Tax cuts' appeal is obvious: more money for the same effort. But proponents don't usually leave it at that. At a Sept. 27 rally celebrating the release of the Republican's "Unified Framework" for federal tax reform (which soon splintered into deeply divergent House and Senate bills), President Donald Trump predicted that economic growth "takes off like a rocket ship."

The day after Trump's speech, Treasury secretary Steven Mnuchin told CBS' Major Garrett, "Not only will this tax plan pay for itself, but it will pay down debt,” around $1 trillion worth over 10 years.

Is any of this true? Do tax cuts generally — particularly the kinds of cuts the House has passed and the Senate is mulling specifically — accelerate growth? Do they pay for themselves?

Do tax cuts pay for themselves?

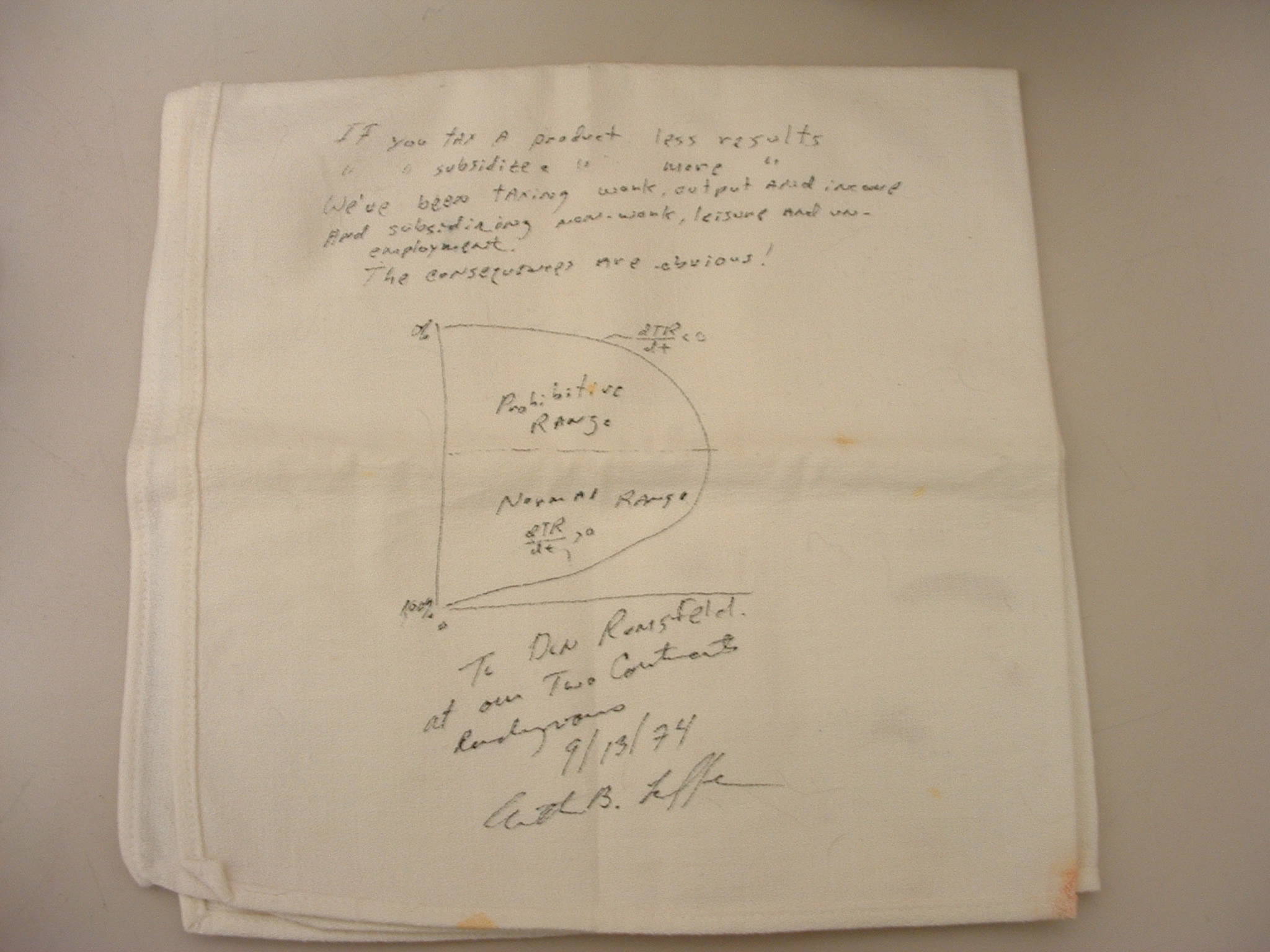

Take the second question first. Prior to 1974, no one, Republican or Democrat, believed that cutting taxes would increase government revenue. No one, that is, but economist Arthur Laffer, who sketched what turned out to be the Keynesian consensus' death certificate on a cocktail napkin during an afternoon meeting with Dick Cheney, at the time Gerald Ford's deputy chief of staff; Jude Wanniski, an associate editor at the Wall Street Journal; and Grace-Marie Arnett, who would serve as the Ford campaign's deputy press secretary. (Accounts of the meeting differ. The above is based on Wanniski's 2005 retelling.)

{kind=link}

The Laffer curve, as Wanniski dubbed the illustration, graphs the theoretical relationship between income tax rates and government revenues. At 0% and 100% tax rates, the government gets nothing: at 0% because it doesn't try, and at 100% because no one else does (faced with the prospect of handing over every cent of income, the labor force stays home). Somewhere between these two extremes lies the tax rate that generates the maximum amount of government revenue.

No one disputes these basic premises, which boil down to the law of diminishing returns. But nearly every economist disputes Laffer's conclusion — which Mnuchin shares — that cutting taxes from their actual levels (in 1974 or 2017) would bring the government closer to maximizing revenue. Most reckon that Uncle Sam tops out at some significantly steeper rate than the current 14.2%.

In 2012 Chicago Booth's Initiative on Global Markets asked 40 prominent economists how they felt about the following statement: "A cut in federal income tax rates in the US right now would raise taxable income enough so that the annual total tax revenue would be higher within five years than without the tax cut." Is Laffer right? Not one of the respondents agreed. About a third plain-old disagreed, while 38% did so strongly. A handful said "uncertain" or "no opinion." Weighted by the confidence the respondents expressed in their answers, "strongly disagree" won a clear majority.

The University of Chicago's Richard Thaler appended a comment summing up the consensus: "That's a Laffer!"

Would the GOP bills pay for themselves?

As for the Republican tax bills currently making their way through Congress, the most generous estimate available — outside of Mnuchin's— is that the House version would reduce federal revenues by $1.98 trillion over a decade and make $0.9 trillion of it back by boosting growth; the Senate version scores worse. Those estimates come from the Tax Foundation, a right-leaning think tank that makes the not-uncontroversial assumption that workers bear 70% of corporate taxes. The Treasury put the figure at 18% until this summer, when the relevant research disappeared from its website.

At the time of writing, Senate Republicans are discussing "trigger" clauses that would automatically hike taxes or cut spending if their plan fails to pay for itself.

Do tax cuts accelerate growth?

The idea that tax cuts boost growth enough to pay for themselves and then some is rejected by economists, including the ones who work at conservative think tanks. But do they boost growth at all?

Here the consensus breaks down. The 2012 survey put the question to the same 40 economists who panned the Laffer curve: "A cut in federal income tax rates in the US right now would lead to higher GDP within five years than without the tax cut." Just over a third agreed, just over a third were uncertain, and 8% disagreed or strongly disagreed. Weighted by confidence, uncertainty ruled the day.

"There wasn't enough information with which to answer," Claudia Goldin, a Harvard economics professor who responded "uncertain," told me recently via email. "How big a cut? On whom? What would happen to expenditures?"

Fair points. Forecasting the effects of "a cut" — any old cut — is tricky. In 2005 the Congressional Budget Office (CBO) gave it a go, working out the macroeconomics effects of as generic a tax reduction as they could come up with: all federal individual income tax rates (AMT, long-term capital gains and dividends included) fall by 10%, so that what was the 25% bracket is now 22.5%, and so on.

The CBO had to wrestle with some thorny questions to forecast the effect on growth. Take labor, for example: lower rates mean workers can make the same after-tax income with fewer hours of labor, so the cut would tend to decrease hours worked. On the other hand, each additional hour worked generates more after-tax income than before, so there's an incentive to work more, increasing overall output. The higher returns on hours worked could also make the difference for potential secondary earners, drawing more bodies into the labor force. On balance, the CBO reckons, tax cuts boost hours worked.

All told, the CBO estimated that output could increase by 0.5% to 0.8% over the first five years, and shrink by 0.1% in the second five — or grow by 1.1%. The findings offer a tepid endorsement of tax cuts similar to that of the economists surveyed in 2012. They probably boost growth a bit, except it depends, and really we're not sure.

Would the GOP bills accelerate growth?

As for the specific GOP tax bills under consideration, things are a bit clearer. The Initiative on Global Markets polled roughly the same sample of economists again on Nov. 21 of this year and asked them about the proposals' likely effects.

Almost no one thought they would boost GDP growth. A healthy chunk were uncertain, but the majority disagreed, strongly or otherwise, with the statement: "If the US enacts a tax bill similar to those currently moving through the House and Senate — and assuming no other changes in tax or spending policy — US GDP will be substantially higher a decade from now than under the status quo."

It is worth hearing the one "agree" make his case. Darrell Duffie, professor of finance at Stanford, wrote that a "corporate tax reduction is likely to grow GDP. Whether the overall tax plan is distributionally fair is another matter."

About that. According to a CBO analysis released Sunday, the Senate bill would cost the federal government $234.0 billion in 2019, as taxpayers earning $30,000 or more receive a $236.5 billion break. Those making less than $30,000 would make up the difference with a $2.6 billion tax hike. In 2027 the federal government would earn $40.1 billion above baseline: those earning more than $75,000 would get a $22.9 billion cut, while those earning less would get a $50.7 billion hike.

There is more than distributional fairness at work here. The Senate bill, if it becomes law, may stunt growth precisely because of this reverse-Robin Hood effect.

Janet Currie, who chairs Princeton's economics department, told me via email, "The effects of an income tax on growth depend on whether more money goes into the pockets of people who have high propensities to consume out of income." In other words, because low earners are more likely to spend any additional money they earn (or don't pay in taxes), the most straightforward way to boost growth is to cut taxes for the lowest-income households.

But that's not what the bill would do. Currie writes: "I think a lot of lower income people will see little if any reduction in taxes from this bill and that some will actually face tax increases. The big beneficiaries will be higher income people who may not have a high propensity to consume out of additional income." Give a rich person a dollar, and they will spend a relatively small portion of it on goods and services; they're more likely to invest it in an asset or leave it in cash.

So will the GOP bills, as written, boost growth? "I have doubts," says Currie.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

David Floyd

David Floyd is an Atlanta native and a Kenyon alum living in Brooklyn. He writes about the intersections of investing, politics, energy and international relations. His work also appears at Investopedia.

Read David's Bio