CrowdStrike Holdings CRWD stock has been in a downward trajectory over the past three months. Shares of the company have plunged 21.9% over the past three months, underperforming the Zacks Security industry’s decline of 19.2%.

CrowdStrike has also underperformed industry peers, including Fortinet FTNT, Check Point Software CHKP and Okta Inc. OKTA. Shares of Fortinet have inched up 0.2%, while Check Point Software and Okta shares have lost 10.2% and 2.7%, respectively.

3-Month Price Return Performance

Image Source: Zacks Investment Research

This underperformance raises the question: Should investors cut their losses and exit, or is it worth holding CRWD stock?

CrowdStrike Encounters Slowing Sales Growth

Although CrowdStrike has experienced impressive growth since its IPO, recent quarterly reports have shown a deceleration in its growth rate. The company's revenue growth, while still robust, is not as explosive as in previous years.

CrowdStrike had enjoyed more than 35% year-over-year top-line growth till fiscal 2024. However, the growth rate decelerated in fiscal 2025 to 29%. This trend is expected to continue in fiscal 2026.

For fiscal 2026, CrowdStrike expects total revenues to be in the range of $4.797 billion to $4.807 billion, indicating a year-over-year increase of 21% to 22%. The Zacks Consensus Estimate for fiscal 2026 and 2027 suggests that the top-line growth will further decelerate to around 21%.

Image Source: Zacks Investment Research

Rising Costs Hurt CrowdStrike’s Profitability

To survive in the highly competitive cybersecurity market, each player is continuously investing to broaden their capabilities. Investment in research & development (R&D) is a top priority for CrowdStrike. Over the last six fiscals, CrowdStrike’s R&D expenses increased 12-fold to improve the design, architecture, operation and quality of its cloud platform.

Over the past few years, CrowdStrike has invested heavily to enhance its sales and marketing (S&M) capabilities, particularly by increasing the sales force. As a result, CrowdStrike’s S&M expenses increased nearly ninefold to $1.52 billion in fiscal 2025 from $173 million in fiscal 2019.

In the third quarter of fiscal 2026, S&M and R&D expenses soared 20.2% and 23.3%, respectively, year over year. Though the firm foresees these investments generating benefits over the long run, higher expenses are expected to weigh on the company’s bottom-line results.

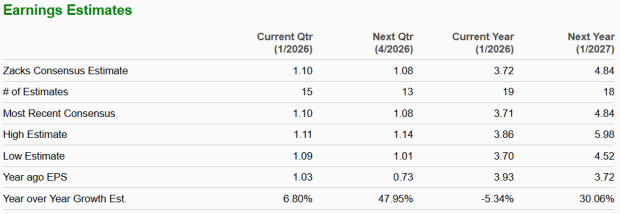

Increasing costs are likely to impact CrowdStrike’s bottom-line performance in fiscal 2026, as reflected in the Zacks Consensus Estimate. The consensus estimate for CRWD’s fiscal 2026 bottom line is pegged at $3.72 per share, indicating a year-over-year decline of 5.3%.

Image Source: Zacks Investment Research

Valuation: CRWD Trades Above Industry and Peers

CrowdStrike is currently trading at a high price-to-sales (P/S) multiple, far above the Zacks Security industry. CrowdStrike’s forward 12-month P/S ratio sits at 22.09X, significantly higher than the Zacks Security industry’s forward 12-month P/S ratio of 11.07X. The Zacks Value Score of F also suggests that CRWD stock is overvalued.

Forward 12 Month P/S Ratio

Image Source: Zacks Investment Research

CRWD stock also trades at a higher P/S multiple compared with other industry peers, including Fortinet, Okta and Check Point Software. At present, Fortinet, Okta and Check Point Software have P/S multiples of 7.8X, 5.02X and 6.58X, respectively.

Key Technical Indicator Signals Bearish Trend for CRWD

CrowdStrike shares have dipped below their 50-day & 200-day moving averages, a bearish technical signal that indicates the potential for continued downward pressure in the short term.

CRWD 50-Day & 200-day Simple Moving Average

Image Source: Zacks Investment Research

Conclusion: Time to Sell CrowdStrike Stock

CrowdStrike’s decelerating sales growth, rising costs and premium valuation warrant a cautious approach to the stock, which makes this Zacks Rank #4 (Sell) stock less attractive in the near term.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpCheck Point Software Technologies Ltd. (CHKP) : Free Stock Analysis Report

Fortinet, Inc. (FTNT) : Free Stock Analysis Report

Okta, Inc. (OKTA) : Free Stock Analysis Report

CrowdStrike (CRWD) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.