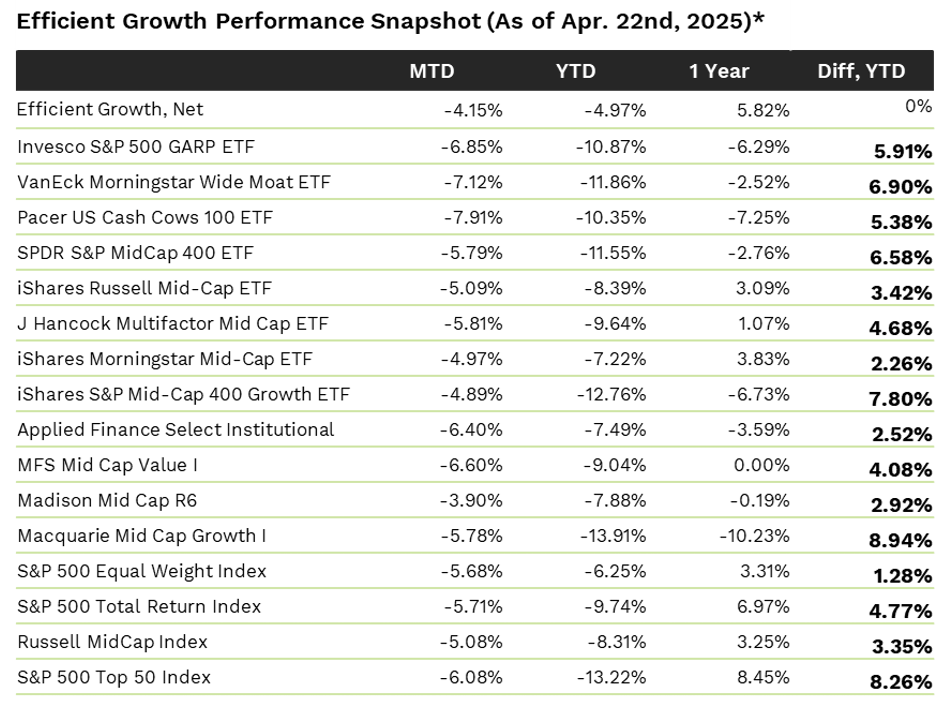

Running Oak's Efficient Growth portfolio has delivered precisely what we said it would. It outperformed EVERY SINGLE benchmark and peer (that we follow), ytd, coming into today. Efficient Growth had outperformed the S&P 500 by 4.77%, the S&P Equal Weight by 1.28%, and the Russell Mid Cap by 3.35%, gross of fees.*

Most importantly, Efficient Growth has delivered roughly 50% of the downside of the S&P 500, ytd. Since 1989, Efficient Growth delivered roughly 50% of the downside of the S&P 500.* For the last 4 months AND 35 years, Efficient Growth has been consistent and reliable. Invest in a strategy you can depend upon. Hope is insufficient.

Why Invest in Efficient Growth:

- Top 2 percentile: Running Oak’s Efficient Growth separate account has performed in the top 2% of all Mid Cap Core funds in Morningstar's database over the last 10 years, net of fees.1

- Opportune: A little known - yet very large - hole exists in the typical equity portfolio, precisely where the most attractive risk/reward asymmetry currently lies. Efficient Growth fills that hole - and opportunity - like few portfolios do.

- 5 Stars: Efficient Growth has a 5-Star Morningstar rating.

- Since inception, Efficient Growth has provided 25% more return than the S&P 500 Equal Weight Index and 7% more return than the S&P 500 Total Return Index, given the same level of downside risk, gross of fees. (Ulcer Performance Index)*

Differentiated Approach and Construction

- Mid Cap stocks are at their cheapest in 25 years relative to Large. Efficient Growth provides significant Mid Cap exposure.

- Efficient Growth is built upon 3 longstanding, common sense principles: maximize earnings growth, strictly avoid inflated valuations, protect to the downside.

- Running Oak utilizes a highly disciplined, rules-based process, resulting in a portfolio that is reliable, repeatable, and unemotional.

How to Invest

- Efficient Growth is currently available as an SMA and ETF. (ETF specifics and SMA historical performance can't be shared in the same letter - sorry, it's annoying, I know. Please inquire for the ticker or more information.)

- In just 21 months, The ETF Which Shall Not Be Named has grown over 15,000% since launch - from 2 to 310mm - despite the recent market decline.

"Common sense is like deodorant. The people who need it most never use it." – Anonymous

For 8 years, I have been waiting for a time when numbers, once again, matter and investors, once again, think. If this is, in fact, the return of common sense, thought, reality, and portfolio deodorant, our year-to-date outperformance likely provides a glimpse of the next 10 years.

For far too long, people have indiscriminately bought every dip, driven by a pervasive narrative of “the market always goes up in the long run.” (Notice “long run” is never defined.) The Fed or US government – not the economy, itself – has stepped in and pushed equities right back up, reaffirming that half-baked narrative, leading to a widely-held, errant belief of many.

Years of this back and forth – the market goes down; it’s manipulated back up (QE2); the market goes down; it’s manipulated back up (QE3); the market goes down; Powell caves in 2018; the market goes down; the Fed cuts rates to 0 (and QE4 and $1T in stimulus), and so on – has reinforced a dogma of “Buy the dip. Never sell. The market always goes up. You can’t lose.” It’s happening again today via social post.

And if you can’t lose, why think? In fact, thinking and discipline would have hurt you over the last decade. Many investors stopped buying deodorant and adopted the belief that their aggrieved olfactory cortexes were liars.

“Do you smell that?”

“Nope.”

Efficient Growth kept up with the S&P 500 over the last decade+, but it was an outlier; 95% of thinkers underperformed. Thus, equity investing evolved into a thoughtless exercise. But when in life is it best to not think? Our clients work day in and day out, week in and week out, year in and year out; the least we can do is steward that money thoughtfully and make an effort to protect it.

“You miss 100% of the deodorant you don’t apply.” — Someone in a crowded elevator

Complacency - a feeling of quiet pleasure or security, often while unaware of some potential danger or defect

The Complacency Bubble is in the beginning stages of popping. Equity investors are very slowly becoming aware of the defect in buying without thinking and the dangers of investing in overvalued companies, i.e., companies that should go down.

The end of a bear market is marked by night terrors of buying the dip, not record inflows into leveraged Tech ETFs. Per BTIG, retail investors piled into TQQQ and SOXL last week.

"Puberty teaches you two things: emotions are weird, and deodorant is not optional."

The world is changing rapidly; it’s going to get weird and uncomfortable, like a teenager.

A summary of where we’ve been, what’s changing, and where we’re likely going would take hours. Here’s a brief oversimplification, instead.

Where We’ve Been

- The Fed Put has saved the day for almost 4 decades.

- Globalization like nothing seen in history drove growth and historically high profit margins for decades.

- Massive government deficits have funded growth since 2008, not a vibrant, healthy economy.

- Inflation recently spiked to a level not seen since 1981.

What’s Changing

- The highest tariffs since the 1930s were recently announced, then paused, then escalated, then…

- Recent tariffs led to the highest spike in inflation expectations since the early 80s.

- Despite one of the five largest crashes in equity history, bonds went down. (Yields went up. That’s a significant divergence from historical norms.)

- Consumer Confidence is at its lowest level since 1990.

Where We’re Likely Going

- Higher Rates for Longer: Because of recent inflation, the stickiness of inflation, inflation expectations, and the potential inflationary impact of tariffs, the Fed CAN’T LOWER RATES. Inflation, not recessions, is the greatest risk to a political system.

- Stagflation: Inflation meets recession. This currently appears to be the most likely outcome.

- RIP Fed Put: No ZIRP this time. (Zero Interest Rate Policy - 0%)

- Lower Corporate Profit Margins: Deglobalization means lower profit margins.

*Notice the upward slope over the years of globalization. This will reverse.

Maybe Most Critically – Higher Rates for Good (Meaning for Bad)

There has been a great deal of talk about trade deficits. Trade deficits are neither good nor bad. They can be either. Here’s a drastically oversimplified illustration of the good. (Note: There’s also bad.)

- China makes stuff cheaply.

- Americans buy more stuff, because they pay less for the stuff.

- Americans buy stuff with dollars.

- The Chinese sell stuff for dollars.

- The Chinese buy US Treasuries with those dollars.

- More dollars for US Treasuries mean lower yields.

- Lower yields mean lower rates. Mortgages are lower; housing is more affordable; growth is higher; valuations are higher, etc.

- Now, reverse that.

(Note: The Chinese have behaved badly for many years, manipulating their currency lower, IP theft, etc. As is the case with most things in life, it isn’t a black or white dynamic.)

Complacency Bubble, Part II

High valuations require a low regard for risk or, in other words, complacency. If complacency evaporates, high valuations do, too. Here are 2 simple and obvious examples.

Apple is trading at over 2x its long-term valuation, despite FAR LESS cash and FAR LESS growth.

Below illustrates what a moderate reversion to the mean implies. Note that both the P/E and Profit Margin in the table are optimistic - a 62% decline, based upon optimistic metrics.

TESLA

Were Tesla to go from a meme stock that is completely untethered from reality to just meaningfully overvalued, here’s what that would imply.

“I trust my deodorant more than I trust most people.”

Trust in math. Lower drawdowns have an outsized impact on higher compound returns. Tesla and Apple are just two obvious examples of prime candidates for reversion to the mean. Their limited upside doesn’t justify their very significant downside. Portfolios that indiscriminately (index funds) – or intentionally (Large Cap Growth) – own a significant percentage of these two stocks are playing with grenades.

“Natural deodorant: because smelling like a salad is still better than regret.”

Common Sense – The investment philosophy of

- Maximize Earnings Growth

- Don’t Pay a Stupid Price

- Lessen Drawdowns

just naturally makes sense, and Running Oak is herbaceous. Belief without understanding crumbles under duress, leading to "Sell it all!" calls from clients at inopportune times. Trust in what you can understand; your clients will.

“Deodorant is like a good friend — always there when things start to stink.”

Our rules-based investment process is highly disciplined, ensuring that we consistently aren’t stupid. Running Oak invests in profitable, high growth, attractively valued companies with lower debt levels repeatedly and reliably.

"Skipping deodorant is a bold strategy. Let’s see how that plays out."

Spoiler alert: it won't turn out well. NOW is the time to make a change and position for an uncertain future and a decade likely to be very different from the last. If you have losses, realize them. If you have gains, take advantage of the current dead cat bounce in the most crowded trades in history: the Magnificent 7, index funds, and Large Cap Growth. The economic and market environment have changed dramatically. Portfolios should probably change, too. (That was facetious.)

Mid Cap Reminder - Mid Cap stocks have outperformed Large Cap by 60bps over the last 33 years, AND they’re cheaper, AND they’re under-invested. The typical equity investor is woefully underinvested in upper Mid Cap and lower Large Cap (MARGE), in particular. Efficient Growth fills that gap like few strategies do, providing value like even fewer do.

Running Oak's goal is to maximize the exponential growth of clients' portfolios, while subjecting them to far less risk of loss. In other words, we aim to help your clients realize their dreams and avoid their nightmares.

If you appreciate critical thinking, math, common sense, and occasional sarcasm, we would love to speak with you. Please feel free to set up a time here: Schedule a call.

Seth L. Cogswell

Founder and Managing Partner

Edina, MN 55424

P +1 919.656.3712

For additional data and context regarding the claims made within this letter, please refer to the Disclosures and Additional Data document located here.

“All opinions expressed in this newsletter are those of Running Oak Capital’s and do not constitute investment advice.”

Investment Advisory Services are offered through Running Oak Capital, a registered investment adviser.

*Past performance is no guarantee of future results. Performance expectations are no guarantee of future results; they reflect educated guesses that may or may not come to fruition. All indices are unmanaged and may not be invested into directly.

*YTD performance through 4/22/2025 is reflective of a representative account within the Efficient Growth composite of which is substantially similar and has performed closely in-line with broader composite returns historically.

*Statements reflect the opinion of Running Oak Capital on the average investor’s equity portfolio allocation. This is based on informal feedback and experience from interactions with investors and other financial professionals.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments and strategies may be appropriate for you, consult with us at Running Oak Capital or another trusted investment adviser.

Stock prices and index returns provided by Standard & Poor’s.

Latest articles

This data feed is not available at this time.

Data is currently not available