Devon Energy Corporation DVN is expected to report a year-over-year decline in its top and bottom lines when it reports third-quarter 2024 results on Nov. 5, after the market close.

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

The Zacks Consensus Estimate for DVN’s third-quarter revenues is pegged at $3.86 billion, indicating a 2% decline from the year-ago reported figure.

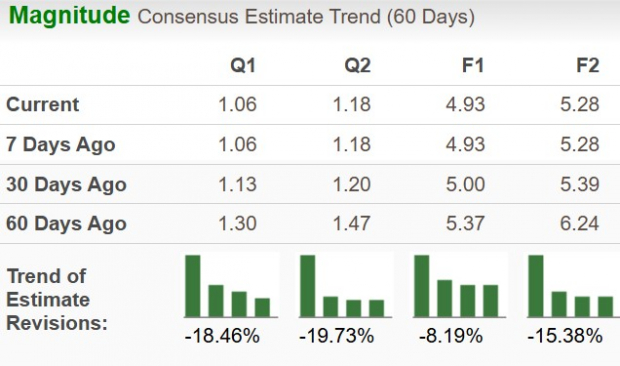

The consensus estimate for earnings is pegged at $1.06 per share. The Zacks Consensus Estimate for DVN’s third-quarter earnings has declined 18.46% in the past 60 days. The estimate suggests a year-over-year decline of 35.8%.

Image Source: Zacks Investment Research

Solid Earnings Surprise History

Devon’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 5.49%.

Image Source: Zacks Investment Research

What the Zacks Model Unveils

Our proven model does not conclusively predict an earnings beat for Devon Energy this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. That is not the case here, as you can see below.

You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Earnings ESP: Devon has an Earnings ESP of -0.70%.

Zacks Rank: Devon Energy currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Likely to Have Shaped DVN’s Q2 Earnings

Devon continues to benefit from its multi-basin portfolio and high-margin assets. Increased productivity from the wells placed online during the first nine months of 2024 is likely to have been a primary contributor to strong production volumes. The acquisition of Grayson Mill Energy during the quarter is going to boost the company’s production volumes.

Third-quarter earnings are expected to have benefited from effective cost management, which is likely to keep operating expenses within the guidance level and boost margins. Devon also achieved prominent operational efficiencies in Delaware in the first half of 2024, which is expected to have continued in the third quarter as well, boosting the performance of the company.

Stable free cash flow generation is expected to have continued in the third quarter as well, which assisted in increasing shareholders’ value. The ongoing share repurchases have lowered the shares outstanding level of the company, which is likely to have had a positive impact on third-quarter earnings.

DVN’s Price Performance and Valuation

DVN’s shares have declined 23.2% in the past six months compared with the industry’s drop of 5.1%.

Image Source: Zacks Investment Research

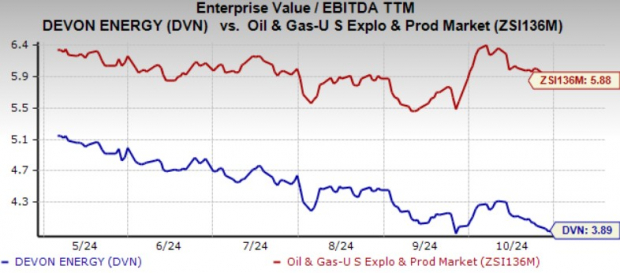

Devon shares are somewhat inexpensive on a relative basis, with its current trailing 12-month Enterprise Value/Earnings before Interest Tax Depreciation and Amortization (EV/EBITDA TTM) being 3.89X compared with its industry average of 5.88X.

Image Source: Zacks Investment Research

Some of the other operators in the same space, like APA Corporation APA and EOG Resources Inc. EOG, are trading at a higher value compared with Devon. The shares of APA and EOG are trading at current trailing 12-months EV/EBITDA multiple of 5.42 and 5.13, respectively.

Investment Thesis

The highly productive multi-basin domestic assets of Devon are the primary contributor to its strong performance. The company’s acquisition of Grayson Mill Energy will enable it to maintain high-margin production and strong free cash flow for years. Devon has significant financial flexibility and has been reducing its debt and lowering its annual interest expenses.

The company’s current ratio stands at 1.11, indicating its financial strength to meet near-term debt obligations. In addition, the drop in interest rates is going to have a positive impact, as it will lower the borrowing costs for long-term projects.

A highly competitive oil and gas industry may limit the company’s capacity to apply for new drilling rights or acquire properties due to competitors who are financially stronger than Devon with more resources at their disposal.

To Sum Up

Devon’s high-quality domestic assets with a balanced exposure to oil, natural gas and NGL production and its low-cost production structure boost margins. The company is presently trading at a discount.

Those who already own this stock would do well to retain it in their portfolio.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpDevon Energy Corporation (DVN) : Free Stock Analysis Report

APA Corporation (APA) : Free Stock Analysis Report

EOG Resources, Inc. (EOG) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.