Investors just got another lackluster earnings report from industrial conglomerate 3M (NYSE: MMM). While the stock has undoubtedly sold off in recent years due to its growing legal risks, the company has also disappointed investors with its operational performance. It's the latter I'd like to focus on in this article.

There's a value case to be made for 3M, and a nearly 5% dividend yield is nothing to sneeze at, too. Still, it's not enough to make the stock a buy. Here's why.

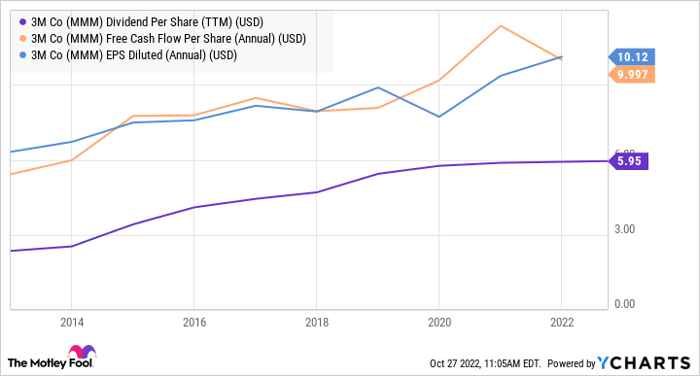

A mature industrial conglomerate

Most companies tend to grow in a similar, evolutionary pattern. First, there's fast growth and possibly a loss-making stage, leading to a profitability and moderate growth stage. Then there's maturity, which is characterized by revenue growth in line with the gross domestic product (GDP) combined with sound earnings generation.

3M is a mature industrial conglomerate. It has broad exposure to the economy at large through its four business segments: safety and industrial, transportation and electronics, healthcare, and consumer products. The company does also face substantive legal issues, but here I'm going to focus on its underlying business.

The company generates substantial earnings and free cash flow (FCF) from which it can sustain a dividend that currently generates a yield of nearly 5%. If you are an investor heavily focused on dividends, then it makes sense to look closely at 3M.

Data by YCharts

Struggling for revenue growth

That said, 3M is not a company that will attract investors looking for growth, because the company has struggled to deliver it in recent years. There's the standout year of 2021, but recall that 3M benefited from respirator sales that year. Otherwise, it's been a pretty mediocre period for the company.

|

3M |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 Est. |

|---|---|---|---|---|---|---|---|---|

|

Organic, local currency revenue growth |

1.3% |

(0.1%) |

5.2% |

3% |

(1.5%) |

(1.7%) |

8.8% |

1.5%-2% |

Data source: 3M presentations.

Furthermore, the guidance for 2022 implies more of the same. Mature industrial companies tend to benchmark themselves against GDP growth or the industrial production index (IPI). Unfortunately, 3M's revenue performance is struggling against these benchmarks. For example, management expects IPI and GDP growth of 3% for 2022 versus 3M's forecast for organic sales growth of 1.5% to 2% this year.

What about margin growth?

If 3M finds it hard to escape the comparison to GDP and industrial production growth, then the answer probably lies in expanding profit margins. Unfortunately, that's also something 3M has struggled to do.

Presumably, this was on the mind of Barclays analyst Julian Mitchell when he asked management about margin prospects for 2023: "3M as a whole has been at that sort of 21%, 22% range for four years or five years now. It's been a couple of years since the last big kind of restructuring announcement in December 2020."

Mitchell is referring to operating margin, but a quick look at adjusted earnings before interest, taxation, depreciation, and amortization (EBITDA) margin performance shows a similarly disappointing performance. 3M's EBITDA margin for the first nine months was down to 26.6% from 28.1% in the same period last year.

The answer doesn't lie in pricing per se. 3M has increased pricing to offset cost increases in 2022, but management typically relies on volume growth rather than pricing to generate margin expansion. 3M no longer breaks out pricing in its earnings presentations, but CFO Monish Patolawala was clear on theearnings callthat management took a "very thoughtful" approach to pricing. This is because 3M prefers to generate margin growth through volume expansion. However, a glass-half-empty view sees that 3M doesn't have the pricing power to hike prices without hurting volume growth.

What it all means to investors

It appears that 3M is struggling to increase revenue and margins and doesn't have the pricing power to change matters anytime soon. Moreover, the restructuring actions taken in the last few years have yet to result in significant margin expansion; the recent results saw pressure on its healthcare and consumer businesses from a slowing economy.

It's not a formula that will likely attract investors who like growth stocks. Until 3M can demonstrate an ability to grow earnings via revenue growth and margin expansion, 3M is a stock only for income-seeking investors.

10 stocks we like better than 3M

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and 3M wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of September 30, 2022

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool recommends 3M and Barclays. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.