Please find Running Oak's most recent performance and letter below.

Why Invest in Efficient Growth:

- Top 3 percentile: Running Oak’s Efficient Growth separate account has performed in the top 3% of all Mid Cap Core funds in Morningstar's database over the last 10 years, net of fees.1

- Opportune: A little known - yet very large - hole exists in the typical equity portfolio, precisely where the most attractive risk/reward asymmetry currently lies. Efficient Growth fills that hole - and opportunity - like few portfolios do.

- 5 Stars: Efficient Growth has a 5-Star Morningstar rating.

- Since inception, Efficient Growth has provided 24% more return than the S&P 500 Equal Weight Index and 4% more return than the S&P 500 Total Return Index, given the same level of downside risk, gross of fees. (Ulcer Performance Index)*

Differentiated Approach and Construction

- Mid Cap stocks are at their cheapest in 25 years relative to Large. Efficient Growth provides significant Mid Cap exposure.

- Efficient Growth is built upon 3 longstanding, common sense principles: maximize earnings growth, strictly avoid inflated valuations, protect to the downside.

- Running Oak utilizes a highly disciplined, rules-based process, resulting in a portfolio that is reliable, repeatable, and unemotional.

How to Invest

- Efficient Growth is currently available as an SMA and ETF. (ETF specifics and SMA historical performance can't be shared in the same letter - sorry, it's annoying, I know. Please inquire for the ticker or more information.)

- In just 20 months, The ETF Which Shall Not Be Named has grown almost 16,000% since launch – from 2 to 318mm.

Performance update:

- Running Oak’s Efficient Growth portfolio is up 0.15%, gross, versus -2.57% for the S&P 500, year-to-date through March 26, 2025.

Efficient Growth was down -1.67%, gross of fees (-1.71%, net), in February.*

Consistently Not Stupid

“It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.” – Charlie Munger

Running Oak’s Efficient Growth strategy is – in all ways – designed to be “consistently not stupid”. We don’t claim to be the most brilliant (even if we like to think we are). We do claim a disciplined adherence to avoiding stupidity.

Here’s why that is critical: NOTHING KILLS EXPONENTIAL/COMPOUND GROWTH LIKE LARGE DRAWDOWNS. (In other words, nothing kills exponential/compound growth like stupidity, even occasional stupidity. Exponential growth and compounding wealth is precisely what clients want. Protect it; don’t kill it.)

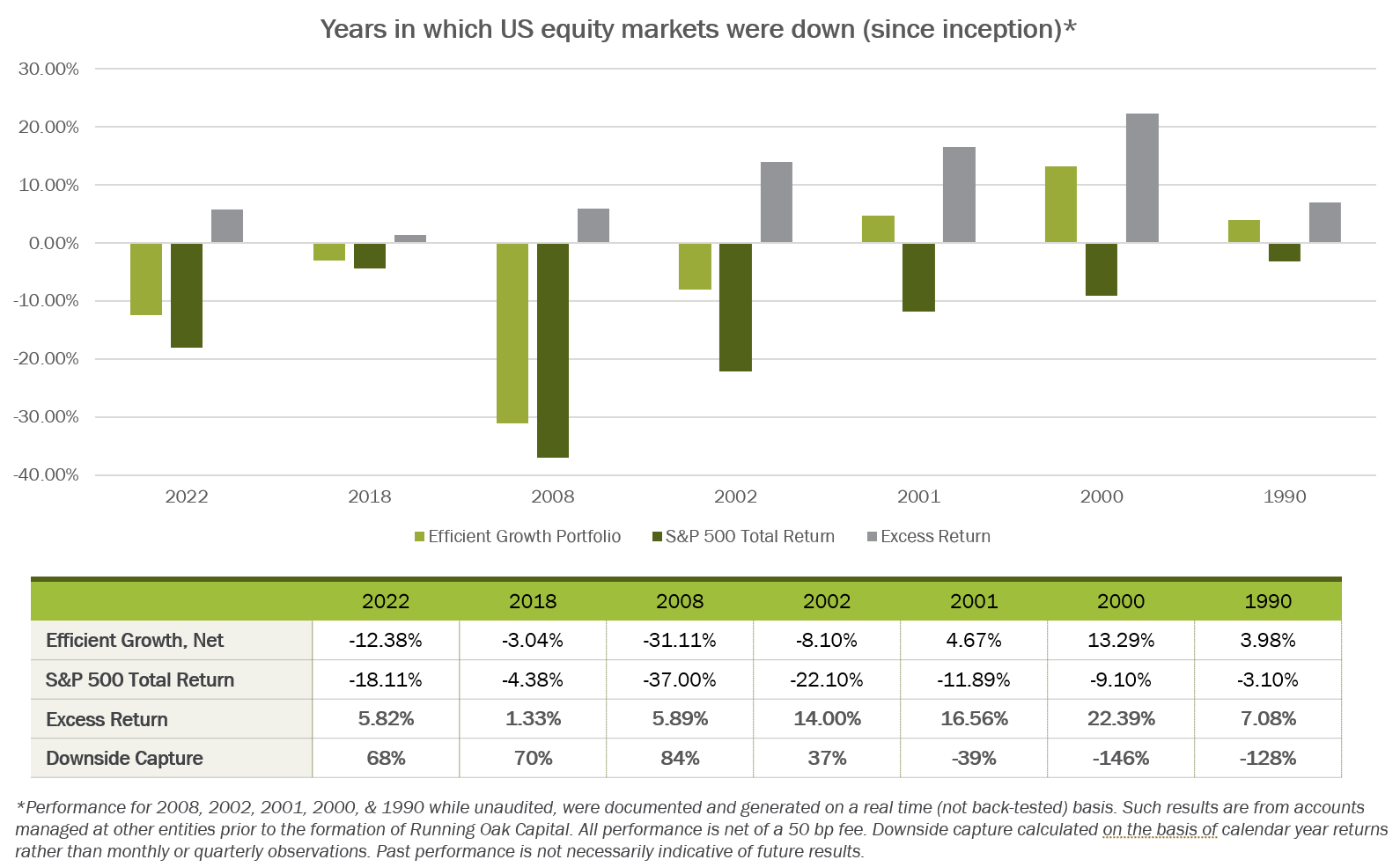

The table below illustrates the extent to which large drawdowns - or occasional stupidity - kills compounding.

By striving to be consistently not stupid, drawdowns are likely to be smaller. Case in point, Running Oak outperformed the S&P 500 Total Return Index every down year since 1989.* Efficient Growth is up 0.15%, gross, versus -2.57% for the S&P 500, year-to-date through March 26, 2025.* Consistently not stupid wins.

"The problem with the world is that the intelligent people are full of doubts, while the stupid ones are full of confidence." – Charles Bukowski

We strongly doubt our ability to deliver unemotional, unbiased portfolio management perfection consistently. Here are a couple ways in which we ensure our own inevitable stupidity doesn’t negatively impact YOUR clients’ exponential growth:

Common Sense – The investment philosophy of

- Maximize Earnings Growth

- Don’t Pay a Stupid Price

- Lessen Drawdowns

isn’t the fanciest, most brilliant strategy. It certainly isn’t the smartest sounding. It is simple and common sense, therefore dependable, and blatantly not stupid.

Disciplined, Consistent, Reliable – Our rules-based investment process is highly disciplined, ensuring that we consistently aren’t stupid. We do the same non-stupid actions over and over and over annnnd over…, just as we’ve done for 4 decades.

Our investment rules are akin to the bumpers you place in bowling alley gutters for 4-year-olds. We think we’re brilliant and excellent bowlers, much like the average 4-year-old using the granny shot free throw technique, but you don’t want your clients’ financial well-being depending upon us actually bowling strike after strike. Let’s be honest: despite my belief that I’m a good bowler, I stink. We believe we’re excellent money managers, but we’re also people and, therefore, prone to emotions and biases.

"The difference between stupidity and genius is that genius has its limits." – Albert Einstein

Rather than relying upon us to be consistently more brilliant than everyone else, it’s more dependable to throw in some bumpers, making it especially challenging to throw a gutter ball. We intentionally limit our stupidity through the application of thoughtful rules.

You could invest in a strategy that is intentionally consistently not stupid, or… you could invest like the majority and in strategies that are inherently stupid by design. Here are a couple examples that are likely to have a particularly large negative impact on client returns over the next several years:

Consistently Stupid #1: Buy, Then Do Absolutely Nothing – Every time the market goes up a lot, armchair investment managers all say the same thing, “Hold your winners. Sell your losers”, as though even a 4-year-old bowler without gutter bumpers can do it. Holding an asset that SHOULD go down - because it’s worth less than the price at which you can sell it - is CONSISTENTLY STUPID.

Active Management – A paper published in the Financial Analysts Journal concluded that the reason many managers fail to provide value over the index is they lack sell discipline. Many hold their winners all the way up… then allllll the way back down.

Passive Management – By construction, passive portfolios are more concentrated in the most overvalued companies and less concentrated in the most undervalued companies at the top. In other words, you own the most of what you don’t want at the worst possible time and the least of what you do want at the best possible time, because they never sell or take profits. That is structural stupidity. During periods of high momentum, like the last decade, being stupid in that manner works, but you’d better sell before it turns. Being occasionally stupid might not hurt you. Being consistently stupid will.

Running Oak – By design, we add to losers, if – fundamentally - they’re winners. We sell winners, if – fundamentally – they’re losers. In other words, we sell stocks that should go down, a weirdly controversial practice.

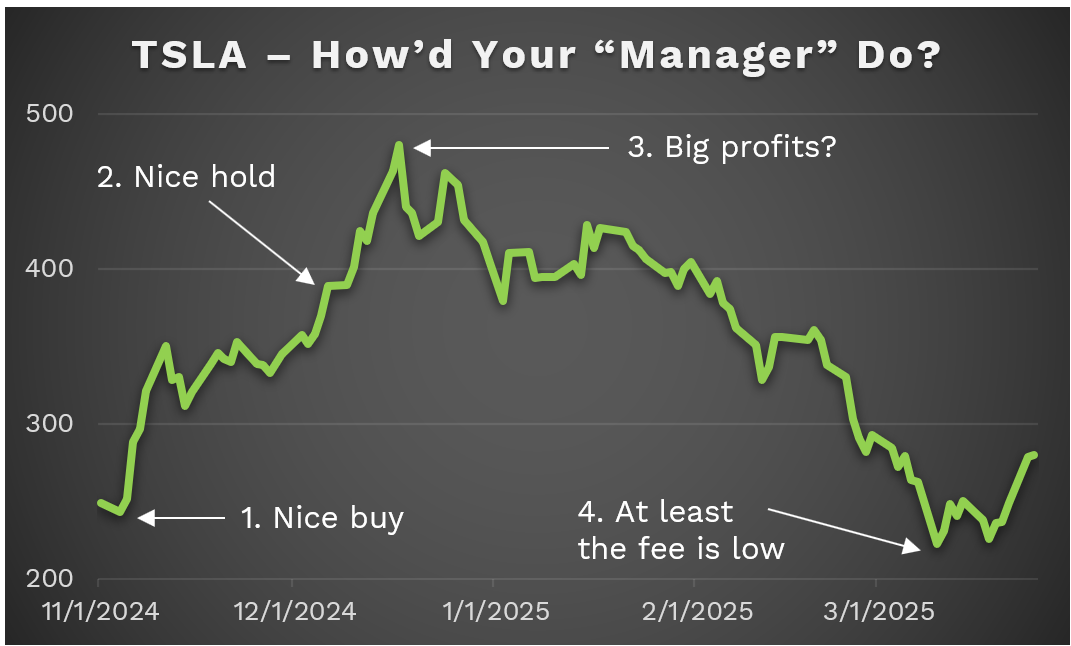

Case Study: Tesla

- Did your “manager” happen to own a ton of Tesla as it doubled in only 30 trading days following the presidential election? If so, nice!

- Did your "manager” trim your significant Tesla holdings as one of the largest companies in the world doubled in a handful of days for no reason whatsoever? If not, hopefully you got the top.

- Did your “manager” sell at the top, taking big profits, knowing there was no reason whatsoever for Tesla to have doubled, let alone be priced at 5x the forward multiple of NVDA? If not, that’s unfortunate.

- Or, did your “manager” hold the exact same amount all the way up and then all the way back down, letting a 2x return over a handful of days in one of the largest companies in the world evaporate? If so, that’s pretty stupid.

Consistently Stupid #2: Zombies

I've never met a zombie, personally, but they're generally considered to be pretty dumb, some might say stupid. Handing a client's hard-earned money to a zombie seems unwise; they just don't appear to be very conscientious. Consistently handing money to zombies, expecting more money in the future, would be consistently stupid. Zombie companies are the corporate walking dead. They don't generate enough income to service their debt.

- 2 to 4% of the companies in the S&P 500 Index are zombies.

- Over 10% of Russell 3000 companies are zombies.

- Many companies are on the cusp of zombie-hood. If we experience a recession, index fund investors will be well allocated to the zombie apocalypse.

- Investors in the S&P 500 and Russell 3000 indexes pay fees to be consistently invested in zombie companies.

Running Oak consistently invests in profitable, high growth, attractively valued companies with lower debt levels. Running Oak consistently doesn't hand our clients' money to zombies. Doing otherwise would not be consistently not stupid.

Mid Cap Reminder - Mid Cap stocks have outperformed Large Cap by 60bps over the last 33 years, AND they’re cheaper, AND they’re under-invested. The typical equity investor is woefully underinvested in upper Mid Cap and lower Large Cap (MARGE), in particular. Efficient Growth fills that gap like few strategies do, providing value like even fewer do.

Running Oak's goal is to maximize the exponential growth of clients' portfolios, while subjecting them to far less risk of loss. In other words, we aim to help your clients realize their dreams and avoid their nightmares.

If you appreciate critical thinking, math, common sense, and occasional sarcasm, we would love to speak with you. Please feel free to set up a time here: Schedule a call.

Best,

Seth L. Cogswell

Founder and Managing Partner

Edina, MN 55424

P +1 919.656.3712

For additional data and context regarding the claims made within this email, please refer to the Disclosures and Additional Data document located here.

“All opinions expressed in this newsletter are those of Running Oak Capital’s and do not constitute investment advice.”

Investment Advisory Services are offered through Running Oak Capital, a registered investment adviser.

*Past performance is no guarantee of future results. Performance expectations are no guarantee of future results; they reflect educated guesses that may or may not come to fruition. All indices are unmanaged and may not be invested into directly.

*YTD performance through 3/26/2025 is reflective of a representative account within the Efficient Growth composite of which is substantially similar and has performed closely in-line with broader composite returns historically.

*Statements reflect the opinion of Running Oak Capital on the average investor’s equity portfolio allocation. This is based on informal feedback and experience from interactions with investors and other financial professionals.

Statements on the ‘typical equity portfolio’ are based on informal feedback and experience from interactions with investors and other financial professionals. Further, statements on where the most attractive risk/reward asymmetry lie, although based on observable data, reflect the opinion of Running Oak Capital.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments and strategies may be appropriate for you, consult with us at Running Oak Capital or another trusted investment adviser.

Stock prices and index returns provided by Standard & Poor’s.

Latest articles

This data feed is not available at this time.

Data is currently not available