38.5%.

Selling, general and administrative expenses grew 6.3% to $456 million from the prior-year quarter. Adjusted EBITDA rose 12% year over year to $543 million. The adjusted EBITDA margin was 26.1% in the quarter compared with the prior-year quarter’s 24.4%.

Dover’s Q3 Segmental Performances

The Engineered Products segment’s revenues were down 5.5% year over year to $280 million in the quarter. The reported figure fell short of our estimate of $293 million. The segment’s adjusted EBITDA increased 2.9% year over year to $63 million. The figure beat our estimate of $61 million.

The Clean Energy & Fueling segment’s revenues were $541 million compared with the prior-year quarter’s $501 million. The figure beat our estimate of $538 million. The segment’s adjusted EBITDA was $127 million, up from the prior-year quarter’s $108 million. The figure topped our estimate of $115 million.

The Imaging & Identification segment’s revenues moved up 5.3% year over year to $299 million. The reported figure beat our estimates of $284 million. The segment’s adjusted EBITDA was $86 million, up from the year-ago quarter’s $81 million. The figure beat our estimate of $84 million.

The Pumps & Process Solutions segment’s revenues rose 16.6% year over year to $551 million in the third quarter and surpassed our estimate of $516 million. The adjusted EBITDA of the segment totaled $183 million, up 21.1% from the year-ago quarter’s $151 million. The reported figure beat our projection of $172 million.

The Climate & Sustainability Technologies segment’s revenues fell 5.2% to $409 million from $431 million in the year-earlier quarter. We had predicted revenues of $455 million for this segment. The segment’s adjusted EBITDA totaled $83.6 million compared with $83.1 million in third-quarter 2024. The figure was lower than our estimate of $87 million.

DOV’s Bookings Rose Y/Y in Q3

Dover’s bookings at the end of the third quarter were around $2 billion compared with the prior-year quarter’s $1.85 billion. Total booking missed our estimate of $1.97 billion.

Dover’s Q3 Financial Position

The company had a free cash inflow of $370 million in the third quarter compared with the year-ago quarter’s $315 million. Cash flow from operations amounted to $424 million in the quarter under review compared with the prior-year quarter’s $353 million.

DOV’s 2025 Outlook

Backed by solid end-market demand, the company raised its 2025 outlook. It has raised the adjusted EPS view to $9.50-$9.60 for 2025 from $9.35-$9.55. The company anticipates year-over-year revenue growth of 4-6%.

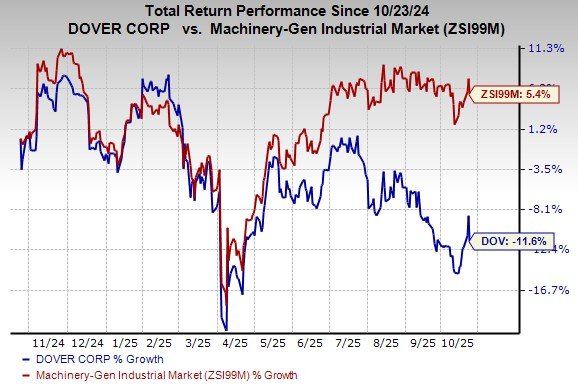

Dover Stock’s Price Performance

Dover’s shares have lost 11.6% in the past year against the industry’s 5.4% growth.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

DOV’s Zacks Rank

Dover currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Dover’s Peer Q3 Performance

Graco Inc. GGG reported adjusted EPS of 73 cents in third-quarter 2025, which missed the Zacks Consensus Estimate of 75 cents. The bottom rose 3% year over year.

Revenues increased 4.6% year over year to $543 million. The top line missed the Zacks Consensus Estimate of $562 million.

Manufacturing Stocks Awaiting Results

Flowserve Corporation FLS is scheduled to release its third-quarter 2025 results on Oct. 28. The Zacks Consensus Estimate for Flowserve’s third-quarter 2025 earnings is pegged at 80 cents per share, suggesting year-over-year growth of 29%.

The Zacks Consensus Estimate for Flowserve’s top line is pegged at $1.21 billion, indicating an increase of 6.6% from the prior year’s actual. FLS has a trailing four-quarter average surprise of 5.5%.

Crane Company CR, scheduled to release third-quarter 2025 results on Oct. 27, has a trailing four-quarter average surprise of 7.5%. The Zacks Consensus Estimate for Crane’s third-quarter 2025 earnings is pegged at $1.46 per share, suggesting year-over-year growth of 5.8%.

The Zacks Consensus Estimate for Crane’s top line is pegged at $576 million, indicating a decrease of 3.5% from the prior-year reported figure.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Dover Corporation (DOV) : Free Stock Analysis Report

Flowserve Corporation (FLS) : Free Stock Analysis Report

Graco Inc. (GGG) : Free Stock Analysis Report

Crane Company (CR) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.